Blog

The power of vehicle taxation schemes

In an earlier blog post, I wrote about the current vehicle market structure in Turkey and also mentioned that purchasing and owning a vehicle in Turkey is quite expensive, mainly due to the high purchase tax that is imposed on new vehicles. Over the past months, as one of the 2015/16 Fellows at the Mercator Istanbul Policy Center (IPC), I had the opportunity to take a closer look at vehicle taxation and other policy measures that could potentially help driving down emissions from the vehicle fleet in Turkey. Some aspects of my analysis for Turkey, summarized here and here, are also relevant to other vehicle markets worldwide. In particular, the powerful impact that vehicle taxation schemes can have on market structure and vehicle emission levels are illuminated by the example of Turkey.

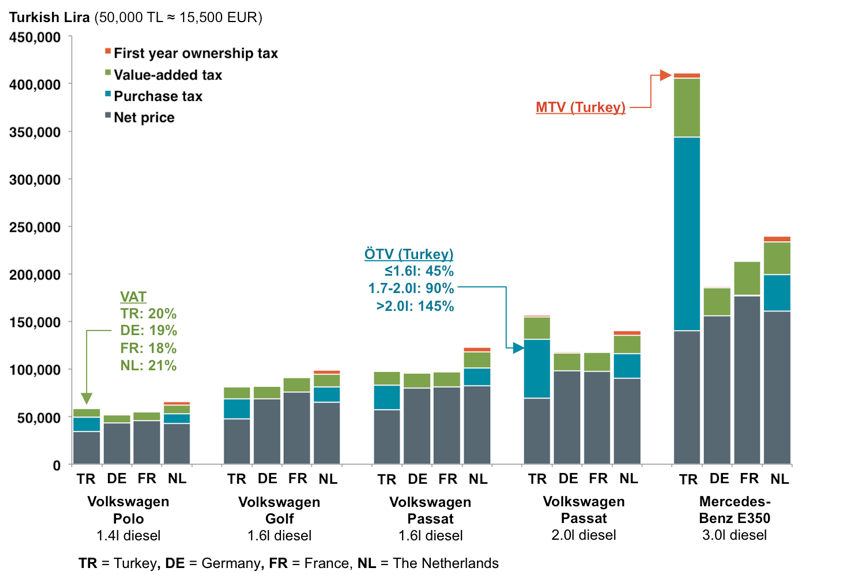

New passenger cars in Turkey are subject to the general value added tax (VAT), which is 18% and applies to all goods. In addition, a special purchase tax is levied, in Turkish called Motorlu Taşıt Araçlarına İlişkin Özel Tüketim Vergisi (ÖTV). In addition to cars, this ÖTV is also levied on tobacco, alcohol and various other items that are considered luxury products. The amount of ÖTV to be collected depends on the engine displacement of a vehicle and ranges from 45% to 145% of the vehicle’s base price. An important tax threshold is at 1.6L engine size. Above this threshold, the taxation level doubles from 45% to 90%. Another threshold is at 2.0L, above which the taxation level increases to 145%. The impact of this tax design is quite dramatic: For a new car worth 20,000 Euros the sales tax is 9,000 Euros if it has an engine displacement of 1.6L or below, but 18,000 Euros if it is 1.7L or above. No wonder that 95% of new cars in Turkey have an engine displacement of 1.6L or below.

The significance of the vehicle taxation scheme in Turkey becomes even more obvious when comparing it to other markets. Figure 1 compares vehicle net prices and taxation levels for five selected vehicle models in four different markets (Turkey, Germany, France, the Netherlands). The models chosen are among the most popular ones within their respective vehicle size segment and are available for sale in all of the four markets. The first three models—a VW Polo, Golf and Passat—all fall below the ≤1.6L engine displacement threshold in Turkey and are subject to the lowest possible taxation level of 45% of the vehicle’s net price. The end price for the customer for these three vehicles is relatively similar for all markets considered, highest in the Netherlands. For the 2.0L engine version of the VW Passat, the situation is different. This vehicle is subject to a 90% ÖTV in Turkey, and as a result the consumer end-price in Turkey is significantly higher than for the same model in Germany, France, and the Netherlands. The last vehicle model, a Mercedes-Benz E350, is subject to a 145% ÖTV in Turkey, and the resulting combination of vehicle net price and taxes is far higher than in any of the other markets. For both the Passat 2.0L and the E350, the amount of taxes to be paid in Turkey is in fact higher than the vehicle net price.

