Blog

Green intermodal freight and unlocking solutions for China’s air and climate problems

Intermodal shipping reduces freight-related air pollutant and greenhouse gas emissions by intelligently integrating multiple transportation modes, tools, and business models and making shipping smoother, more efficient, and cleaner. Indeed, increasing “green” intermodal freight shipping centered around railroad and waterway was one of the pillars of China’s comprehensive air quality campaigns from 2018 to 2020. Then, in October 2021, when China released its national action plan to peak carbon emissions, there was much ink devoted to increasing the share of intermodal freight.

Beyond the environmental gains, establishing an efficient, clean intermodal freight system is a critical part of creating a country with a “modern, clean and low-carbon transportation system,” according to multiple guiding plans from China’s Ministry of Transportation. These include the Outline for Building a Strong Transportation Country and the Outline for National Comprehensive Three-dimensional Transportation Network Planning.

Despite all of this ambition, major bottlenecks remain. For one, China doesn’t have a system to regularly or systematically monitor and store freight activity data, especially intermodal freight data. This kind of information is fundamental for making data-informed policies.

Additionally:

- Each transportation mode is regulated and managed separately by different authorities, and there has been a lack of coordination among these agencies.

- Railroads are essentially government-run and the industry currently lacks the market motivation to support an efficient intermodal freight system.

- Regulations and market-incentive policies for advanced, clean freight technologies have been released piecemeal and do not currently send a clear signal to key market players like shippers and carriers.

- Transport nodes and hubs are still underdeveloped.

- Key operational requirements and metrics, including transport units and shipping documentation, vary by mode and are not yet standardized.

In the United States, meanwhile, intermodal shipping already has a long history. Its development and success was the result of decades of policies and policy adjustments that released the market potential of various modes and helped coordinate them. Based on our recent study and because the United States offers rich experience and lessons for China to consider, this blog post provides an overview of strategies to tackle China’s major bottlenecks.

Closely track the freight system with analytical tools to support data-driven policy

The Commodity Flow Survey (CFS) conducted by the U.S. Bureau of Transportation Statistics and the Census Bureau provides a high-level understanding of the national activity of freight transport by surveying shippers every 5 years. This data offers key insights into the performance of the transportation sector. For example, CFS data showed that intermodal carries various products and is used for long-distance shipping. In addition, the U.S. Bureau of Transportation Statistics and the Federal Highway Administration produce the Freight Analysis Framework with the support of research organizations; the tool supports national and regional freight policy and decision-making with integrated freight data from various sources.

Although the annual China Statistical Yearbook offers a high-level understanding of the performance of the transportation sector, it lacks details such as the type of commodities shipped, their origin and destination, their value and weight, and mode(s) of transport. Meanwhile, information collected from China’s ports indicates that waterway-railroad intermodal shipping carried over 6.87 million TEUs in 2020, a 10% annual growth rate from 2011, when 1.16 million TEUs were carried. Though this illustrates that China is making some good progress in promoting intermodal, the data is not comprehensive, nor is it well documented and evaluated in the freight statistical database.

Use legislation or guiding plans to ensure coordination among all transport modes

In the United States, the Intermodal Surface Transportation Efficiency Act of 1991 (ISTEA) removed barriers and promoted cross-jurisdictional collaborations among all modes of freight transport: highway, railroad, air, and maritime shipping. This was built on a series of deregulations of all modes that accelerated the marketization of freight transportation and enhanced coordination between modes and regions.

