Blog

Early Christmas present to the car industry, or lump of coal? The European Commission regulatory proposal for reducing new vehicle CO2 emissions post-2020

The timing was chosen carefully. The 23rd Conference of Parties (COP) had just started in Bonn, Germany, when the European Commission revealed its regulatory proposal for reducing CO2 emissions from passenger cars and light-commercial vehicles on November 8. Many delegates had hoped that the head of the EU’s Climate Action & Energy section, Commissioner Miguel Arias Cañete, would send a clear signal towards de-carbonization of the road transport sector in Europe. In light the harsh critique that dominated the media hours immediately following the long-awaited announcement (see, for example, here), it seems as if these hopes have been dashed.

But let’s see what the regulatory proposal includes and doesn’t include — as far as we can tell right now, that is, having only had time to glance through the 400+ pages of documents that the Commission published on November 8.

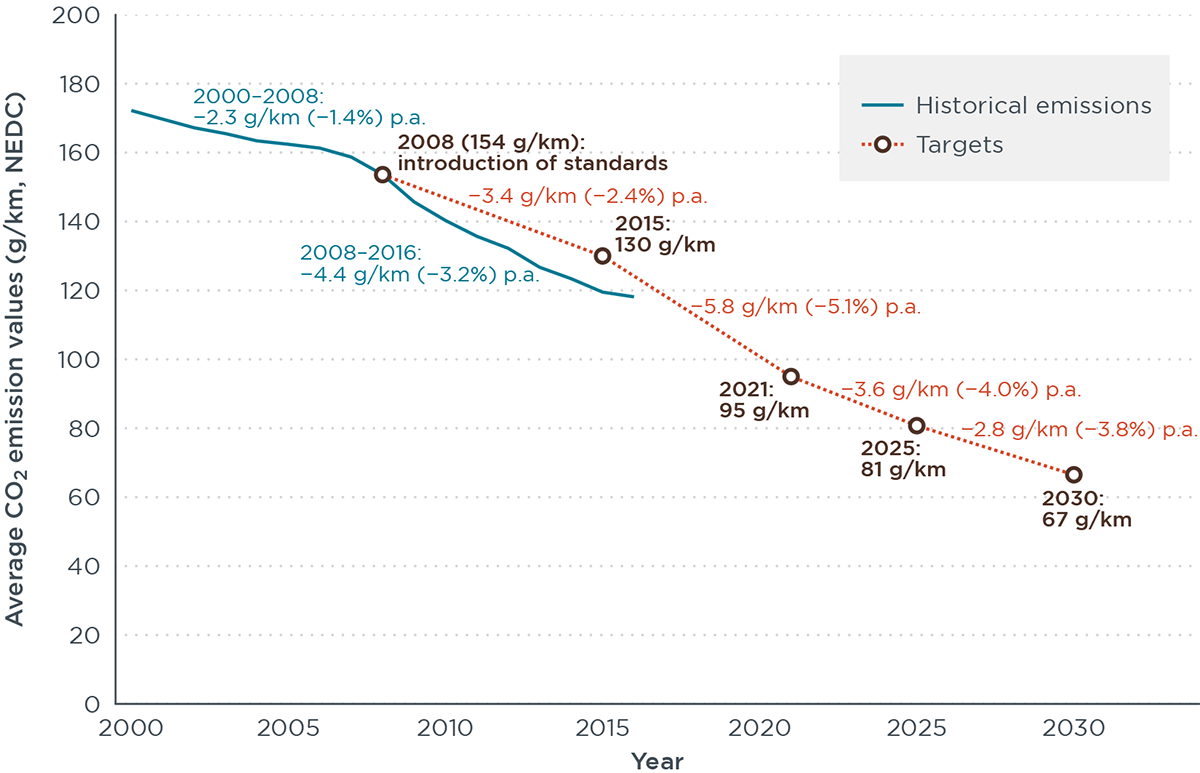

The current EU regulation covers the time period up to 2021 for passenger cars and 2020 for light-commercial vehicles (LCVs), and sets an average CO2 target of 95 g/km for cars and 147g/km for LCVs. This is relating to the “old” regulatory test cycle, the NEDC, and corresponds to an annual CO2 reduction of about 5%.

The new regulation proposed by the Commission extends the time period to 2030. This would give the EU new car CO2 regulation the longest time horizon worldwide. Instead of defining an absolute CO2 target for the average new car fleet (as was/is the case for 2015 and for 2021), the Commission now proposes a percentage reduction target instead. New cars, on average, would have to reduce their CO2 emission level by 30% by 2030, compared to the 2021 starting point. However, the reference to vehicle mass remains. That is, under the new regulation, like the old, heavier vehicles would be allowed to emit more CO2 than lighter vehicles. In NEDC terms, this would mean that the average 2030 target value would correspond to a CO2 level of approximately 67 g/km, or an annual reduction of around 4% (see Figure 1). In this sense, the level of ambition of the new 2030 regulation would lie somewhere between the 2015 regulation (2.5% annual CO2 reduction) and the 2021 regulation (-5%). Looking at absolute CO2 reductions instead of percentage reductions, the Commission proposal would require an annual reduction of 2.8 g/km for the 2030 regulation and thereby would be less ambitious than the 5.8 g/km annual reduction as part of the 2021 reduction. Ahead of the publication of the regulatory proposal, this 30% reduction target for 2030 was under heavy lobby attack, with car manufacturer associations arguing for only 20% reduction and a group of EU member states asking the Commission to go for a 40% reduction instead.