Figure 1. Sales prices and taxation levels for selected vehicle models in Turkey, Germany, France and the Netherlands.

So there is no question that the vehicle taxation scheme in Turkey is powerful in directing vehicle customers’ purchase decisions. But in its current form it incentivizes customers to choose a vehicle with low engine displacement and low price. The CO2 emissions of a vehicle have no direct impact on the taxation level. For example, a Toyota Yaris hybrid model with a CO2 emission level of 78 g/km (according to the NEDC test procedure) under the current Turkish vehicle taxation scheme ends up paying about the same level of tax as a Dacia Duster SUV with CO2 emissions of 137 g/km. This is because both models have about the same engine displacement and about the same net price. Given this situation, it does not come as a surprise that the market share of hybrid (and other electrified) vehicles in Turkey is currently below 0.1%.

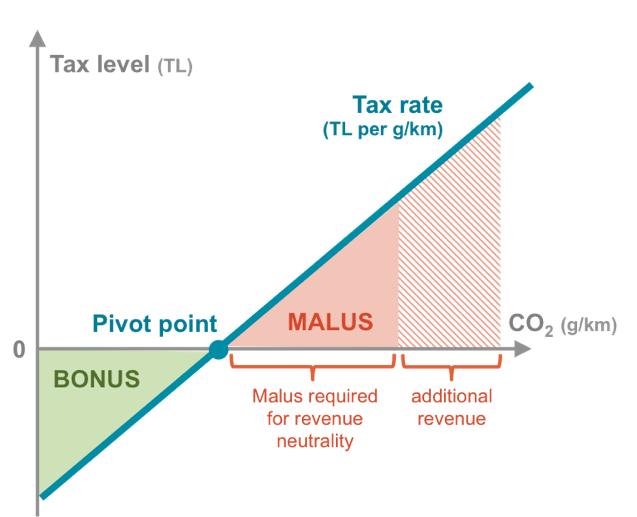

Changing the vehicle taxation scheme in Turkey from one based on engine displacement to one that uses CO2 emissions as the underlying metric would help to overcome the current market hurdle for low-emission vehicles. Figure 2 illustrates what such a taxation scheme would look like. The taxation level would be based on the CO2 emissions of a vehicle, and a linear tax function would be applied without any discrete tax threshold steps (to avoid any unintended clustering around tax thresholds). Vehicles below a set pivot point would receive a bonus payment, while vehicles above the pivot point have to pay a malus. The revenue collected from the malus payments would be used to balance out the bonus payments for low-emission vehicles, thereby ensuring budget neutrality from a government perspective. To help governments around the world design such a feebate-like vehicle taxation system, ICCT offers a calculation tool that can be downloaded and used by anyone interested in the subject.

Figure 2. Schematic illustration of best-practice design for a feebate-like vehicle taxation scheme.

Switching to a CO2-based vehicle taxation scheme provides a win-win situation not only for the government (vehicle emissions are reduced, while overall tax revenues are maintained), but also for customers (CO2 emissions of a vehicle are directly linked to fuel consumption, i.e., choosing a vehicle with lower CO2 emissions not only reduces tax payments but also fuel costs) and the vehicle manufacturing industry (car manufacturers and parts suppliers have certainty that their low-emission vehicle technologies will be purchased and so have an incentive to invest into these technologies and maintain their competitive position). These advantages make a feebate system attractive not only for Turkey but really for any vehicle market that wants to make use of the power of vehicle taxation schemes to reduce emission levels.