Charged up, ready to go! After some delays. How it is to buy an electric car these days.

Blog

Revamping the federal EV tax credit could help average car buyers combat record gasoline prices

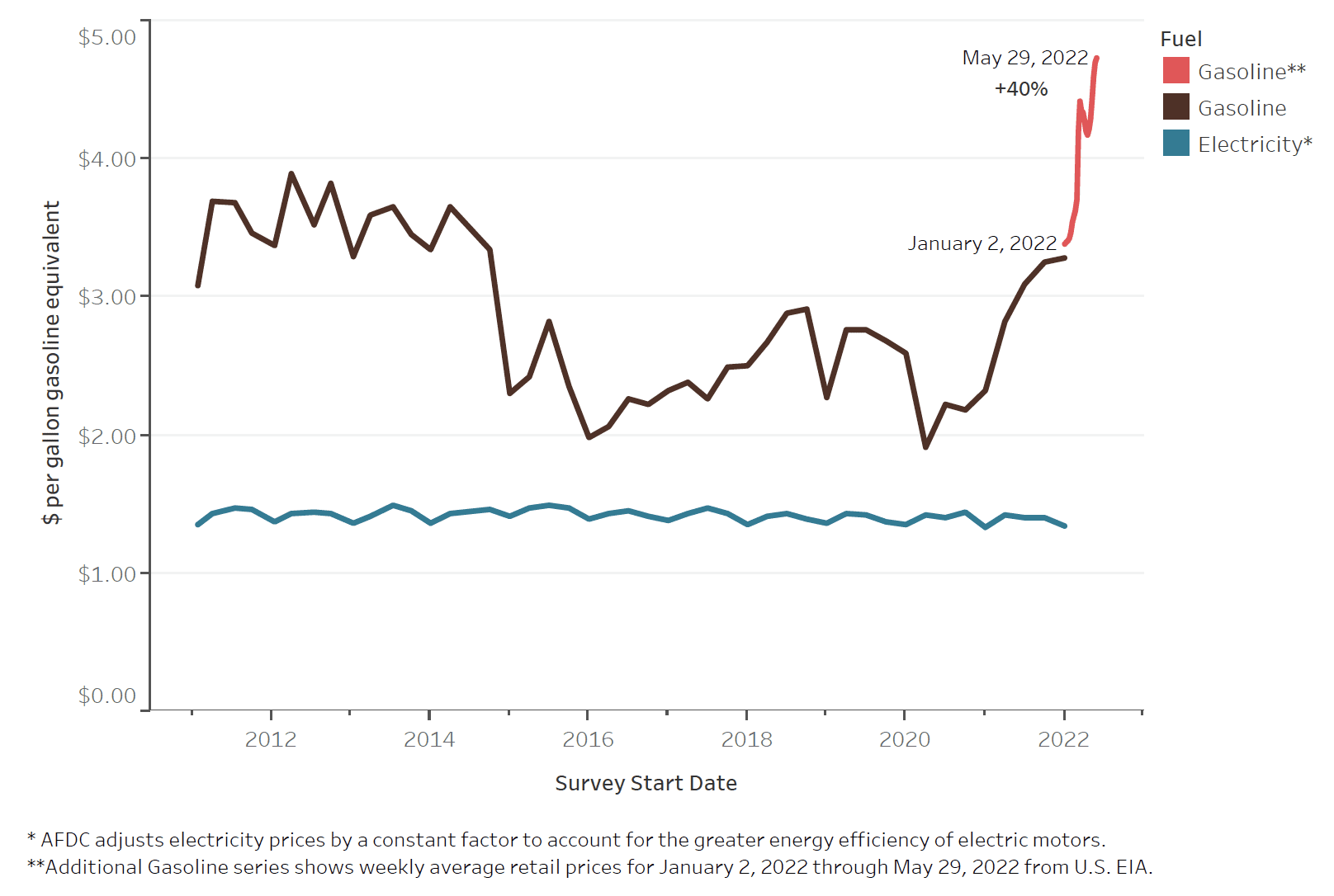

At the end of May, U.S. retail gasoline prices hit another record high in nominal dollars. That they’re still below their July 2008 peak when adjusted for inflation offers little consolation to people grappling with an 8.3% increase in the consumer price index in April compared to 12 months earlier. It’s small wonder then that inflation in general, and gasoline prices in particular, are top economic priorities of the Biden Administration and Democrats in Congress.

As it happens, the opportunity is there to connect those priorities with two others of the administration’s central policy goals: radically and rapidly reducing the nation’s greenhouse gas emissions and increasing sales of electric passenger cars and light trucks—the latter not only a key to reducing transportation emissions but also an objective that can help reinvigorate American manufacturing. That opportunity is to extend the federal $7,500 electric vehicle tax credit. The current credit is tied to a manufacturer’s total EV sales. For some (GM, Tesla) it has already expired, and it will soon for others (Ford, Toyota). Senate Democrats and Biden Administration officials have a critical opportunity to revamp the credit industry-wide as part of the budget reconciliation working its slow way through Congress now.

