Cost of renewable hydrogen produced onsite at hydrogen refueling stations in Europe

Blog

Can the Inflation Reduction Act unlock a green hydrogen economy?

The U.S. Congress passed the Inflation Reduction Act (IRA) in the summer of 2022, combining a wide array of clean energy tax incentives into a single bill. Under this new law, an estimated $369 billion will be spent addressing energy security and climate change over the next 10 years. A key component of the IRA is a lucrative set of tax credits intended to accelerate the deployment of clean energy technologies such as green hydrogen. This financial support has also brought some vehicle makers off the sidelines and into the clean transportation arena, with a few even planning to scale up hydrogen vehicle manufacturing and build new infrastructure. Green hydrogen made from renewable electricity has gained widespread attention due to its potential to decarbonize transportation, including road, aviation, and shipping, as well as industry, but cost is a major barrier to its deployment. Can the IRA’s tax credits level the playing field, reducing the cost of green hydrogen enough to fuel a meaningful share of the transport sector?

The IRA expanded tax credits for renewable electricity and created new provisions for clean hydrogen. Under the law, renewable electricity and clean hydrogen plants in 2023 can receive a production tax credit of 2.6 cents per kWh and up to $3 per kg of hydrogen, respectively, for the first 10 years of operation (their lifetimes are typically up to 30 years). However, the tax cuts run only through 2032, so projects starting up in 2023 would benefit from the full 10-years’ worth of credits, while plants opening later would receive progressively less.

The IRA’s provisions are generous for green hydrogen producers in several ways. First, producers of green hydrogen made from renewable electricity qualify for both tax credits. In addition, the hydrogen tax credit is “direct pay” for the first five years of operation, meaning that clean hydrogen producers can claim a tax refund equal in value to their tax credits for five years. Furthermore, both renewable electricity and clean hydrogen producers can benefit from tax “transferability”—producers with no tax burden can sell their tax credits to a buyer who owes taxes.

To assess the impact of the IRA on green hydrogen production costs, we modeled two scenarios—a baseline case with no tax credit for renewable electricity or hydrogen, and a case in which the IRA tax credit provisions apply. Details of the two scenarios are shown in the table below. The effect of the tax transferability provision is still uncertain, but our analysis assumes that its value needs to be discounted because it is a market-based solution that will likely factor in legal and due diligence costs. We estimate the green hydrogen production cost using a discounted cash flow model that calculates the current value of investing in a green hydrogen plant by accounting for future cash flows. (Details on modeling assumptions can be found in a previous ICCT study.) In other words, the model estimates the green hydrogen production cost of a new plant constructed in a specific year, factoring in any applicable IRA provisions.

Table 1. Benefits of the IRA for producers of renewable electricity and of green hydrogen under two scenarios

| Renewable electricity production | Green hydrogen production | |||

| Baseline Scenario | No tax credit | No tax credit | ||

| IRA tax credit, and applicable statute | 2.6 cents per kWh in 2023, with an inflation adjustment of 2% per year in future years | Section 45 and 45Y | 3 USD per kg in 2023, with an inflation adjustment of 2% per year in future years | Section 45V |

| Applied to first 10 years of operation, and expiring in 2032 | Applied to first 10 years of operation, and expiring in 2032 | |||

| Non-refundable through tax credit years | Section 6417 | Refundable through first 5 years of operation | Section 6417 | |

| Transferable at a 15% discount through tax credit years | Section 6418 | Transferable at a 15% discount after first 5 years of operation, until 2032 | Section 6418 | |

