Blog

Incentivizing zero- and low-emission vehicles: The magic of feebate programs

Feebates, also called bonus-malus programs in some regions, levy a fee on the purchase of vehicles with high carbon dioxide (CO2) emissions and use the revenues to incentivize the purchase of vehicles with zero or low CO2 emissions in the form of a rebate. Thereby, governments can help to spur the transition to zero- and low-emission vehicles while disincentivizing the purchase of vehicles with the highest CO2 emissions. Differing from programs that only rely on incentives, feebates can be designed to be revenue neutral. So, what can other governments take away from established CO2-based feebates? To answer this question, let’s have a look at how feebates have been implemented for cars registered as of June 2022 in France, Singapore, Sweden, and New Zealand.

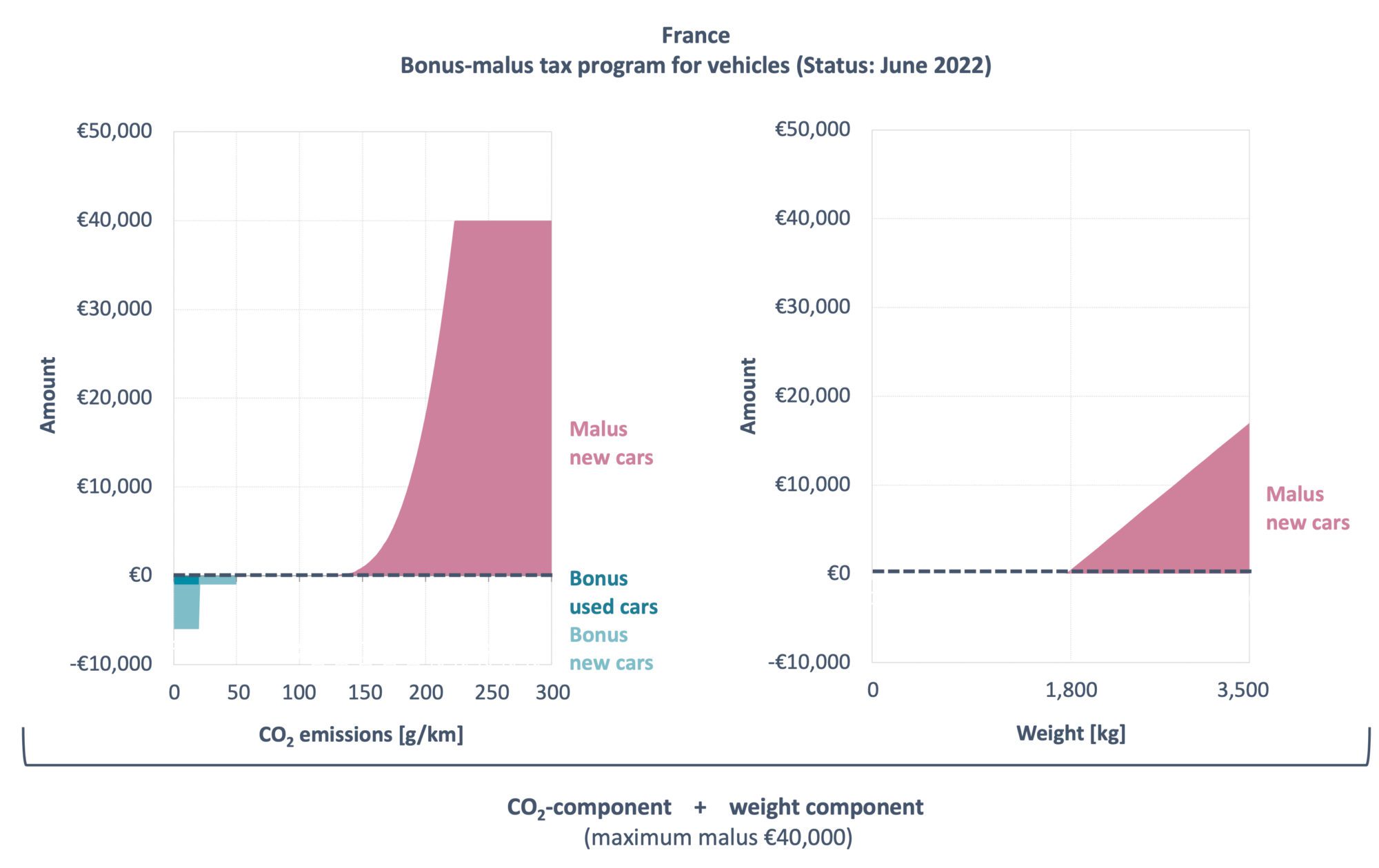

France has the longest experience with a bonus-malus system, having established its program over 14 years ago. It applies to new and newly imported cars and vans, and the amounts are calculated based on CO2 emissions and, since 2022, also on weight for passenger cars. As shown in the figure below, the bonus for new passenger cars with official CO2 emissions of 0 g/km is €6,000, while it is €1,000 for cars with emissions up to 50 g/km. The malus tax applies to vehicles emitting 128 g CO2/km or more and ranges from €50 to €40,000. The weight component of the malus is €10 per kg for cars weighing between 1,800 kg up to 3,500 kg, exempting battery electric vehicles (BEVs), fuel cell electric vehicles (FCEVs), and plug-in hybrid electric vehicles (PHEVs) with an all-electric range of more than 50 km. In addition to new cars, a €1,000 bonus applies for purchasers of a used BEV and FCEV at least two years old registered for the first time in France.

Figure 1. Bonus-malus tax program for passenger cars in France.

