Market Spotlight

European Market Monitor: Cars and vans (June 2025)

Passenger car registrations

Figure 2. Average CO2 emissions of manufacturer pools and individual manufacturers compared with estimated 2025-2027 targets, 2025 YTD

Note: Includes compliance credits. All CO2 values are estimates according to the Worldwide harmonized Light vehicles Test Procedure (WLTP). Only manufacturer pools and individual manufacturers with at least 1% market share YTD are shown. See the section on definitions, data sources, methodology, and assumptions for more.

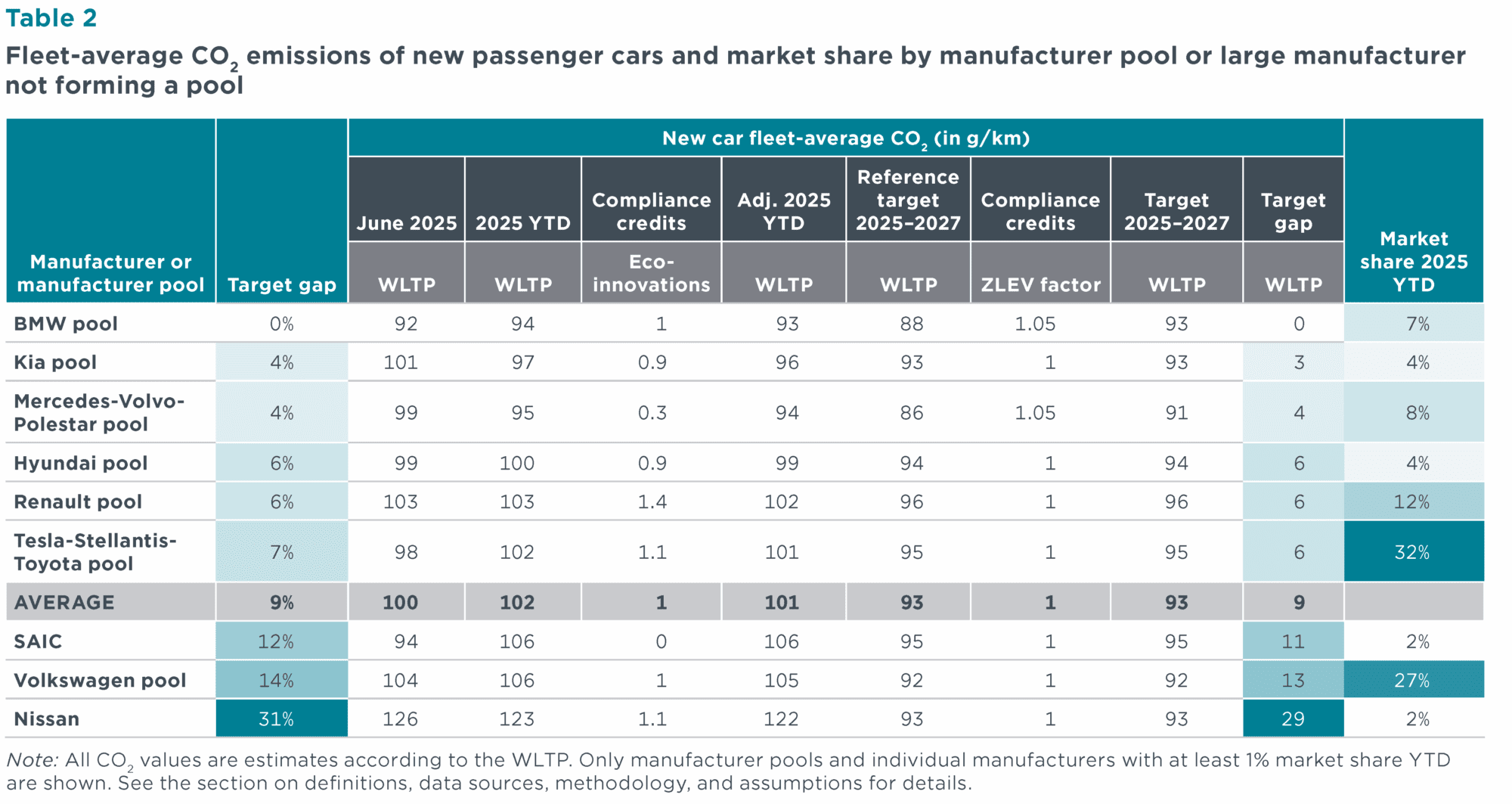

Carbon dioxide (CO2) emissions among manufacturer pools averaged 102 g CO2/km in H1 2025. Manufacturing pools thus remain 9 g CO2/km from the average target of 93 g CO2/km for the 2025–2027 period. With a market share of 32%, the Tesla-Stellantis-Toyota pool reduced its target gap by 1 g CO2/km compared with the previous month. The BMW pool is now on track to meet its 2025–2027 target, while Nissan (29 g CO2/km above) remains the farthest from reaching its target.