Development of average CO2 emission level for new passenger cars in the EU and current as well as proposed regulatory target values.

In addition to a 2030 target, the Commission proposal also introduces a 2025 interim target. This interim target also came under heavy attack, and for some time it was unclear whether it would remain in the final version of the proposal or not. The required average reduction level for 2025 is 15%, again compared to the 2021 starting point. In NEDC terms, this would equal a target value of approximately 81 g/km for 2025. This level is higher than the range of 68–78 g/km that the European Parliament back in 2013 suggested for the target year 2025.

Why did the European Commission move away from absolute CO2 target levels altogether and instead now suggests percentage reductions? Because of the switch to a new emissions’ test procedure, the WLTP, which is being introduced gradually for new vehicles from September 2017 onwards. The Commission argues that with the transition it is impossible to know already now what exactly will be the starting point in 2021 in g/km. As we have pointed out in a recent briefing paper, this approach entails the risk that vehicle manufacturers will try to achieve a particularly beneficial NEDC-WLTP correlation factor, which would inflate the WLTP starting point for 2021. As a result, percentage reductions between 2021 and 2030 would be less significant in terms of g/km reductions. It seems from the proposal that the Commission is planning to safeguard against such gaming by requiring vehicle manufacturers to install fuel consumption meters in their vehicles that would help to monitor real-world CO2 emissions as opposed to test cycle values only, as is the case today. It is well received that the Commission proposal also provides for finally including the verification of CO2 emissions during in-service conformity testing; any deviation between the measured and type-approval value would be used in the calculation of the manufacturers fleet average CO2 emissions according to the proposal.

In addition to percentage reduction targets for the average fleet of a manufacturer, the Commission proposal also includes a crediting system based on the market share of ultra-low emitting vehicles (<50 g/km). For 2025 the target value is 15%, and for 2030 it is 30% of a manufacturer’s overall new car sales. Each vehicle below a CO2 emission level of 50 g/km counts as a low-emission vehicle but the lower the CO2 emission of a vehicle, the more it counts towards the target value. For example, a vehicle with 25 g/km of CO2 only counts as half a vehicle in this context. Even though the commission considered making these ULEV targets mandatory, the proposal released only includes a credit for exceeding them, and no penalty for failing to meet these 2025/30 electric vehicle sales targets. In this respect, the European Commission proposal is less stringent than the regulations in California and China, where there are penalties for not meeting the respective electric vehicle quotas. In case a manufacturer exceeds the 2025/30 electric vehicle target, the European Commission is proposing to grant a bonus of up to 5% of the manufacturer’s fleet CO2 target. For example, a manufacturer that would sell 20% of its fleet in 2025 as zero-emission vehicles would have to reduce its overall fleet CO2 emission level only by 11% compared to the 2021 starting point, rather than facing the standard 15% reduction requirement.

Considering that BMW and Daimler already announced that 15–25% of their sales by 2025 would be electric cars, and that Volkswagen even expects 20–25% of its 2025 sales to be electric, the zero- and low-emission targets the Commission proposes are criticized by NGOs as not ambitious enough (one called them an “early Christmas present to the car industry”). These critics object in particular that the targets are not to be binding for manufacturers. Furthermore, the overall CO2 reduction requirements suggested by the Commission face harsh criticism. While the European car manufacturers’ association calls the proposal “overly challenging”, the German Federal Environmental Agency (UBA) calls for a reduction of new car CO2 fleet levels of “close to 70%” for 2030 compared to 2021 and for a 70% market share of electric vehicles by 2030 in order for Germany to be able to meet its agreed climate reduction target for the transport sector. Depending on the final outcome of the EU regulation, it seems likely that we will face a patchwork of electric vehicle sales mandates in the future, with a number of EU member states moving forward with an additional electric vehicles’ quota, on top of an EU wide target value.

As for the social benefits of the proposed regulation, the European Commission expects that the new vehicle CO2 standards would help to reduce 170 million tonnes of CO2 between 2020 and 2030 and would create 70,000 new jobs. Consumers would save up to around 1,500 Euros per car bought in 2030, and the EU would import less oil, worth around 125 billion Euros over the 2020 to 2040 time period.

As a next step, the European Commission regulatory proposal will now be submitted to the European Parliament and the European Council (the EU member states) for further political negotiations. Depending on how quickly the regulatory process moves forward, the final regulation could be adopted by the end of 2018 or early 2019.