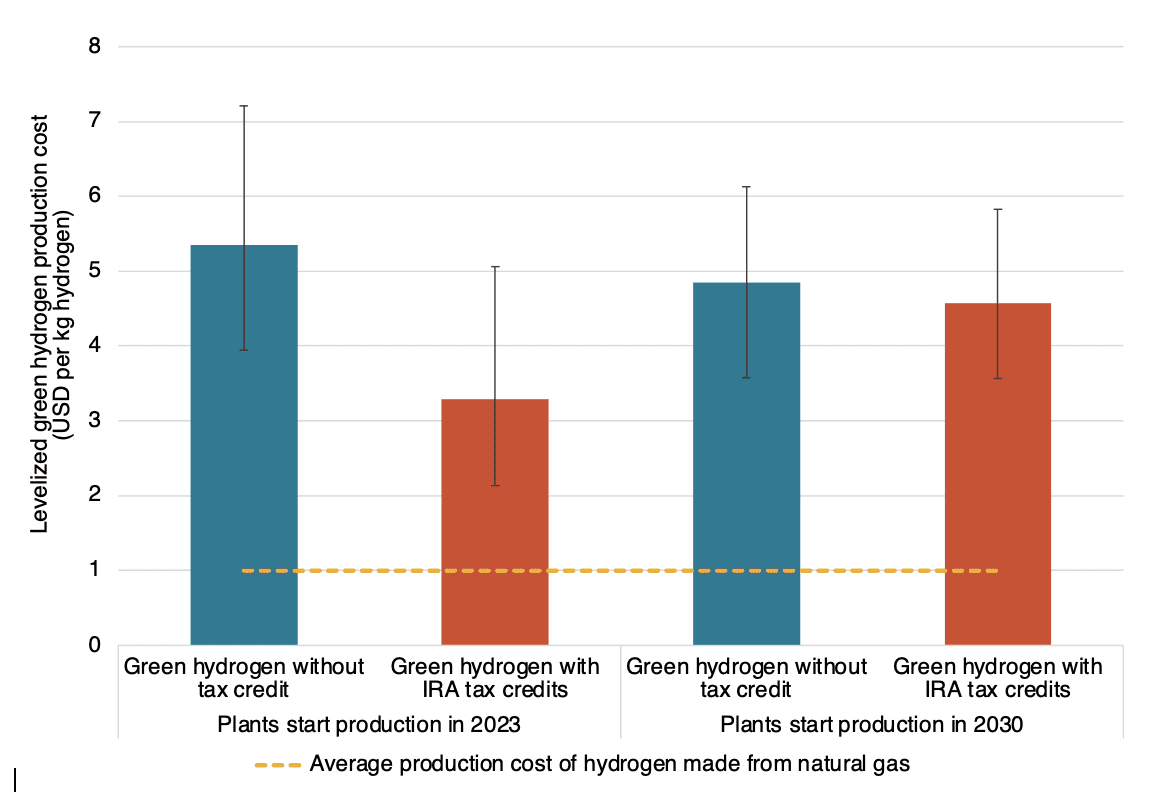

Figure 1 shows the modeled production cost of green hydrogen with and without IRA tax credits for a new project built in 2023 or 2030. The error bars indicate the possible cost range due to regional variations in renewable resources and uncertainties in electrolyzer costs. On average, the IRA tax credits for renewable electricity and clean hydrogen can reduce the cost of green hydrogen production by almost half, falling to nearly $3 per kg hydrogen for a project starting in 2023. The credits’ impacts fade steadily after 2023, until they expire in 2032. A project coming online in 2030 would qualify for only three years of tax credits, resulting in a mere 6% cost reduction compared to the no-credit scenario.

Figure 1. Modeled production cost of green hydrogen with and without IRA tax credits for a new project built in 2023 or 2030

Even with the IRA tax credits, green hydrogen is likely still at a market disadvantage given that the current production cost of hydrogen made from natural gas is only about $1 per kg without incentives. (The dotted yellow line in the figure.) The U.S. Department of Energy (DOE) sets a similar cost target for green hydrogen at $1 per kg by 2030 (an interim target of $2 per kg by 2025); however, even regions with abundant solar and wind resources (the lower end of the error bars) still fall short of those targets.