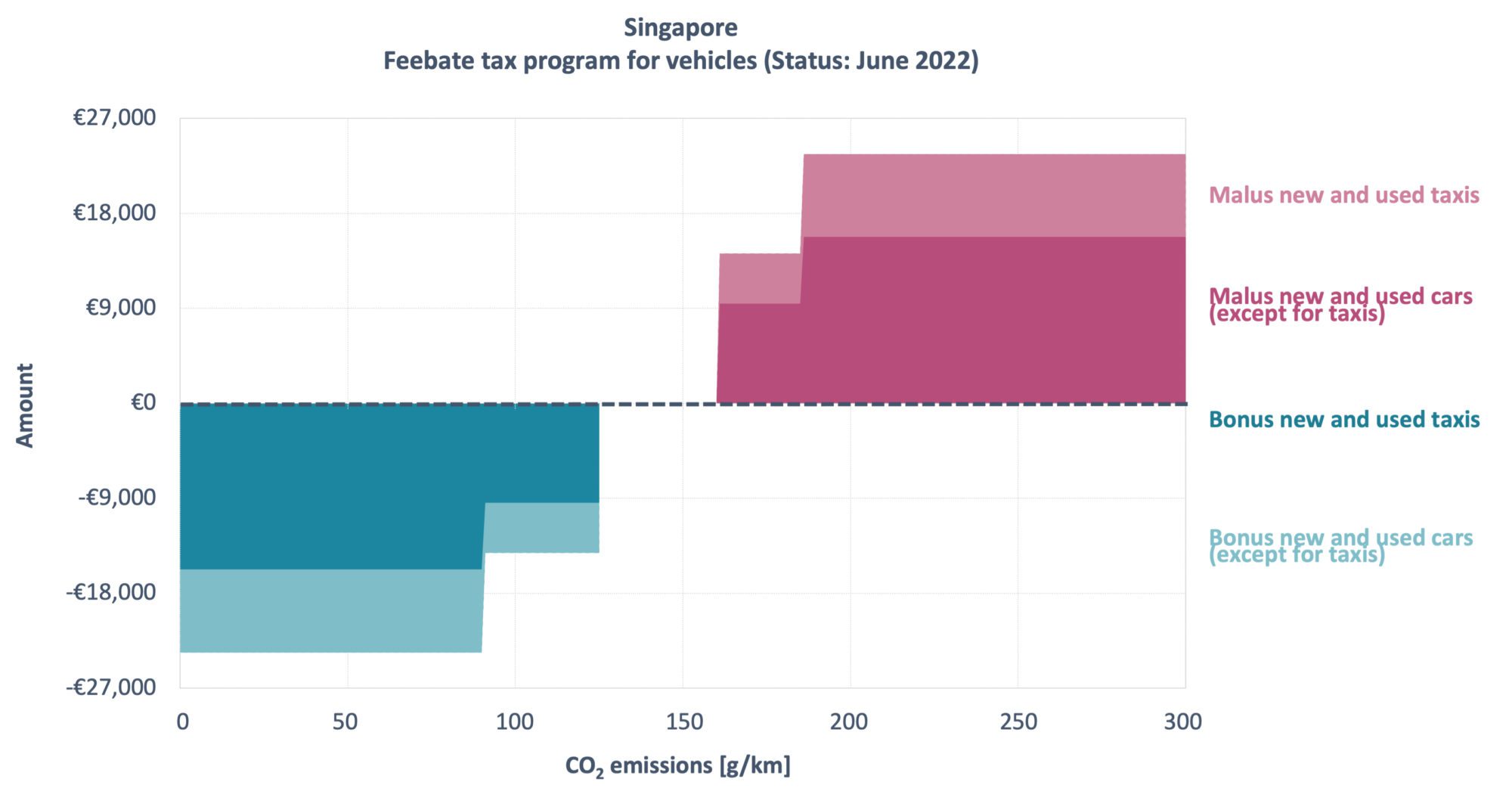

Singapore’s feebate has been around for over ten years and applies to new and newly imported used vehicles registered for the first time in Singapore. Rates, which are higher for taxis, depend on CO2 emission levels in addition to other pollutants. The rebate for cars other than taxis is SG$25,000 (€15,800) if official CO2 emissions range between 0 and 90 g/km. Cars emitting between 91 and 125 g CO2/km receive a rebate of SG$15,000 (€9,500). The fee for higher emitting vehicles is SG$15,000 (€9,500) for cars with CO2 emissions between 161 g/km and 185 g/km and above emission levels of 185 g CO2/km, the one-time fee SG$25,000 (€15,800). As shown in the figure, rates are applied according to a step function, in contrast to the French system which calculates the malus according to a progressive function.

Figure 2. Feebate tax program for passenger cars in Singapore.

