Technical Brief

Zero-emission locomotive technologies: Pathways for U.S. rail decarbonization

The U.S. freight rail system, the largest in the world, carries nearly 40% of the country’s long-distance freight volume by tons per mile, primarily using diesel fuel. Emissions of criteria pollutants from U.S. freight railroads have profound impacts on local air quality and public health, leading to approximately 1,000 premature deaths and $6.5 billion in health damage costs annually. Although the sector’s contribution to total U.S. transportation-related greenhouse gas emissions (GHG) is small (~2%), this share from freight rail is expected to increase as zero-emission technologies are adopted for heavy-duty trucks.

Many countries and regions outside of the United States have committed to zero-emission railways, and overhead catenary systems have become the dominant zero-emission pathway, globally. Meanwhile, catenary systems are used for less than 1% of the U.S. rail network, largely due to the private ownership of freight railroads and the associated financial burdens of installing catenary systems. Countries worldwide have started to explore other low- and zero-emission pathways as well, such as battery-electric, hydrogen fuel-cell, and diesel-hybrid battery-electric locomotives, or a combination of catenary system with these technologies.

The United States has been recently undertaken efforts at a national- and state-level to decarbonize the rail sector, such as through incorporating rail in the U.S. national blueprint for transportation decarbonization and the adoption of California’s In-Use Locomotive Regulation in 2023.

To support U.S. rail decarbonization efforts, this technical brief provides an overview of the existing and emerging low- and zero-emission propulsion technology pathways for locomotives, showcasing the global state of development and reviews the state-of-the-art economic assessment for the technologies.

Key findings from this review include:

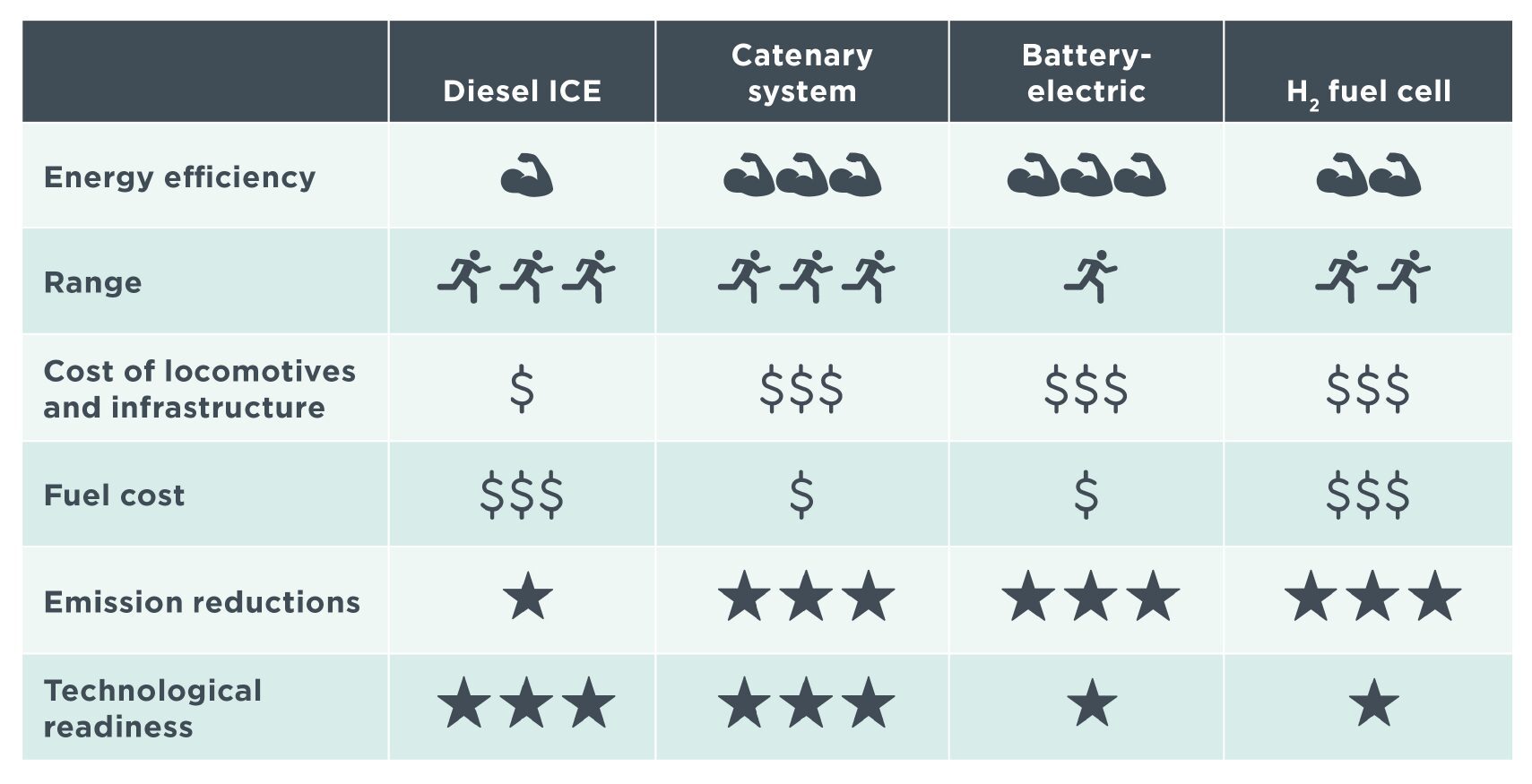

- Each of the major zero-emission technologies have specific challenges and opportunities. Hence, there is no single technological solution applicable for all rail networks and locomotive segments, i.e., freight, passenger-rail, and short-distance switchers.

- Potential interim solutions for the U.S. freight rail could include the use of partial catenary systems, which combine catenary systems with batteries, fuel-cells, or diesel-hybrid powertrains.

- The transition to zero-emission technologies could vary over the locomotive segment, considering the available technologies and relative economics, plus the extent of local air quality and related health impacts. For instance, switchers, industrial locomotives, and passenger rail segments could be prioritized for early decarbonization given that such segments operate relatively shorter distances and consume less energy than freight rail and are associated with significant local air quality impacts.

- Large gaps exist in literature regarding data and estimates for the cost-benefit or total cost of ownership of the technologies. The available estimates indicate that adopting low- and zero-emission propulsion technologies could lead to significant fuel cost savings and health and climate benefits from reduced emissions. With further technological advancement, commercial deployment, and market maturity of the technologies, the total cost of ownership of zero-emission technologies are expected to be lower than conventional diesel powertrains in the future.

Table. Qualitative performance assessment of major zero-emission locomotive technologies