Efficiency technology and cost assessment for U.S. 2025–2030 light-duty vehicles

Blog

The better path for the US auto industry is more efficiency technology, not less

What uncertain times we live in. The automakers wasted no time in calling on the new Trump administration to ease the light-duty vehicle efficiency standards that were established under the Obama administration for model years 2022 to 2025. The same automakers had applauded and smiled, not once but twice, as they committed the industry to farsighted efficiency standards just a few years ago. Well, times have changed. And the new White House looks more than willing to accommodate. This is what elections do.

Automakers are, at a minimum, trying to steer the regulation into the slow lane by pushing the date of final decision on the 2022–2025 targets back out to 2018. They’re also seizing the opportunity to blunt the point of the standards with bids for more “off-cycle credits” (e.g., see Fiat, Ford, GM, BMW, VW, Mercedes), and flexibilities from arcane tweaks to harmonize federal and state rules. This could help pave the way for additional credits like for autonomous-driving technologies and even ride-shared vehicles that will be entering the fleet regardless. It looks like no one is seeking to end California’s ability to be set its own emission standards, or for other states to opt for California’s standards—or, most drastically, fundamentally questioning emission rules as such. That is good news, at least for now, in these uncertain times.

Of course, California also drives the nation’s vehicle emissions policy. And policy makers in the Golden State appear ready to fight for the targets established in 2012. Other governors and mayors have also spoken up in opposition to the automakers’ lobbying. There are 13 states committed to California’s clean car standards. Together they represent over a third of the U.S. market, nearly 6 million annual auto sales. That makes for a lot of car buyers, and a lot of state attorneys general. Speaking of which, there were 12 states that previously took this to the Supreme Court—and won.

At the ICCT we habitually focus on the long-term perspective—which, at the moment, means staying focused on how steady incremental improvements can be deployed across the world’s cars. This means reducing risks and ensuring a clear regulatory path to provide for secure technology investments. Our latest technology assessment is meant to more fully inform the current U.S. debate, assessing the technologies that will sustain vehicle efficiency improvements and their associated costs.