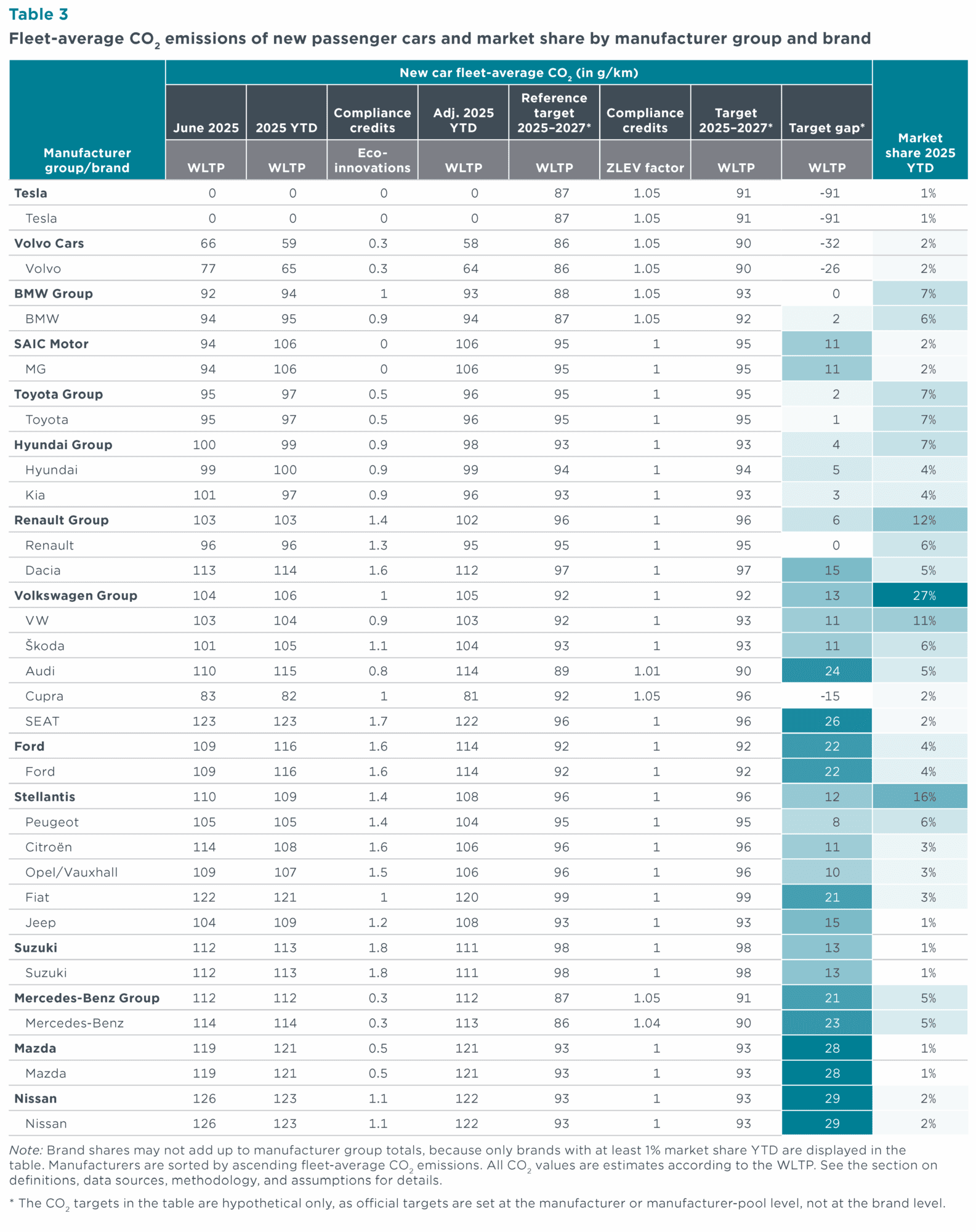

Looking at individual car brands with market shares of 1% or greater, apart from Tesla, Volvo had the greatest over-compliance at 26 g CO2/km below its projected brand-level average target for 2025–2027, and was followed by Cupra, which was 15 g CO2/km below its target. Mazda and Nissan currently have the largest target gaps at 28 and 29 CO2/km, respectively.

