Driving electrification: A global comparison of fiscal policy for electric vehicles

Blog

If subsidies are no panacea, how to incentivize electric vehicles in China?

Even with more than 17,500 electric vehicles (EVs) sold in 2013, China is among the slower EV markets of the eleven examined in a recent ICCT study: light-duty EVs amount to less than 0.1 percent of new passenger vehicle sales in China’s huge and growing auto market. Among those light-duty EVs, battery electrics (BEVs) dominate, compared to plug-in hybrid vehicles (PHEVs), accounting for more than 80% of EV sales. What’s more, the majority of the Chinese EV fleet is comprised of government fleets and taxis rather than private cars. This is quite different from other markets where EV sales come from either private purchases or company purchases for private use (as is common in European countries).

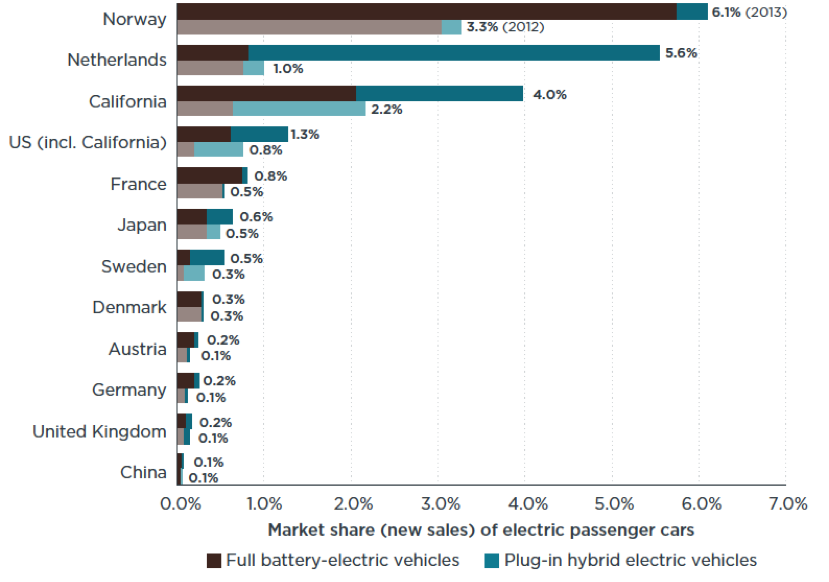

Market share of electric passenger cars for the years 2012 (lighter colors) and 2013 (darker colors), in comparison to total sales

For this study, we looked at differences in the fiscal policies used to support electric vehicle sales in China, Japan, the United States, and eight European countries. The policy incentives investigated include direct consumer subsidies, reduction in or exemption from taxes paid at time of purchase or annually, and fuel cost savings from switching to electricity and EV efficiency improvement. We evaluated two representative vehicles, the Renault Zoe BEV and the Volvo V60 PHEV, to demonstrate the key role played by fiscal incentives in spurring electric vehicle markets. Norway and the Netherlands are prime examples of the relationship between fiscal incentives and electric vehicle sales. As the global frontrunner, Norway’s EV sales accounted for 5.6% of all new car sales in 2013, and about 15% in the first quarter of 2014. Its EV market is similar to China’s, in that BEVs dominate.

Subsidy programs for new energy vehicles and energy-saving and cleaner vehicles have been in place in China since 2010 [.pdf]. New energy vehicles, including BEVs and PHEVs, are also exempted from an annual “vehicles and vessels” fee. Despite relatively high incentives, electric vehicle sales and market growth rate are still very low in China. Our report attempts to explain why this is so.