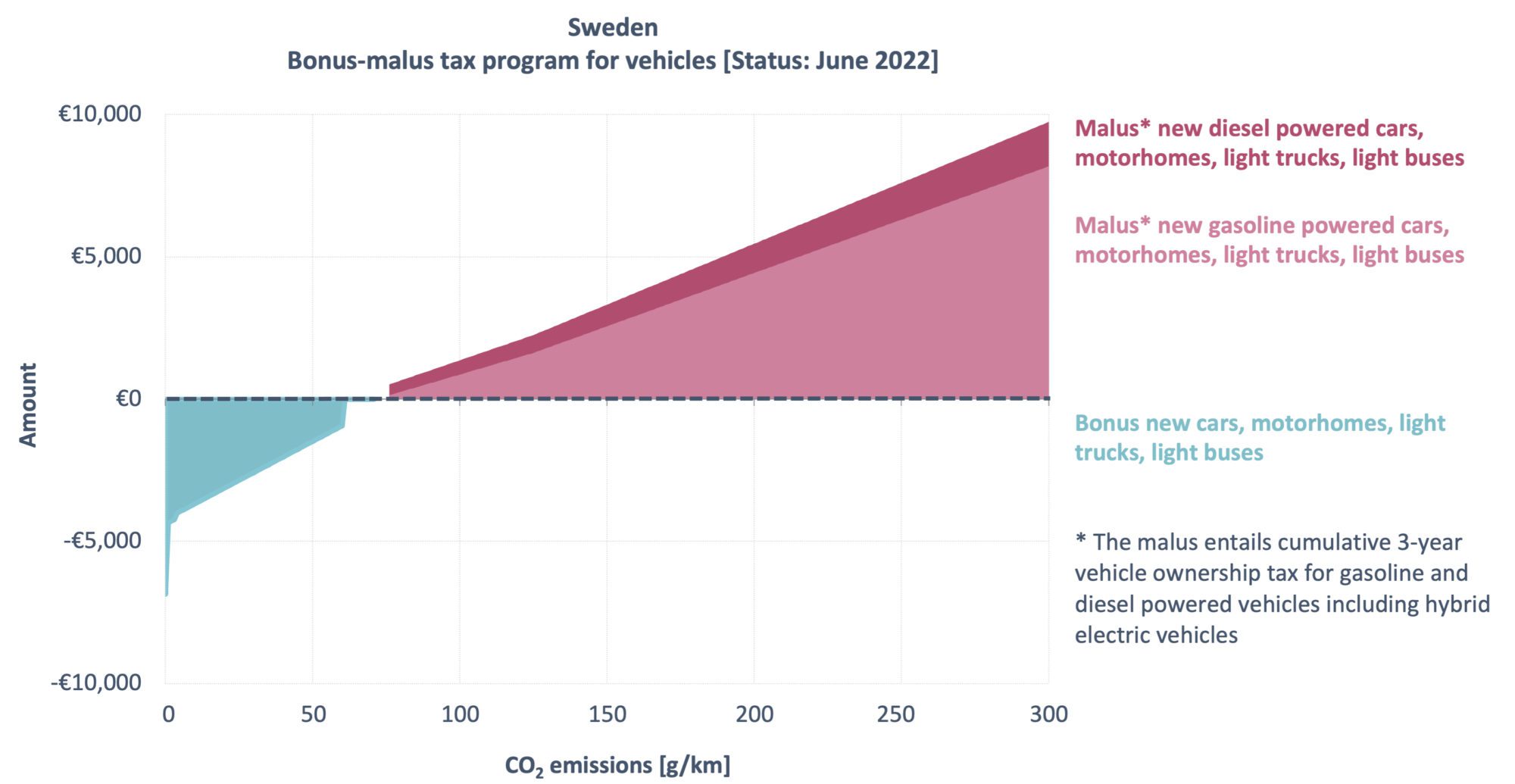

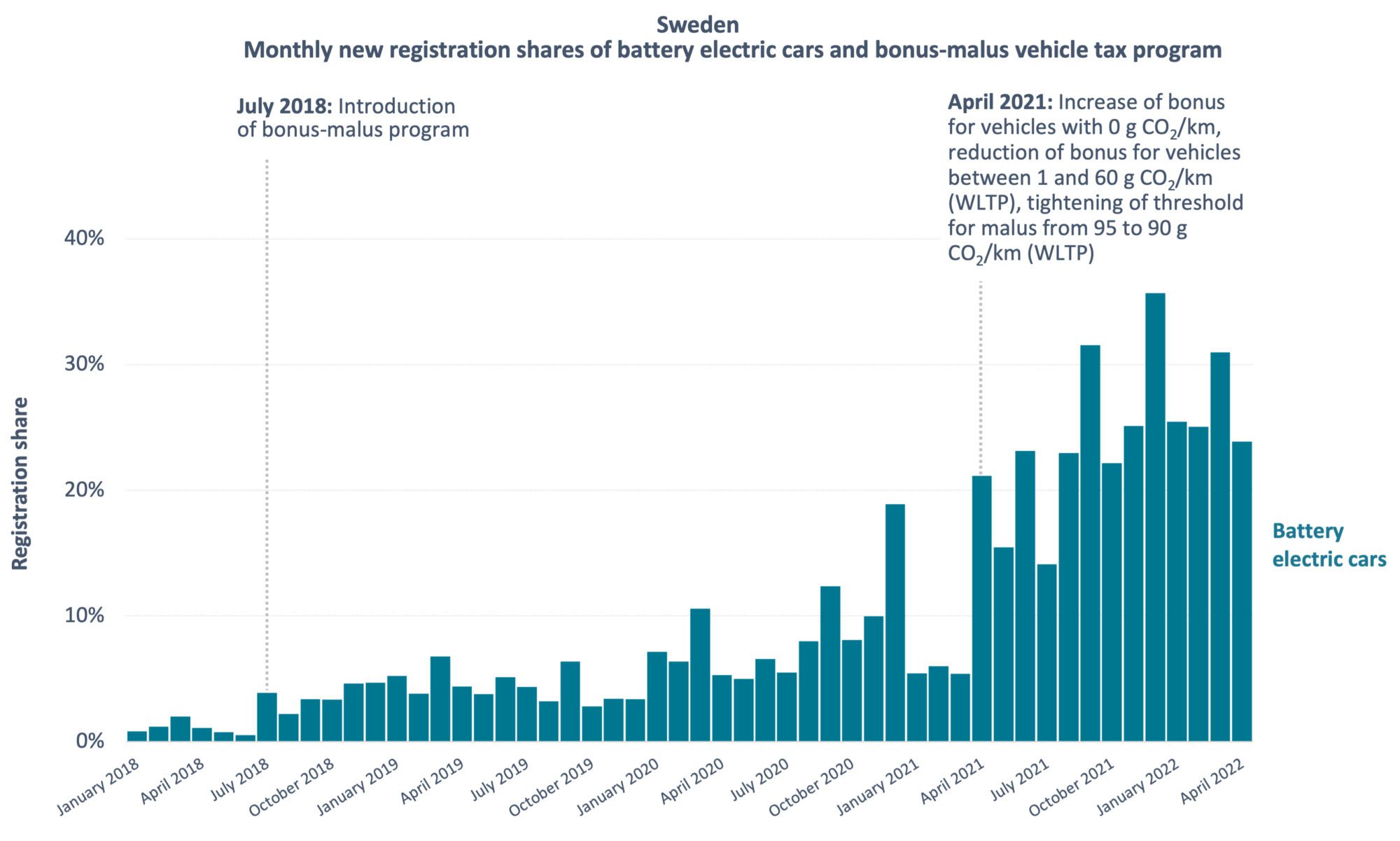

Sweden introduced a bonus-malus system in July 2018. It applies to new cars, motorhomes, light trucks, and light buses. The bonus for a vehicle emitting 0 g CO2/km is SEK 70,000 (€6,900). Bonus rates for vehicles with official emission values between 1 and 60 g CO2/km decrease linearly from SEK 44,400 (€4,400) to SEK 10,000 (€900). The malus reflects an increased vehicle ownership tax during the first three years of ownership for gasoline and diesel-powered vehicles, including hybrid electric vehicles (HEVs), with diesel vehicles paying higher rates. Malus rates for vehicles first registered from June 2022 increase linearly starting at official emission values of 76 g CO2/km.

Figure 3. Bonus-malus tax program for vehicles in Sweden; the malus entails cumulative three-year ownership taxes.