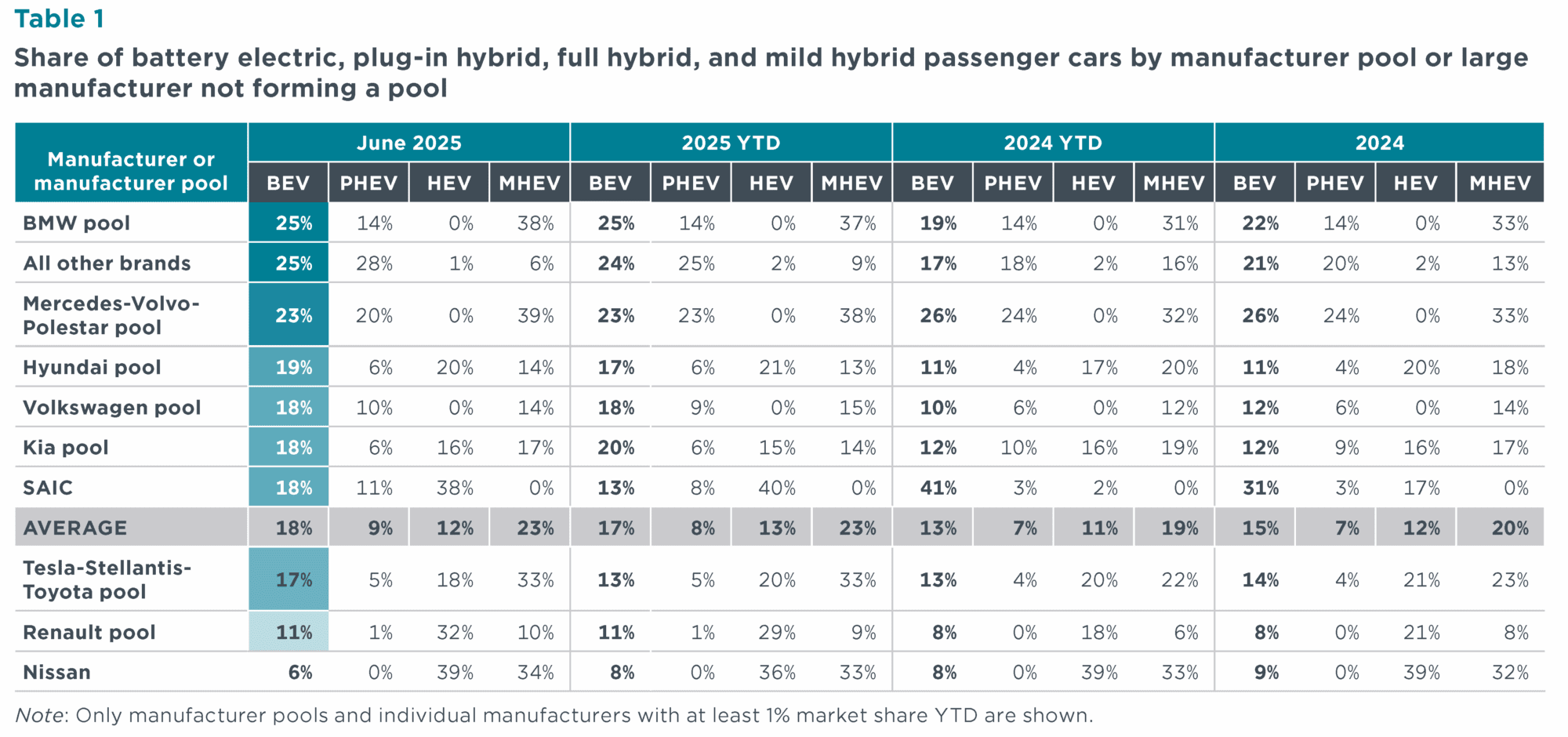

Table 1. Share of battery electric, plug-in hybrid, full hybrid, and mild hybrid passenger cars by manufacturer pool or large manufacturer not forming a pool

Table 2. Fleet-average CO2 emissions of new passenger cars and market share by manufacturer pool or large manufacturer not forming a pool

Table 3. Fleet-average CO2 emissions of new passenger cars and market share by manufacturer group and brand

Passenger car registrations by country

Figure 3. Share of plug-in hybrid and battery electric passenger cars by country, including information on market size (total new car registrations)