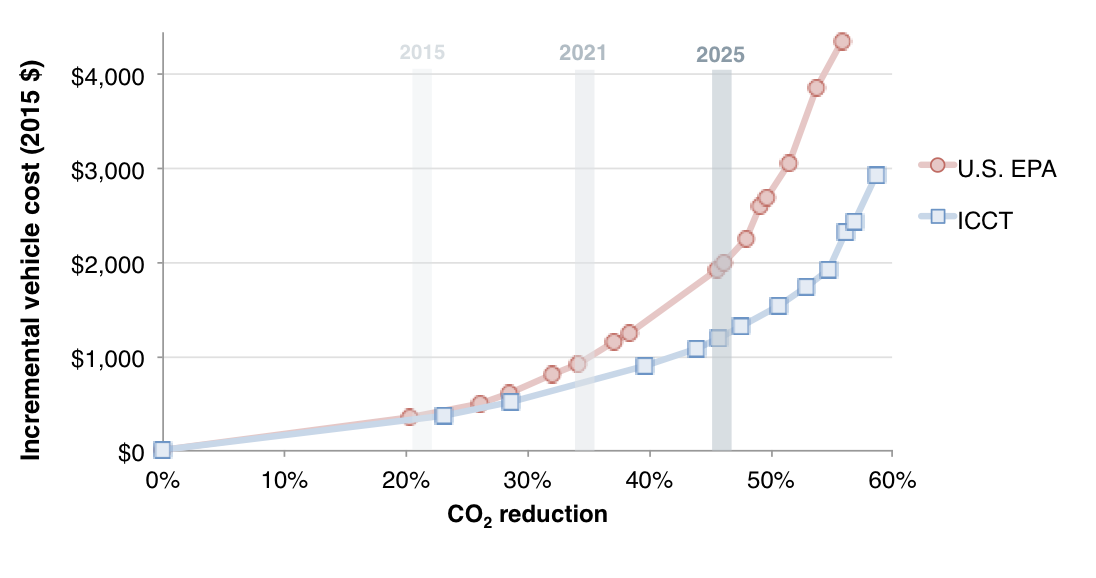

What did we find in our analysis? That there are lots of efficiency technologies, they keep improving, and they’re cost-effective. In fact, the technology costs to comply with the 2025 standards are 30% to 40% lower than the EPA/NHTSA projections (see figure). Innovation in technologies like turbocharging, high-compression cylinder deactivation, lightweighting (what Fiat-Chrysler’s Marchionne used to refer to as plain-vanilla technology) keep letting us eke more miles out of each gallon of gasoline. Car buyers are the ones who reap the rewards, getting fuel savings that are two to three times the technology cost, even if gas prices stay low.

Vehicle efficiency technology cost to reduce carbon emissions

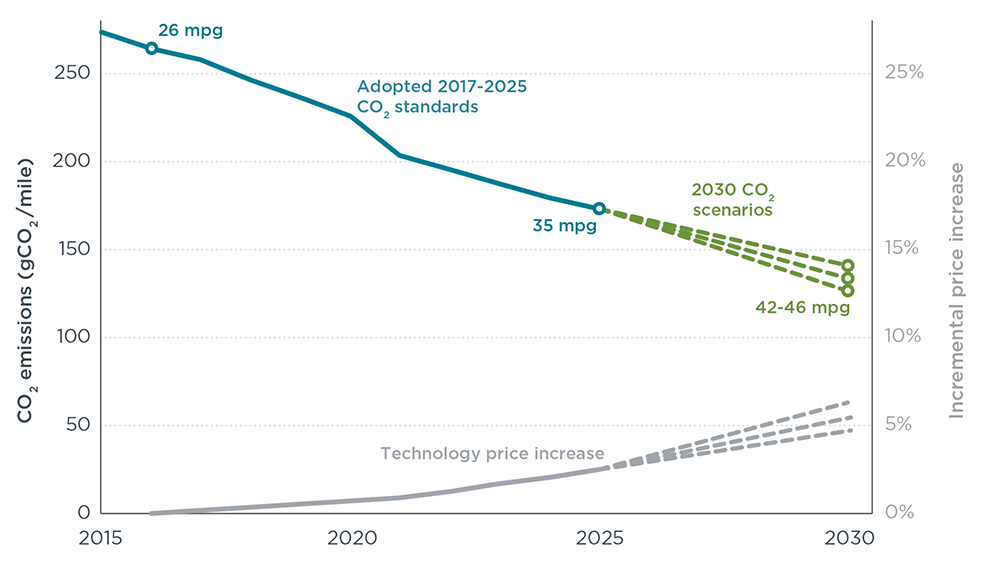

We also looked at how the new vehicle fleet could keep improving: from 26 mpg today, to 35 mpg in 2025 with the adopted standards, to 42–46 mpg in 2030. (These are consumer label fuel economy values, whereas the regulatory test cycle fuel economy is higher). On average, new MY 2030 vehicles could get 60% better mileage in exchange for an increase in vehicle price of just 5%—a very reasonable proposition indeed. I know 2030 sounds like a long way away. But that’s the point of steady, gradual, long-term regulation: When there’s lots of lead-time for automakers, it creates a stable environment to make long-term investments to gradually roll out lower-cost technology over time. We all win.

Increased vehicle efficiency, reduction in vehicle emissions, associated costs

Those technology investments affect national and global market outcomes. Strong standards with long regulatory lead-times are pillars of good energy, technology, and industrial policy. The present uncertainty is the antithesis of that, and could well ensure that the U.S. market lags behind Europe and China in technology innovation and adoption. The automakers and the White House could bring that about. Our research suggests that the better path—for technology investments, consumers, and the environment—is to keep driving forward.