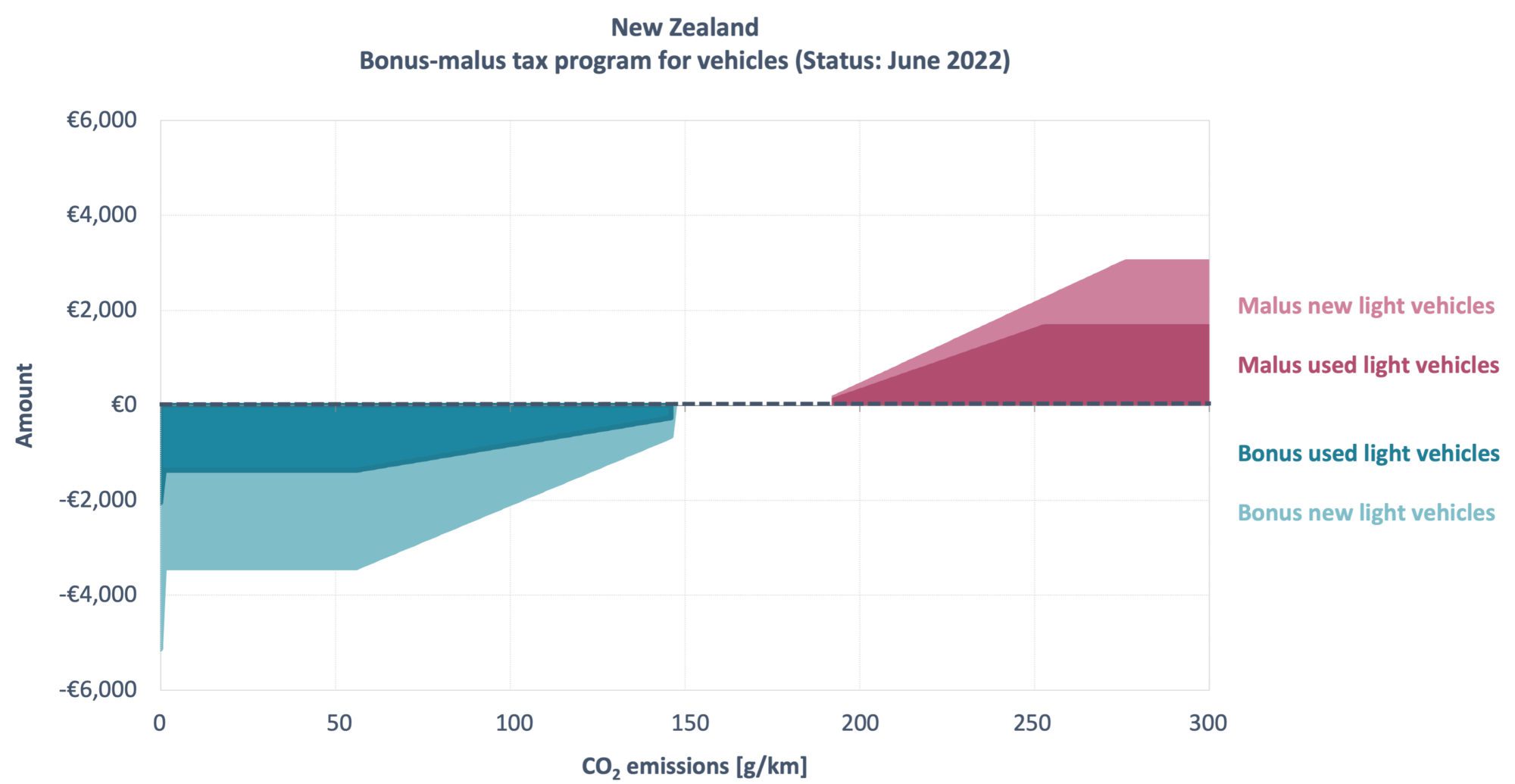

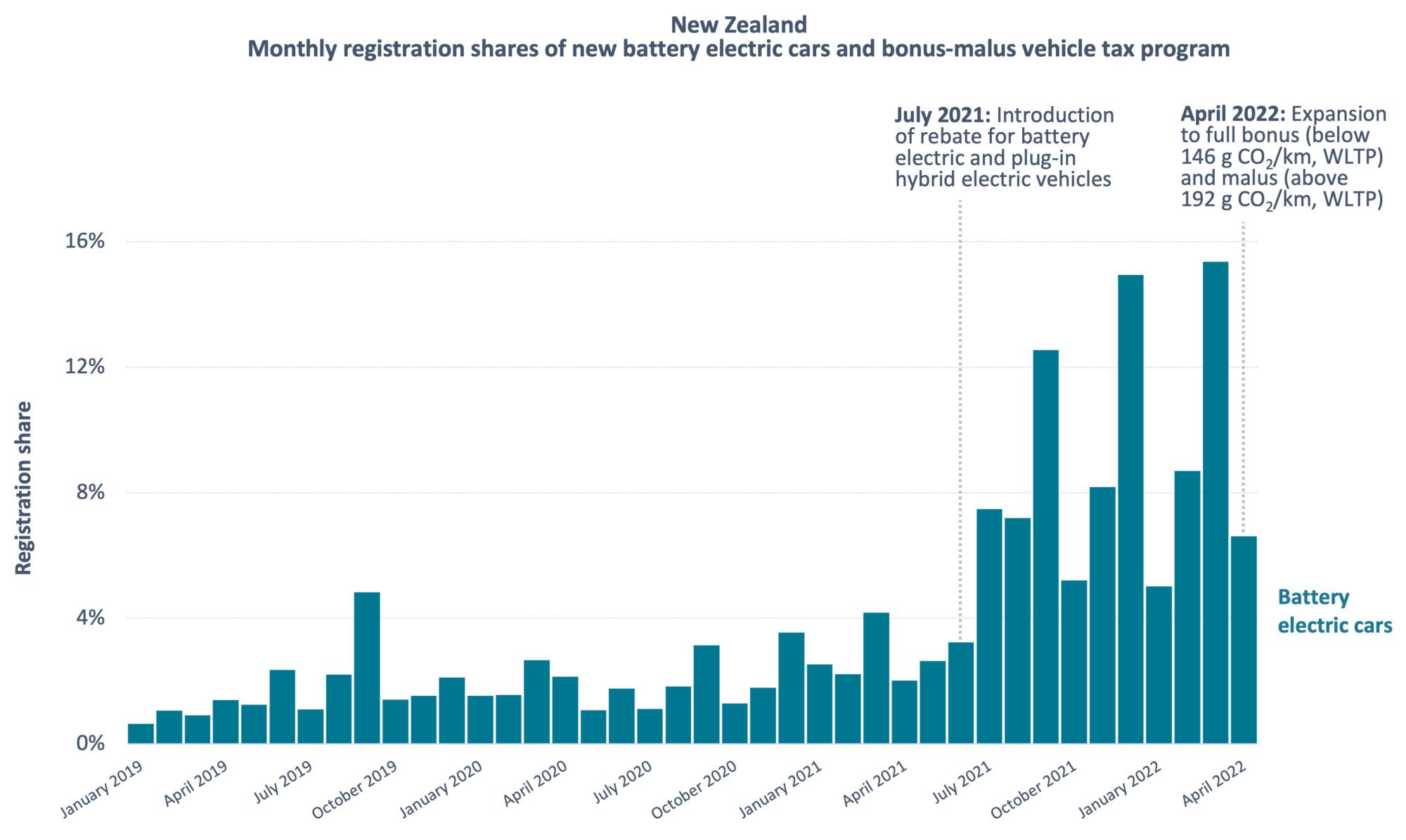

New Zealand is the latest country to establish a feebate program. The country introduced a rebate for BEVs and PHEVs in July 2021 and expanded the program to a full bonus-malus scheme in April 2022, which applies to new and used imported passenger cars and light commercial vehicles (aka light vehicles) first registered in New Zealand. For new vehicles, the maximum rebate is NZ$8,625 (€5,100) for emissions of 0 g CO2/km and NZ$3,423 (€3,400) if official CO2 emissions range between 1 and 56 g/km. For new vehicles with CO2 emissions between 56 and 146 g/km the rebate linearly decreases to NZ$654 (€260). The fee for high-emitting new vehicles starts at 192 g CO2/km at NZ$259 (€200), linearly going up to NZ$5,175 (€3,100) for cars emitting 276 g CO2/km or more. The rebates and fees for used vehicles are reduced by about half.

Figure 4. Feebate tax program for light vehicles in New Zealand.

