Blog

U.S. airline fleets due for renewal

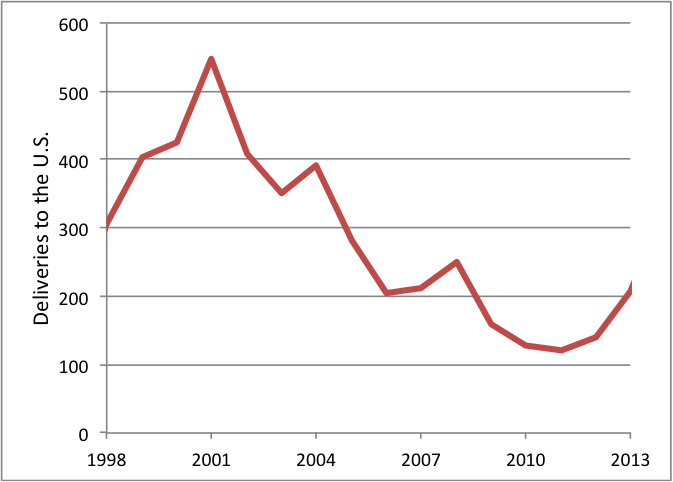

One of the main takeaways from our 2013 U.S. airline fuel efficiency ranking is that overall U.S. domestic airlines showed no year-to-year improvement in fuel efficiency. That is not surprising. In the past 15 years, relatively few new, more efficient single aisle aircraft types were brought to the market and purchased by the airlines. In addition, deliveries of new passenger aircraft to the U.S. have also been falling for more than a decade. U.S. airlines did purchase over 200 new aircraft in 2013, including Boeing Next Generation 737s with winglets and Airbus A320s with sharklets. That represents an increase over the last few years, but viewed in a slightly longer context, it’s still a low number.

New passenger aircraft deliveries to the U.S., 1998-2013

Source: Ascend Fleets database (August 2014)

Note: Aircraft deliveries include narrowbody, widebody, regional jet, and turboprop aircraft.

Almost 550 aircraft (48% of the global total) were delivered in the U.S. in 2001. But that number declined and then flattened out in recent years (to 14% of total global deliveries in 2013), while deliveries to the rest of the world have been rising steadily.

Airlines that may not have the best fuel efficiency today often point to their fleet renewal plans to demonstrate their commitment to efficiency and environmental protection. Examples include United, which intends to replace its entire fleet of aging Boeing 757-200 aircraft (averaging 19 years) with new Boeing 737-900ERs by 2015. American Airlines, which we ranked as the least efficient U.S. domestic airline in 2013 due in part to a 1.5% drop in fuel efficiency from 2012, anticipates receiving more new aircraft deliveries than any other U.S. carrier through 2022. American Airlines’ fleet renewal program took flight in 2009, when it began to replace its MD-80 aircraft (averaging 22 years) with more fuel-efficient Boeing 737-800s. Its fleet now includes 226 of those aircraft, with 80 more on order. American plans to enhance its fleet further with new types including the Boeing 737 MAX family (100 orders) and Airbus A320 NEO (130 orders) beginning in 2017, and argues that in five years it will have the “U.S. airline industry’s youngest and most fuel-efficient fleet.”

That’s an empirical question – the type we like. To assess how much of an impact fleet renewal programs will have on each airline’s average fleet age, we projected the average fleet age through 2020 using the 2013 fleet as a baseline, aircraft deliveries by airline from the Ascend Fleets database, standard aircraft retirement curves, and activity projections based upon the recent past. We also estimated a simple fleet turnover rate, or the number of years it will take each airline to replace its current fleet (in 2013) entirely with new aircraft. For Allegiant Air, which purchases only used aircraft such as those shed in the American-US Airways merger, no attempt was made to project a 2020 average age due to the high uncertainty both in timing and age of purchased aircraft.

U.S. airline fleet size, deliveries, turnover rate, and average age

| Airline | 2013 fleet size | 2014–2020 projected deliveries | Simple fleet turnover rate (yrs) | Avg. fleet age (yrs), 2013 | Avg. fleet age (yrs), 2020 (est.) |

| Alaska Airlines | 128 | 95 | 9 | 9 | 8 |

| Allegiant Air | 70 | 0 | — | 22 | — |

| American-US Airways (merger) | 967 | 830 | 8 | 13 | 7 |

| Delta Air Lines | 794 | 260 | 21 | 16 | 15 |

| Frontier Airlines | 54 | 80 | 5 | 7 | 6 |

| Hawaiian Airlines | 43 | 43 | 7 | 9 | 7 |

| JetBlue Airways | 194 | 106 | 13 | 7 | 9 |

| Southwest Airlines | 675 | 233 | 20 | 11 | 12 |

| Spirit Airlines | 54 | 100 | 4 | 5 | 6 |

| Sun Country Airlines | 18 | 2 | 63 | 11 | 17 |

| United Airlines | 687 | 350 | 14 | 13 | 11 |

| Virgin America | 53 | 21 | 18 | 4 | 9 |

| Total | 3737 | 2120 | 12 | 13 | 11 |

Source: Flightglobal Ascend Fleets database (August 2014)

Note: Aircraft deliveries include order, option, option LoI, and LoI. Fleet turn-over rates were estimated by taking the current fleet count and dividing by the annual average number of deliveries from 2014-2020.

This simple analysis, which cannot account for used aircraft purchases or the sale of still flyable aircraft to second users, for example after a merger, nonetheless allows some interesting comparisons to be made. If current aircraft orders hold, Spirit and Frontier will have the U.S.’s youngest fleets in 2020, both averaging about 6 years, due to aggressive aircraft purchasing. With 61 Airbus aircraft in service and a total of 55 A320neo and A321neo orders, Spirit could completely replace (or, more likely, double the size of) its current fleet in only 4 years. Similarly, Frontier has 79 A319neo and A320neo orders through 2020 and could potentially turn over its current fleet with new aircraft by 2020.

Back to American’s claim. We estimate that American’s fleet age, when combined with the aging US Airways’ fleet, may fall by almost 50%, from 13 years in 2013 to 7 years in 2020 – right behind Spirit and Frontier. Thus, unless American is able to shed its much older fleet (e.g., MD-80s) very quickly, it will be questionable whether it will have the youngest U.S. fleet in 2020. The average age of Virgin America’s fleet, the youngest fleet in 2013, is expected to double by 2020, due to relatively few near-term new aircraft deliveries. Other airlines, like Sun Country, also don’t appear to be investing in new aircraft anytime soon. Overall, the average fleet age for major U.S. carriers is expected to fall moderately, from 13 years in 2013 to 11 years in 2020. Some of the largest (and older) airlines in the U.S. – notably Southwest and Delta – would take 20+ years to turn over their fleet at their present rate of new deliveries.

This analysis assumes that Boeing and Airbus’s current robust order sheet will hold, which may not be realistic given the recent collapse in oil prices. While airlines like American – the largest U.S. airline after its merger with US Airways (in terms of scheduled passengers carried) – are expected to make progress in fleet renewal, other airlines have aging fleets that are also overdue for renewal. In order for the U.S. aviation sector to meet its 2020 carbon-neutral growth goal, airline efficiency improvements via new aircraft and engine technology are going to have to increase sharply from their present rate.