Aviation climate finance using a global frequent flying levy

Blog

Would a frequent flying tax be progressive?

Last year, the aviation sector finally established a long-term climate goal of net-zero carbon emissions by 2050. While low-carbon technologies that help achieve this goal are emerging, it is unclear who will pay for them and how.

In September last year, we published a proposal for using a global frequent flying levy (FFL) to cover the estimated abatement cost of commercial aviation. A frequent flyer levy is a per-flight tax that increases in amount as one takes more flights in a year. We argued that an FFL would raise the revenue in a progressive manner, because it would, at least in our proposal, generate virtually all (98%) of its revenue from the world’s richest 20%. The escalating levy would place less tax burden on lower-income populations compared to a flat tax—although, as we noted in the paper, because of how unevenly distributed flying is around the world even a flat tax would generate most of its revenue (80%) from the richest 20%.

While concentrating tax burden on the global wealthy is a nudge towards equality, there are more common ways to determine whether a tax is progressive or regressive: does the tax rate increase with the total taxable amount, and do the poor need to pay a larger proportion of their income compared to the rich? Classic examples of regressive taxes include sales tax and property tax; spending on necessities makes up a larger share of poorer households’ income than richer households’.

Since a fair amount of the energy the less well-off consume is necessary consumption, a carbon tax can at least potentially be regressive. However, a 2020 study looking at OECD countries demonstrated that a carbon tax can be progressive in countries with low income inequality (e.g., Sweden and Denmark), and that even when the overall carbon tax is regressive, it can be progressive for luxury goods.

Air travel, at least defined in economic terms, is a luxury good (income elasticity greater than one). Taxing aviation is therefore very different from taxing the rest of our carbon-emitting activities. Lower-income households will have a lot less exposure to the tax, as they generally fly less. A 2022 study based on UK data confirmed this logic and concluded that “all taxes on air travel are distributionally neutral or progressive.”

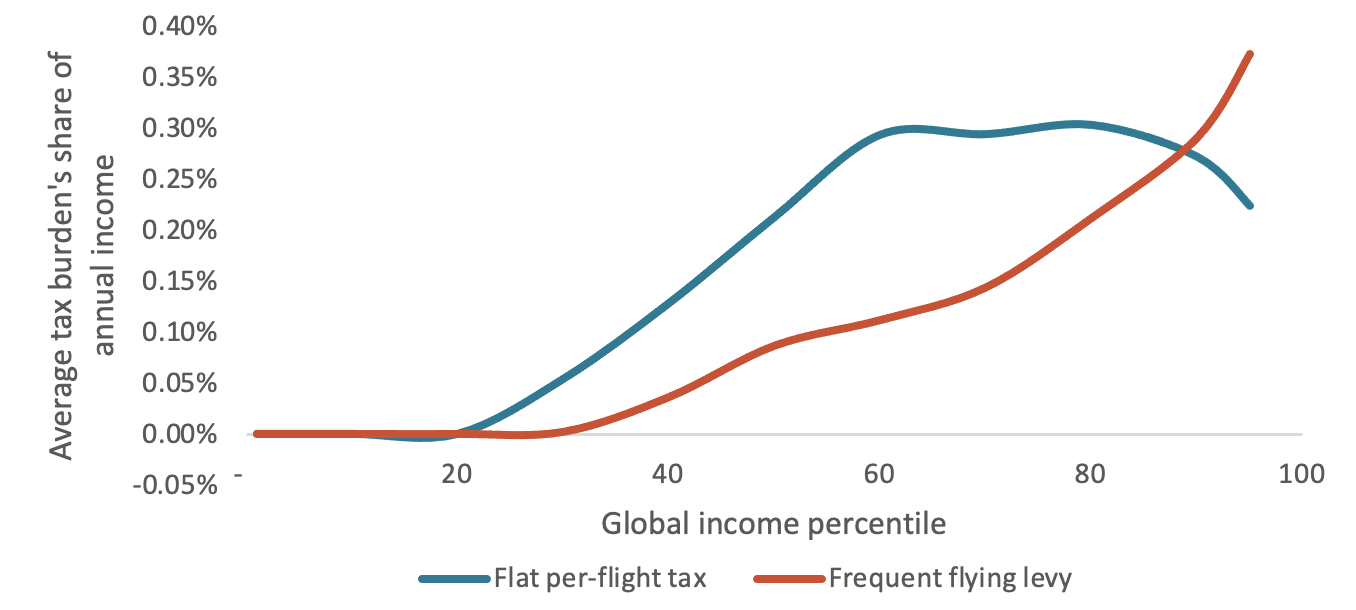

So, would a per-flight tax be progressive based on taxes paid as a share of annual income? In our FFL paper, we estimated the flying frequency of each income bracket in 178 countries, using a derived income elasticity of air travel, and created hypothetical tax schedules based on decarbonization costs. To answer the question of how progressive such a tax might be, we calculated the total flying taxes that would be incurred in a year for each bracket and the tax percentage of total income in that bracket. Figure 1 below plots the global average of annual total tax amounts’ share of individual income under both a flat per-flight tax and an FFL.

Figure 1. Modeled aviation tax burden as a share of annual individual income by global income decile.