One main argument in favor of feebates or feebate-like programs is that financial incentives coupled with disincentives can help to spur the transition to zero- and low-emission vehicles and thereby reduce CO2 emissions from transport. While it is difficult to isolate the effects of one single measure on the average national CO2 emission levels of new vehicles, there is an indication that these schemes help to stimulate purchases of zero- and low-emission vehicles. In Sweden, registrations of BEVs, which have zero tailpipe emissions, surged to historic highs following the introduction of the bonus-malus scheme, with monthly shares reaching 2%–5% in the last half of 2018, as shown in the figure below, up from an average of 1% in the preceding six months. Increased bonus rates for BEVs and decreased rates for vehicles emitting between 1 and 60 g CO2/km, which applies mostly to PHEVs, starting in April 2021 also appear to have helped to spur particularly BEV purchases. Between April 2021 and April 2022, BEV shares of new passenger car registrations ranged between 14% and 36%.

Figure 5. Monthly shares of battery electric cars in new passenger car registrations in Sweden between January 2018 and April 2022 (NEDC = New European Driving Cycle, WLTP = Worldwide Harmonized Light Vehicles Test Procedure).

New Zealand’s bonus-malus program also appears to be having a positive effect on electric vehicle registrations. By the end of April 2022, nine months after the introduction of the rebate and one month after the introduction of the fee, registration shares of new battery electric passenger cars have increased significantly, as shown below. Since July 2021, their monthly shares reached historic highs of between 5% and 15% compared to shares of 2% to 4% in the first half of 2021. In April 2022, following the introduction of the full bonus-malus scheme, new registrations of PHEVs and HEVs rose by over 9 and 21 percentage points compared to the previous month, respectively.

Figure 6. Monthly shares of battery electric cars in new passenger car registrations in New Zealand between January 2021 and April 2022 (WLTP = Worldwide Harmonized Light Vehicles Test Procedure).