EVs are much cheaper to operate than gasoline vehicles. In large part that’s because the price of fuel for them—electricity—is a lot lower than the price of gasoline after factoring in the greater efficiency of electric motors (see chart). A typical first owner of an EV will save several thousand dollars in fuel costs. The price of electricity is also a lot less volatile. Both are good things in a period when general price inflation has again become a kitchen-table concern.

Figure 1. Average retail fuel prices in the United States. Sources: Alternative Fuels Data Center and U.S. EIA

But EVs are not as cheap to buy as gasoline cars—not yet, at least, though that time is likely only several years away. It takes money to make money, the saying goes. It takes money to save money, too. The day-to-day cost savings of an EV are out of reach of people who can’t quite manage the upfront price. The $7,500 federal EV tax credit has been a mainstay of U.S. electric vehicle policy for the past decade, stimulating EV sales by reducing the difference in purchase price compared to conventional vehicles. It could be even more important, and effective, in the coming years. By the end of this decade, 2030, the U.S. EV market has to expand from early adopters to the average vehicle buyer if we’re going to decarbonize road transport quickly enough to match either our climate or our manufacturing goals. In 2021, EVs made up 4% of U.S. passenger light-duty vehicle sales. That share will have to quadruple from 2021 to 2026, to around 17%, then increase 8 percentage points each year to meet Biden’s goal of 50% EV sales by 2030. And to reach a level compatible with achieving the Paris goal of limiting warming to below 2°C, EV sales must grow even faster, reaching 65% in 2030 and 100% in 2035.

For many consumers, a few thousand dollars in purchase incentives can make the difference in whether they are able to afford an EV. Research on the effectiveness of California’s Clean Vehicle Rebate program found that more than 90% of rebates for model year 2019 vehicles were claimed by buyers of EV models priced under $40,000, and more than half of survey respondents who received 2019 rebates indicated they “would not have purchased/leased their EV without the state rebate.”

We compared the top-selling gasoline car in the U.S. in 2021 (Toyota Camry) against a similar battery-electric vehicle (Chevy Bolt) and found the EV price premium before incentives is $5,655. Renewing the federal tax credit would not only eliminate that price premium but make it cheaper to buy the EV—and allow a wider swath of consumers to realize the immediate savings on day-to-day operating costs.

Yet in its current form, the federal credit automatically phases out a little more than a year after an automaker sells 200,000 EVs, and GM has already reached that cap. So, this example illustrates not only how extending the credit could work to the benefit of American consumers, but also one way that it could be made more effective, by doing away with the sales cap.

There are other ways as well that the credit could be made more helpful to consumers. Currently, the credit is non-refundable, meaning the EV buyer has to have enough tax liability to be able to claim the full credit amount. And the credit is not available as a rebate, meaning EV buyers may have to wait a year or longer after the point of sale before they see it show up in their bank accounts. Both of these provisions limit the opportunity of low- and moderate-income vehicle buyers to take advantage of it. Reforming these elements of the federal EV tax credit would deliver on the Biden Administration’s commitment to equal opportunity while contributing to prudent environmental and economic policy.

The federal EV tax credit was created in different circumstances than today’s. The EV market barely existed, and the credit needed to stimulate interest from early adopters—by definition a smallish group for any new technology. It helped to do that, and now the EV market is poised to take off. Now the need is to grow that market from early adopters to average vehicle buyers. As circumstances have changed, there are actions that can and should be taken to both enhance the effectiveness of federal dollars and contain the cost of the program. One is to limit credit eligibility to EVs below a certain sales price, which could be different for cars and light trucks. Several state rebate programs have already implemented MSRP caps, ranging from $42,000 to $60,000, prioritizing incentive dollars for EV models that are most affordable to the average vehicle buyer. Another is to reduce the incentive amount over time across all manufacturers to approximately match reductions in EV costs. For example, the total incentive amount could start at $7,500 in 2022 and decline by $1,000 each year until it phases out in 2030. Phasing out the incentive over time would be less disruptive to the EV market compared to an all-or-nothing approach organized by manufacturer. Third, in light of the aim to equalize the opportunity to purchase EVs, lawmakers could increase the rebate amount available to lower-income households. For example, California’s program increases the standard rebate amount by $2,500 for consumers with household incomes below 400% of the federal poverty level.

The federal EV tax credit is not yet an idea whose time has passed. Just the opposite. It’s a double-edged policy tool that will advance key environmental and economic aims while helping pretty ordinary Americans deal with rising gasoline prices and a rising cost of living. Now is the time to extend it, with prudent changes, as part of the reconciliation package.