The annual amount of flat taxes would increase from 0% of income for the bottom 20% to around 0.3% for the 60th to 94th percentiles. The tax charges taper off for the top 5% at around 0.2% of their income. An FFL would make up a significantly smaller share of annual income for the 20th to 79th percentiles and surpasses the flat tax at around the 90th percentile. The FFL would sum up to about 0.4% of annual income for the richest 5%. When the marginal tax rate increases, like an FFL, high-income individuals have a harder time offsetting the tax burden with their higher income than if there was a flat tax. Moreover, exempting the first flight from the FFL would further alleviate the tax burden for lower-income individuals. Globally, then, the progressivity of an aviation tax, especially a frequent flying levy, is rather evident.

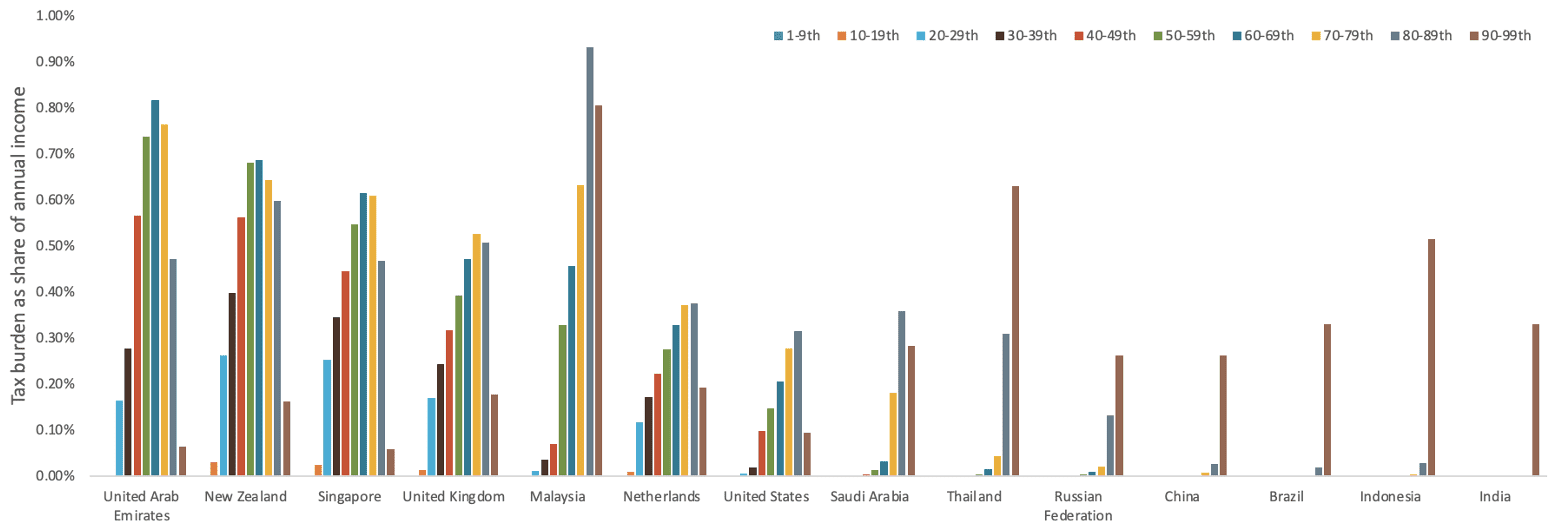

At the country level, FFL is still largely progressive, but the distribution of tax burden by income would vary greatly based on each country’s income inequality and flying behavior. Within the top 30 aviation markets in the world, there are about five different distribution patterns across their domestic income percentiles (Figure 2).

Developed markets such as New Zealand, Singapore, the United Kingdom, and the United States would see increasing FFL tax impact starting from the 20th percentile and peaking around the 50th to 60th or 70th to 80th percentiles depending on the country. The tax impact would taper off for the top 20% as their higher income outpaces the escalating levies for taking more flights. In relatively mature markets such as Malaysia, Saudi Arabia, and Thailand, tax impact would pick up around the middle brackets (40th to 70th percentiles) and peak around the 80th percentile. There is only a small dip for the top decile, and for Thailand we even start to see a larger impact for the top 10%. For the emerging markets, the distribution would be drastically different, where FFL would only affect the top 20% to begin with and the impact is much greater for the top decile than for the second. FFL would also impose a slightly bigger impact on the richest 10% in emerging markets than the richest 10% in developed markets.

Figure 2. Modeled aviation tax burden as share of annual individual income, by country-level income percentile.

The bottom line is that, regardless of the shapes of these distributions, lower-income individuals would not be paying a larger share of their income for aviation climate tax compared to higher-income individuals. This confirms the progressivity of an FFL on the level of individual countries. However, the distributions seem to suggest that the middle class in developed countries would shoulder a larger burden of FFL than the richest 20% would. If this is indeed the case, then in order to shift more tax burden to the most frequent flyers, who tend to be in the top 20% bracket, an FFL might need to escalate more drastically as flying frequency increases.

While our paper on FFL only covered scheduled commercial flights, it could be even more fair and efficient to levy taxes on private jet users. They fly more frequently and emit more carbon each trip than most commercial flyers. Since there is no ticket sale involved, climate taxation could take such forms as an annual registration fee or a straightforward tax on fuel.

One notable exception to the correlation between income and flying frequency is recent migrants, some of whom travel often despite lower incomes. Taking into consideration the travel purpose, seating class, and the traveler’s income level would further improve tax equality.

While we can be fairly confident that an aviation tax would be progressive both globally and within each country, we need to further investigate how much taxation is the most fair and efficient. The fairness and efficiency should be evaluated against those of other regulations, such as fuel-efficiency standards, and against incentives for private investments, demand management policies, and so on. Stay tuned for our upcoming research on the structure of aviation climate finance!