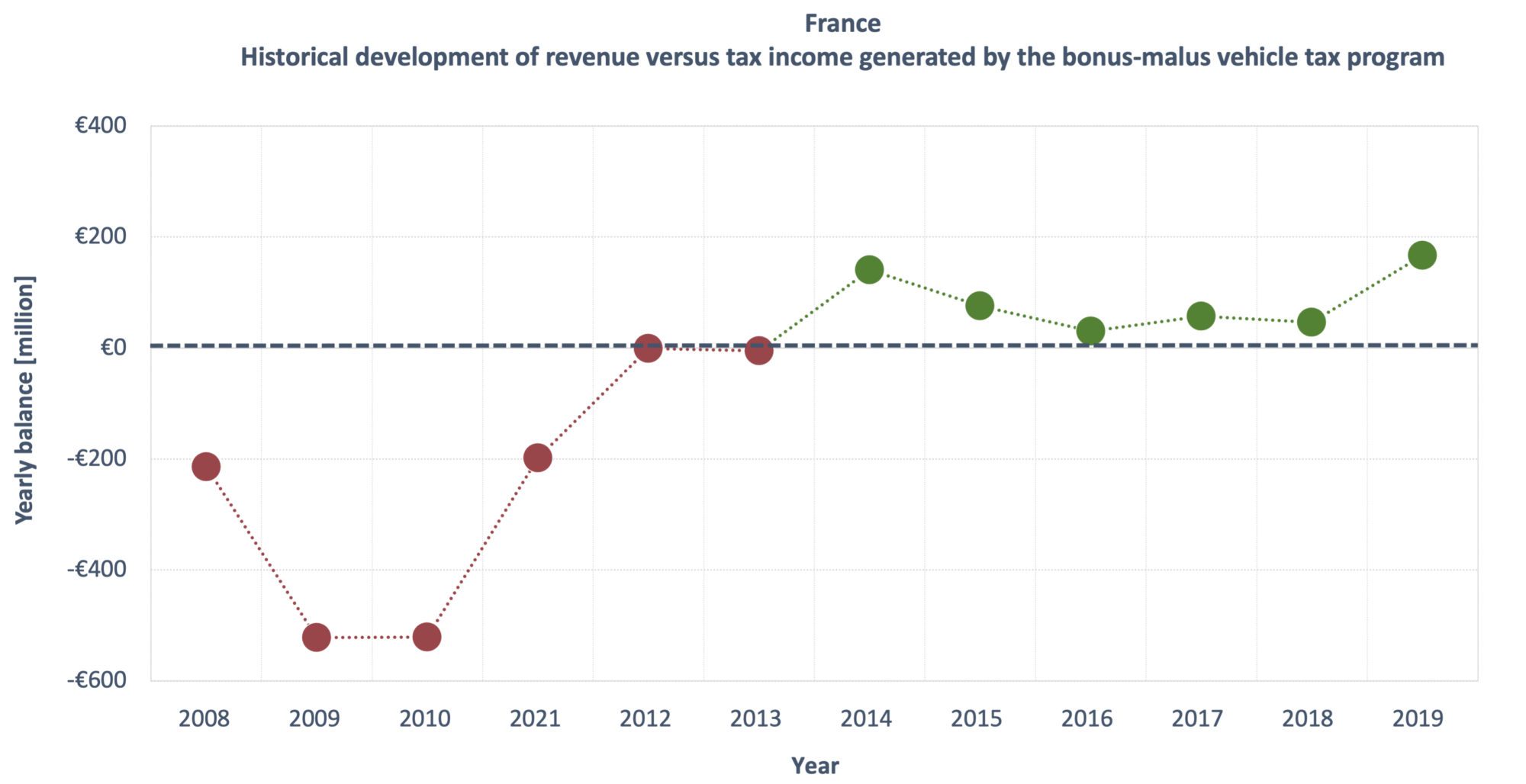

Another key argument for feebate programs is that they can be cost neutral if designed carefully. Taking France as an example, the bonus-malus program ran a deficit in the early years, peaking with at over €500 million in 2009. Since 2014, the program has achieved a constant positive balance, even when financing the bonus for scrapping an older car between 2016 and 2018. Hence, the government appears to have managed the bonus-malus without loading the public budget with expenses since 2014.

Figure 7. Balance amounts of the French bonus-malus tax.

As shown in France, if designed carefully and reviewed regularly considering market changes, bonus-malus schemes can help the transition to electric vehicles in a revenue-neutral way. The step design of the bonus-malus program in Singapore, in contrast to the progressive curve design used in France, Sweden, and New Zealand, may make it harder for the government to maintain a neutral budget. This is due to manufacturers being able to design vehicles to register type-approval CO2 emissions just below the step function cut points to qualify for large rebates. When looking at how the programs can positively effect uptake overall, the tighter thresholds affecting most vehicles in Sweden have likely contributed to higher BEV registrations. Additionally, including used vehicles in a feebate scheme as in France, Singapore, and New Zealand can be of additional benefit to reach a broader consumer group such as low-income households.

Overall, feebates can be a crucial policy measure in the transition towards zero- and low-emission vehicles. For countries where the transition to zero-emission vehicles is in full progress, as in Sweden, it is time to think about the next phase, such as how to gradually phase out rebates or bonuses and how to deal with lost fuel tax revenues. But so far, most markets still have a long way to go. Feebates or bonus-malus programs can certainly be one good option to reach this point at a faster pace while helping to spur supply and consumer demand in these markets.