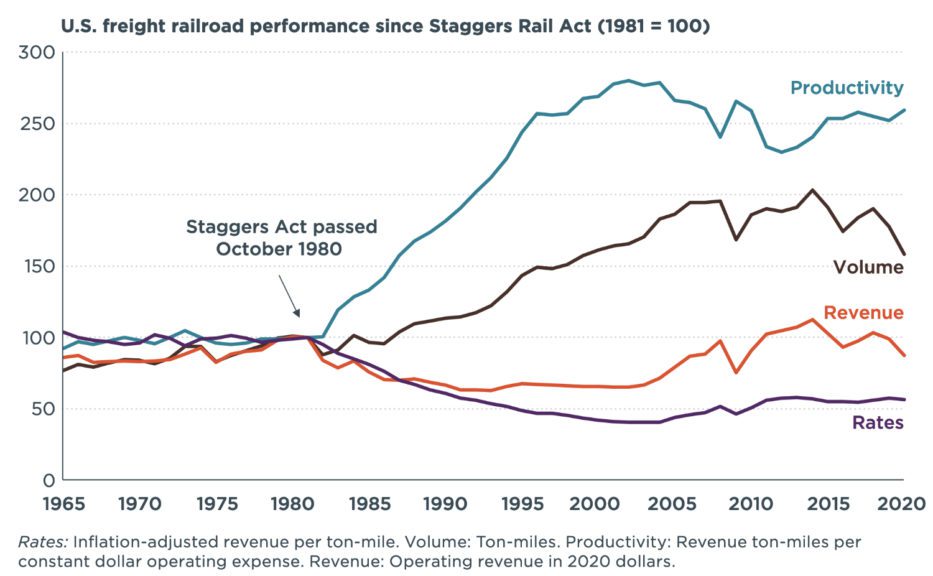

Using rail as an example of this marketization, the Staggers Rail Act of 1980 built a customer-focused, market-based approach that allowed railroads to determine the prices, routes, and services for maximum efficiency and recognized their need to earn adequate revenue. The impact on the railroad industry, which had been sliding into bankruptcy in the 1960s and 1970s, was pronounced, as illustrated by the productivity, volume, revenue, and price trends shown in Figure 1. The new structure established by ISTEA and investment in the transportation network and infrastructure ensured that the focus became the efficiency of the entire freight system. This was instead of the focus being on each mode individually, and this enhanced the ability to connect and interchange between modes.

Figure 1. U.S. railroad performance, 1964–2020. Source: Shao et al. (2022)

China has a comprehensive transportation network, hub system, and facilities planned, and thus it is imperative to ensure coordination and collaboration among different modes. The reform of all modes needs to focus on making it so that prices, routes, and services are set for improved efficiency and recognize the need to earn enough revenue to be successful. The railroad system will be a priority, given China’s goal of promoting it as the backbone of the freight system. The reform can further assist the connection of modes by reducing redundant paperwork and unnecessary administrative processes.

