Driving electrification: A global comparison of fiscal policy for electric vehicles

Blog

Electric vehicle incentives, chargers, and sales: What we see and what we don’t (yet)

In the US, ambitious state goals and national goals for electric vehicle (EV) adoption have challenged automakers and policymakers to find new ways to encourage consumers to choose EVs over conventional vehicles. In search of a formula for cost effective, widely appealing, and long-lasting EV support, local and state officials are experimenting with different combinations of a broad set of measures that range from direct rebates and perks like HOV lane access to infrastructure support to educational campaigns. At the same time, analysts (including us) are pulling together all the data we can find on policies, infrastructure, and sales to see if we can detect patterns and begin to identify the best practices in EV policy.

Our latest analysis indicates that state subsidies and non-fiscal incentives like HOV lane access are increasing EV uptake, but many other factors are also at play. A recent study by researchers at Cornell University went deeper, using three years of data on vehicle sales and public chargers across over 300 US cities (or more technically, metropolitan statistical areas) to estimate that a 10% increase in charging stations will lead to a 11% increase in EV sales. The authors apply this finding in a model that shows that federal spending on public charging infrastructure could lead to more EV sales than the same amount of spending on direct EV rebates. This is due in part to the positive feedbacks between charging infrastructure and EV purchases: people are more likely to buy an EV if they see a lot of places they could charge it, and businesses are more likely to invest in EV chargers if they see more of their customers driving EVs. Of course, more chargers help to increase the functional range and benefits of EVs, so it’s not all that surprising, but the magnitude of the impact is an important finding.

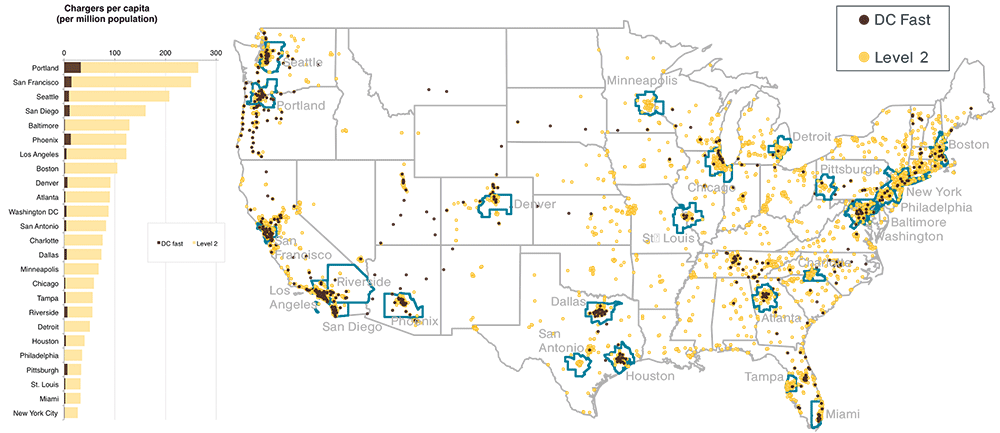

In our ongoing city-level analysis we are also finding a strong correlation between public charger availability and EV uptake in major cities. The Alternative Fuels Data Center is an excellent resource for data on current and planned EV charging infrastructure in the US, and their data show a lot of variation in charger availability across the US. Based on the AFDC data, we analyzed the chargers per capita in the 25 most populous US metropolitan areas (See the box and map, below). The top five cities in terms of EV uptake have an average of 200 chargers per million people, while the five cities with the least EV sales average only 60 chargers per million people. Even in the top five EV uptake cities, gasoline stations outnumber chargers by more than two to one. There is definitely room for a lot more investment in public charging infrastructure.

This is a useful finding for policymakers: investment in public charging matters, and may even be a better investment than direct incentives. Nevertheless, we shouldn’t fall into the trap of letting the pattern we can see most clearly – public charging is associated with high EV sales— lead us to ignore the importance of the connections we haven’t been able to quantify yet (economist Daniel Kahneman describes this sort of mistake as the error of thinking “What you see is all there is”). Other studies have pointed out that public chargers contribute less to EV charging than other charging locations, that the majority of EV charging takes place at the home, and that employees are 20 times more likely to drive an EV if their workplace provides charging facilities. The Cornell study also showed a positive effect of home charger subsidies on EV sales, and EV owners can get continued benefits from off-peak charging discounts offered by utilities. Then again, other research indicates that many prospective car buyers are unaware of the incentives and fuel-saving benefits of EVs, so there are fundamental information gaps as well.

To find the right formula for EV support, it is important to keep tracking the actions of different city and state players – including public officials, utilities, and workplace charging partners– in supporting public charging infrastructure, providing various consumer incentives, and information resources. As the EV market matures and we see sales shift in different areas, a broad view of the policy landscape can help us pick out the most critical policies and also find important interactions among different policies. For now, we’re not ready to rule anything out.