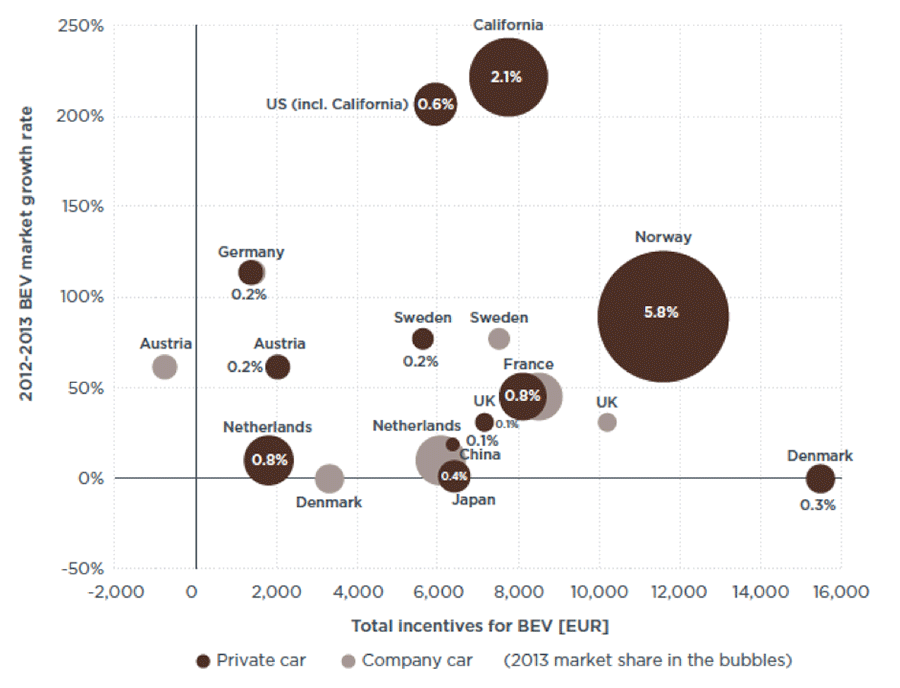

BEV Market growth rate vs. per-vehicle incentive for BEV (Renault Zoe), private and company cars, 2012–2013

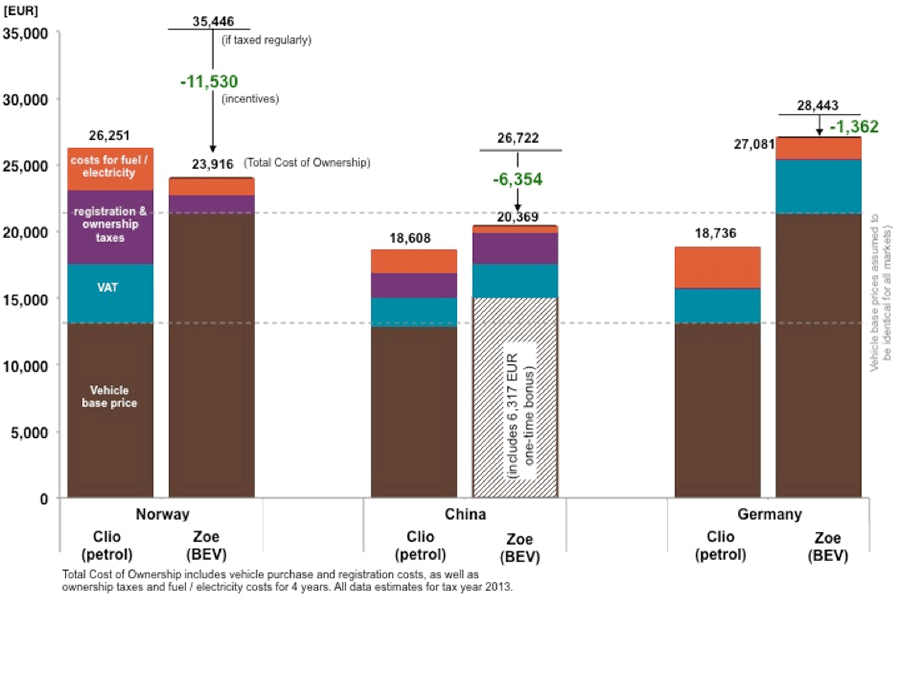

The figure below breaks down the cost of the Renault Zoe (BEV) and Clio in Norway, China, and Germany, as representative examples, to demonstrate the large differences in the level and type of fiscal incentives for electric vehicles. To ensure fair comparison, the vehicles are assumed to be available in all countries at identical base prices (excluding value-added tax, “VAT”), and annual taxes and fuel/electricity cost are included for a time period of four years. All data estimates are for tax year 2013.