Use railroad and waterway to ship bulk goods

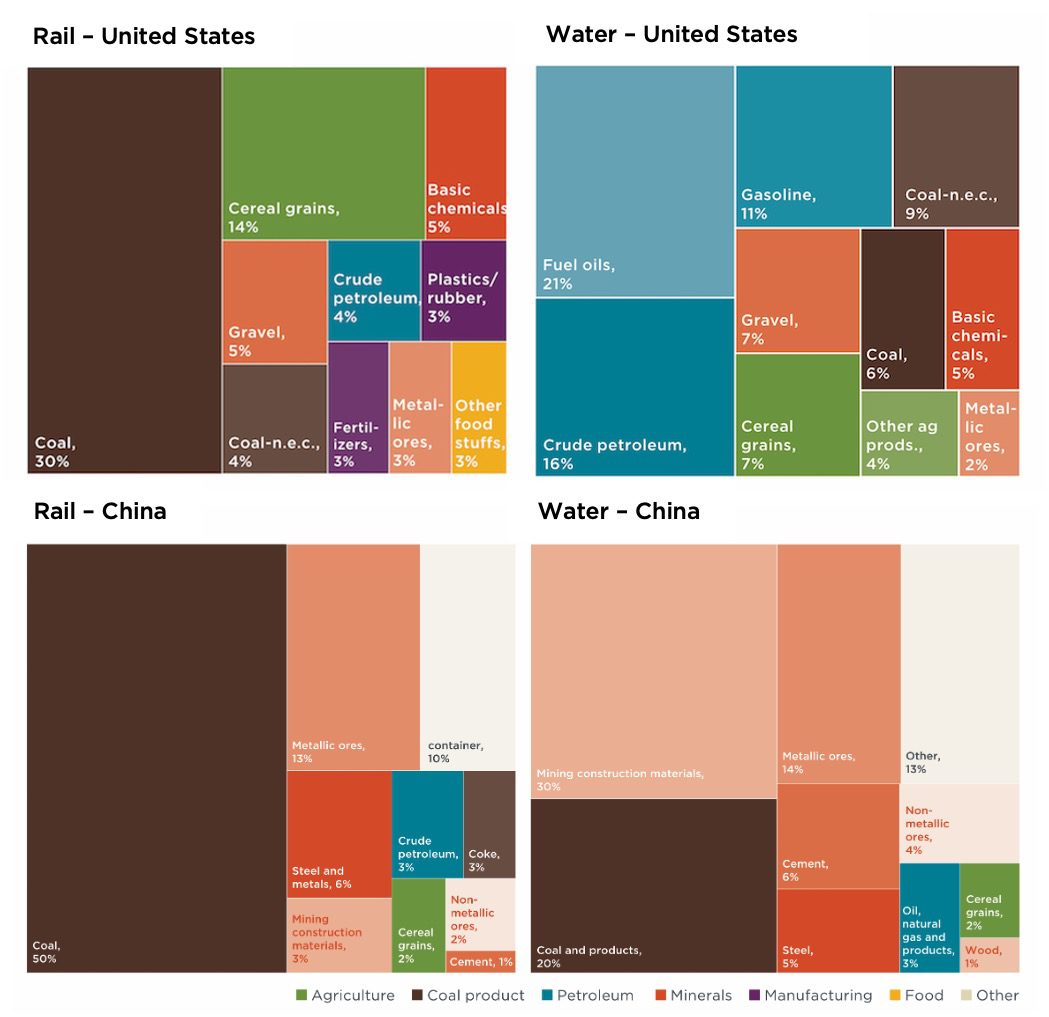

Our recent study looked at coal as an example and found that in 2018, railroads hauled about 70% of products (by weight) at least part of the way, and inland waterway shipping also accounted for around 10% of U.S. coal tonnage. Railroad and waterway also carried a wide range of products such as agricultural products, minerals, manufacturing goods, petroleum, and foodstuffs (see top of Figure 2), and these two modes are recognized for their high efficiency, low emissions, and low cost when compared with other modes.

Figure 2. Top 10 commodities by weight shipped by rail in the United States and China, 2018. Source: Shao et al. (2022)

Compared with the United States, products hauled by railroad and on waterways were limited in China. In 2018, trucks claimed almost 60% of the shipping tonnage for bulk products such as coal and iron ore. The commodity types hauled by railroad and waterway were mostly coal products and minerals. However, there’s more potential, as our case studies on motor vehicle shipping patterns suggested that the two modes could be the backbone of hauling higher-value products. With targeted regulations, the share of railroad in shipping motor vehicles in China increased from 8.6% to 29.2% and that of waterway from 8.5% to 15.1% in just 4 years, from 2015 to 2019.

Embrace cutting-edge technologies with the right policy kits

Cutting-edge technologies can accelerate a transition toward an efficient intermodal system. The invention and broad application of containers was one example that facilitated the shift to the intermodal system in the United States. Recently, technology-forcing approaches and innovative programs successfully assisted the United States in reducing air pollution and carbon emissions, and these will continue supporting the transition to zero-emission technologies.

Meanwhile, the freight sector in China has struggled to introduce advanced technologies. Using zero-emission trucks as an example, sales fell by almost 90% between 2017 and 2020, from 69,000 units to 6,700 units. In addition, China’s trucking sector is highly disaggregated, and most carriers have just a few trucks or are owner-operators. Fierce competition depresses profits and prevents investment in advanced technologies. Other factors such as split economic incentives, shortage of charging facilities, and information barriers could further delay investment in new technologies.

To build a green, efficient, intermodal freight system, China needs to continue the strategy of shipping structure adjustment, including its goal of making railroad the backbone of the system. In an upcoming blog post, we’ll elaborate on railroad freight, the most critical link in intermodal shipping, and how it can accelerate the adjustment of China’s freight system.