Investigating the U.S. battery supply chain and its impact on electric vehicle costs through 2032

Report

Assessment of U.S. electric vehicle charging needs and announced deployment through 2032

Global electric vehicle momentum continues, and with its rise comes questions of how much charging infrastructure will be needed to keep up with demand, how much is already built or expected to be built, and if that amount is enough.

This paper analyzes the increase of U.S. light-duty BEV sales and the associated home, workplace, and public charging needs through 2032 based on estimates of potential market growth from the Environmental Protection Agency’s proposed Multi-Pollutant Emissions Standards. It then compares those charging needs with a detailed examination of more than 160 announcements—made by federal and state governments, charging infrastructure providers, automakers, retail companies, utilities, and other stakeholders—about charging deployments and investments in charging infrastructure.

The paper leads to three high-level conclusions:

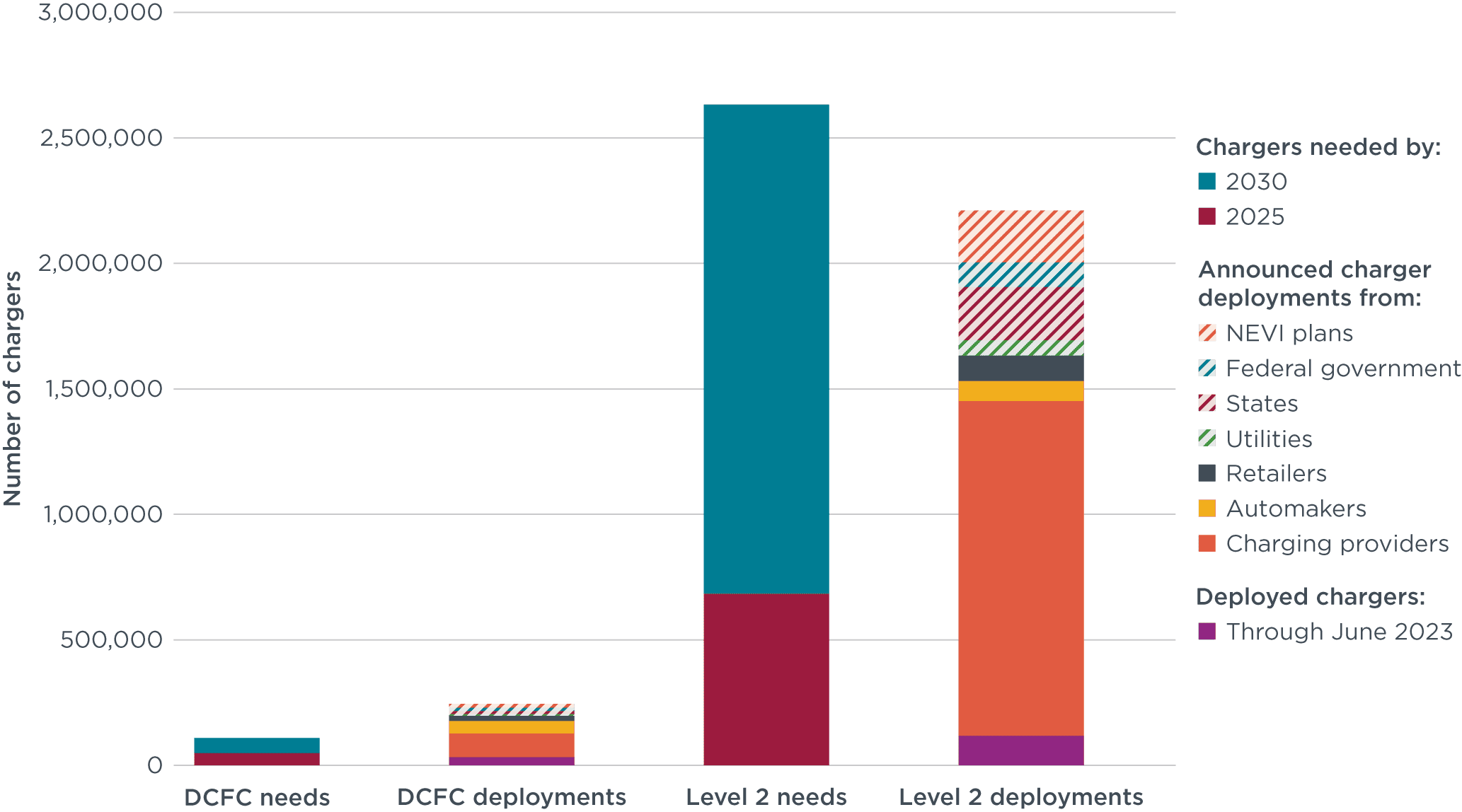

- Continued EV market growth requires continued charging deployments. The report finds that the impending BEV fleet will require about 3.7 million Level 2 chargers at public locations and workplaces, 136,000 direct current (DC) fast chargers, and 40.1 million chargers at single-family and multifamily homes in 2032.

- Millions of new chargers have been announced. Announcements by charging providers, automakers, and retailers indicate that 164,000 new DC fast chargers and 1.5 million new Level 2 chargers could be deployed at public locations and workplaces by 2030. Additional announcements by the federal government, states, and utilities could lead to potential additional deployments of 47,000 DC fast and 579,000 Level 2 chargers.

- Charging announcements cover a substantial share of the chargers needed by 2030. The combined number of existing and announced charging deployments from private stakeholders cover about 182% of the needed public DC fast chargers and about 62% of the needed public and workplace Level 2 chargers in 2030. With the inclusion of potential additional charging deployments from government and utility stakeholders, announced deployments could provide about 225% of the needed public DC fast chargers and about 84% of the needed public and workplace Level 2 chargers.

Figure ES1. Non-home EV chargers needed by 2030 compared with announced deployments

The paper finds that announced charging deployments are on track to keep up with needs from increased BEV sales. Continued commitment and collaboration among stakeholders are essential to sustain this momentum. If stakeholders fall short of their charging commitments, more chargers will continue to be needed. At the same time, it is likely that additional charging deployment will continue to be announced in the coming years, underscoring the dynamic nature of the EV landscape and the ongoing public and private sector commitments to cleaner transportation solutions.

[Press Statement] New report finds announced charging infrastructure installations are poised to keep up with an accelerated U.S. transition to BEVs