Lithium supply may far exceed demand from U.S. light-duty BEVs through 2032, new study finds

Report

Investigating the U.S. battery supply chain and its impact on electric vehicle costs through 2032

Many batteries and battery materials will be needed to supply the increased sales volumes of battery electric vehicles (BEVs) in the United States. Additionally, the auto industry will need to secure a sufficient and affordable supply to manufacture and sell BEVs at prices comparable to their combustion engine counterparts. A key challenge in this is how to scale investments in mining, refining, and battery production in the next 10 years.

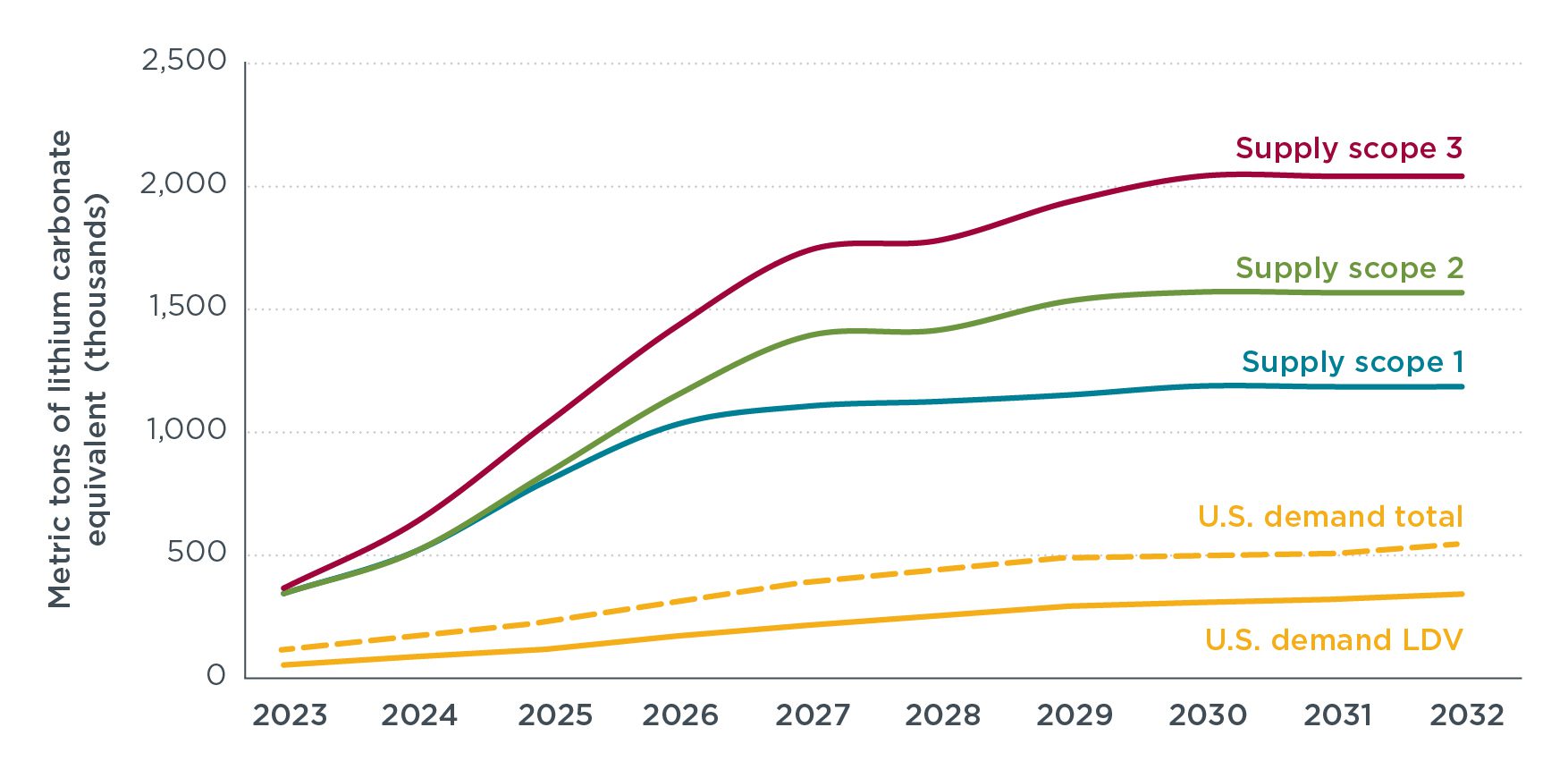

This paper analyzes key questions about the development of the U.S. battery supply chain and its impact on BEV costs through 2032. It quantifies the projected annual lithium demand for increased U.S. light-duty BEV sales to 67% by 2032, which is aligned with estimates of potential market growth from EPA’s proposed Multi-Pollutant Emissions Standard. The study then compares that demand with announcements of new and expanded lithium supply. The analysis finds that by 2032, the United States is projected to need around 340 thousand metric tons per annum (ktpa) of lithium carbonate equivalent (LCE) for new light-duty BEVs. Through identifying three potential scopes of lithium supply, the analysis finds that new lithium supply may far exceed lithium demand from new U.S. light-duty BEVs through 2032.

Figure ES1. Three scopes of announced lithium supply from United States and its existing and potential FTA and CMA partners compared to lithium demand from new U.S. light-duty BEV sales through 2032.

The study also generates hypothetical price scenarios of three key battery materials (lithium, cobalt, and nickel) and develops bottom-up battery cost analysis to identify the impact of changing raw material prices on battery and BEV costs.

The analysis leads to the following high-level conclusions:

- Over 100 new lithium mining and refining projects are underway in the United States and its existing and potential future FTA and CMA partners as of 2023.

- Battery pack and BEV costs are linked to raw material prices, but substantial continued battery and BEV cost reductions are expected under most raw material price scenarios.

- Incentives in the United States for battery production and BEV purchases accelerate the timing for purchase price parity by about three years.