The incentive provided by Norwegian government, for example, on a typical BEV amounted to approximately 97,000 RMB (11,500 Euro) per vehicle, or more than half of the vehicle base price. That incentive took the form of full exemptions from VAT, registration, and annual vehicle taxes. In Germany, by contrast, owners of electric vehicles ended up paying more taxes than they would have owed on comparable non-electric combustion engine vehicles, as the minimal current tax exemptions offered there are more than fully offset by the higher VAT that generally applies to electric vehicles. Neither of these two countries provides direct subsidies to EV, but the tax scheme and fuel/electricity cost could also make significant difference in the total cost of the purchase of an EV.

The incentive provided by the Chinese government is relatively moderate, with a small portion coming from the exemption from the vehicle and vessels fee and a large sum of one-time subsidies for new energy vehicles and energy saving vehicles. Nevertheless, the incentives are not enough to offset the higher base price, excise tax, and acquisition tax [.pdf] of the example BEV in the study. In other words, the total cost of ownership over the first four years of BEV operation is higher than a comparable gasoline vehicle in China, whereas the reverse is true in Norway.

Comparison of total cost of ownership for a Renault Zoe battery electric vehicle and a Renault Clio gasoline vehicle for Norway, China, and Germany.

Moreover, note that the two example vehicles in the study are available exclusively in European market in real world. Unlike the European market, price differences between electric vehicles and comparable non-electric combustion-engine vehicles are much greater in China. For example, the base price of the BAIC E150 (battery electric vehicle) excluding VAT is about 130,000 RMB (16,000 Euro), higher than the conventional BAIC E series vehicle, while the BYD F3DM (plug-in hybrid vehicle) is about 100,000 RMB (12,000 Euro) more expensive than the conventional BYD F3. By contrast, the price gaps between the Zoe and the V60 and their conventional-vehicle counterparts are around 70,000 RMB (8,000 Euro). Thus, even taking into account additional subsidies provided by some city governments (e.g., Beijing, Shanghai, Guangzhou), the incentives available in China still do not offset the higher total cost of operation of EVs there.

The study also shows that a number of factors in addition to fiscal incentives are influencing development of the market for electric vehicles. An example is California, where BEVs have a higher sales-growth rate and market share than other markets with the same level of fiscal incentives due to many non-fiscal consumer incentives which are not quantified in the study. BEVs and PHEVs are permitted in high-occupancy vehicle lanes, a significant incentive in congested metropolitan areas. The Zero Emission Vehicle program effectively spurs EV sales from manufacturers side. Other aspects of California EV deployment plan include charging infrastructure investments, electric utility actions, consumer awareness campaigns, and municipal-level initiatives. Norway also provides many additional incentives, such as free parking, free toll road, and access to bus lanes, in addition to the high incentives already be quantified in the study.

There is no question that fiscal incentives and differences in fuel and electricity prices do not tell the full story. Large subsidies may not be a panacea. The State Council of China set ambitious goals for EVs in 2012: cumulative BEV and PHEV sales/production of 500,000 units by 2015, and 2 million by 2020. But 2013 EV sales for private use were below expectations. Things may have started to turn around, as a slew of city-level incentives have led to a 120 percent growth in the first quarter of 2014 compared to 2013. Obstacles such as inaccessible charging infrastructure, lack of electric grid infrastructure readiness, and limited EV models eligible for local subsidies remain. To accelerate EV sales more effectively, China needs a better understanding of the roles of different incentives and the corresponding market response. A comprehensive EV strategy must support not only the early adopters but also a long-term transition to a mature mass market.