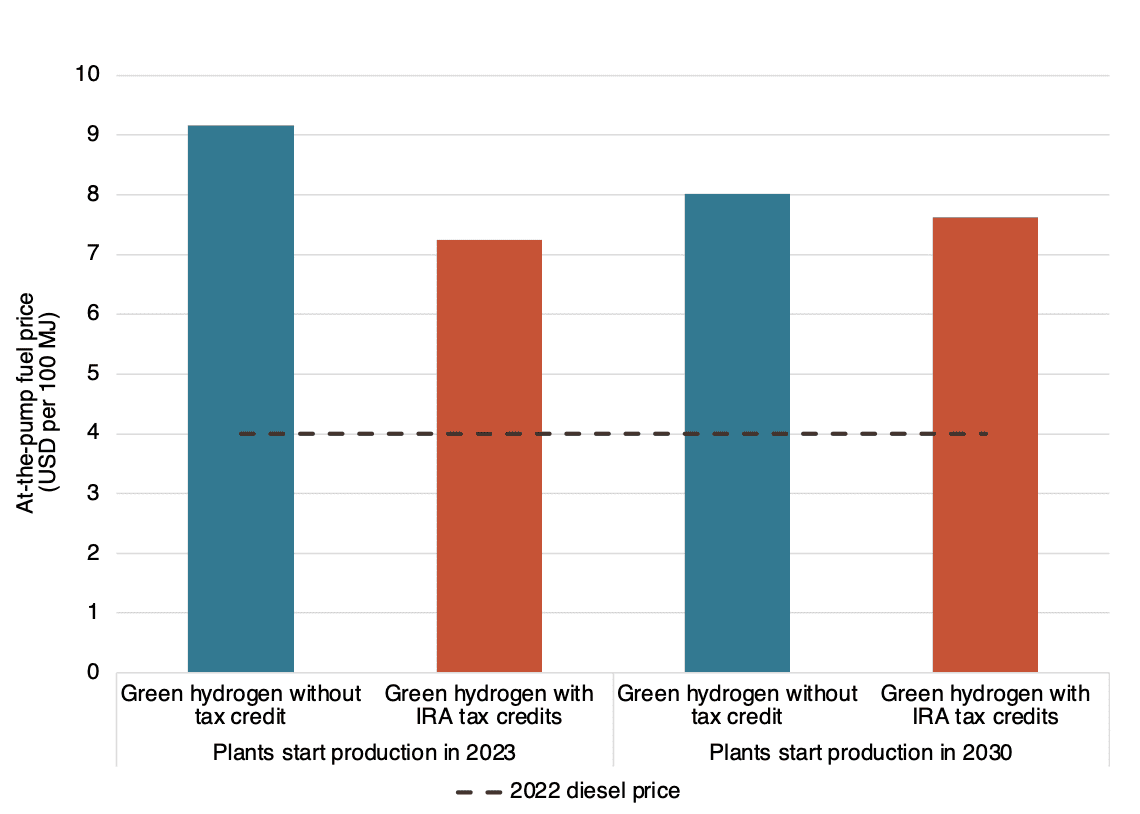

Factors beyond production costs should also be considered for a full understanding of establishing a green hydrogen economy. Depending on where hydrogen is produced and how it is consumed, distribution and infrastructure costs could drive up hydrogen prices. Taking the road sector as an example, building and operating a hydrogen fueling station would add roughly $6 per kg hydrogen, resulting in a price of at least $9 per kg for hydrogen fuel, even accounting for the IRA credits. This at-the-pump price is more than double the current diesel retail price in the United States on an energy basis, as shown in Figure 2 below.

Figure 2. At-the-pump price of green hydrogen with and without IRA tax credits for a new project built in 2023 or 2030.

To be fair, such a comparison should also account for the greater efficiency of hydrogen fuel cell vehicles (FCVs), which are 1.4 times more efficient than long-haul trucks. Yet even after incorporating vehicle efficiency into the formula, the fuel cost of green hydrogen is still higher than diesel. In addition, the vehicle cost of FCVs can double the cost of diesel trucks.

Another key consideration for the hydrogen economy is energy efficiency; turning renewable electricity into green hydrogen results in conversion losses of approximately 30%. This difference can be compounded on the user side. Depending on the vehicle type, battery electric vehicles can be 1.4 to 2.5 times more efficient than FCVs. Therefore, even if green hydrogen were to dominate the hydrogen market, it would still face the challenges of competing with other fuels from the user side.

The IRA is sending a promising signal on green hydrogen. The tax credits provided in the IRA can reduce green hydrogen production costs by half for plants that take advantage of the full set of tax credits coming online this year. However, a green hydrogen economy remains far from reality in the United States; even with the tax credits, green hydrogen is not a silver bullet for every sector. Due to high costs and conversion losses, green hydrogen probably makes the greatest economic sense for end uses that are challenging to electrify directly, such as industrial uses and long-haul aviation and shipping.