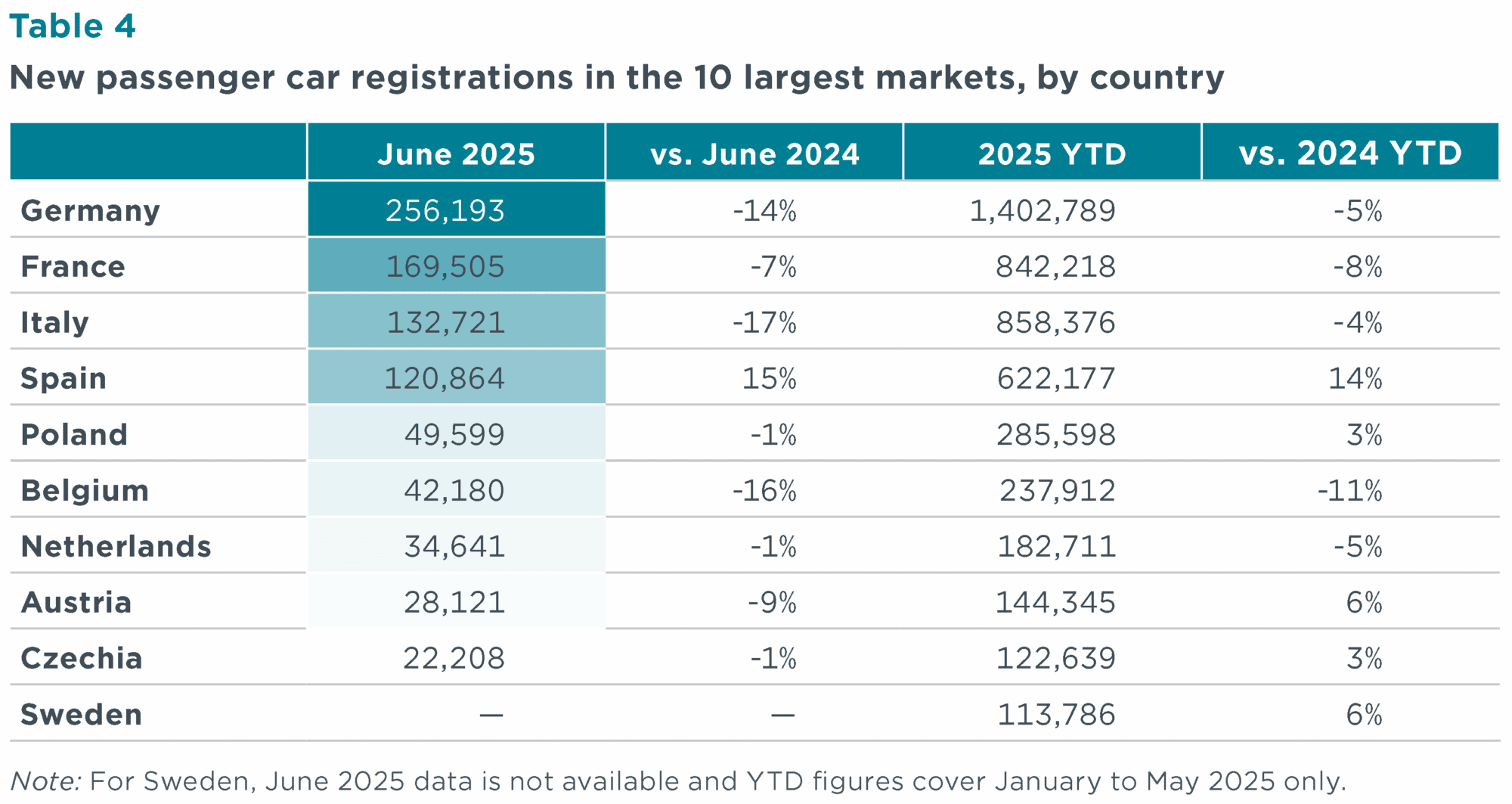

Table 4. New passenger car registrations by country

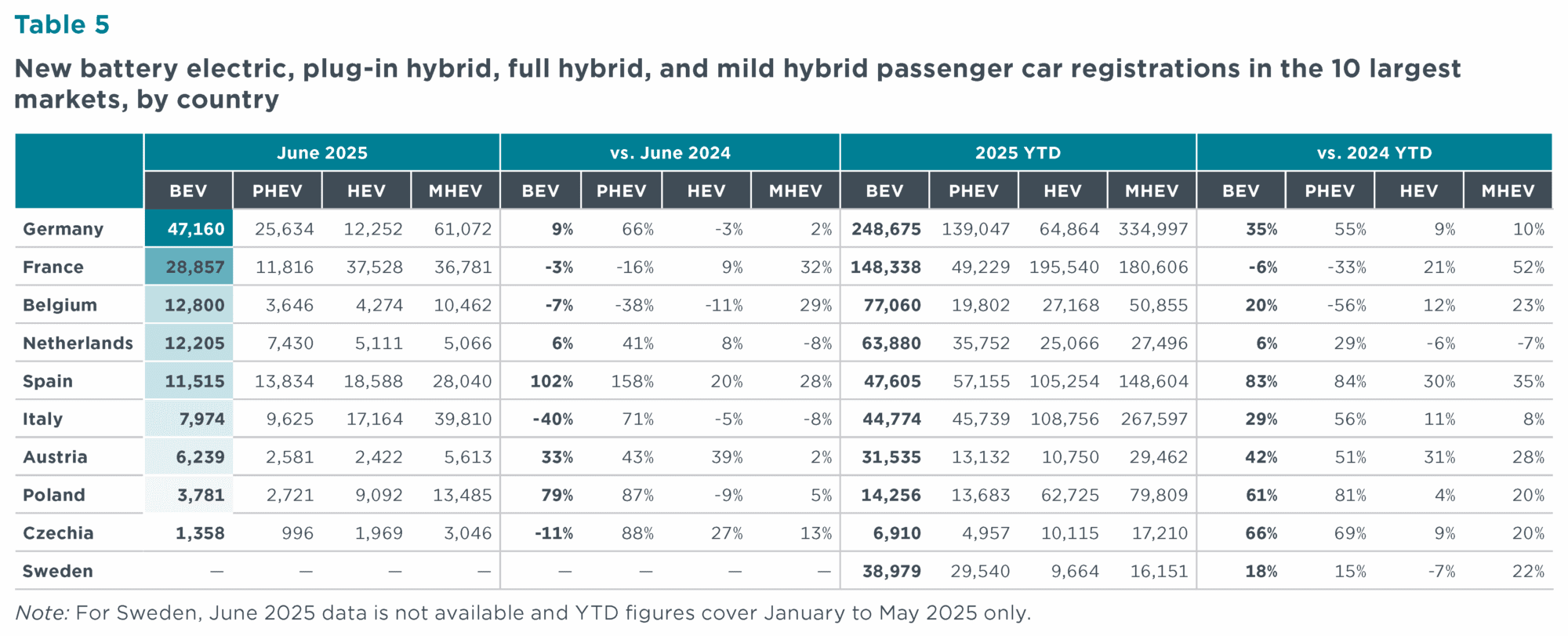

Table 5. New battery electric, plug-in hybrid, hybrid, and mild hybrid passenger car registrations by country

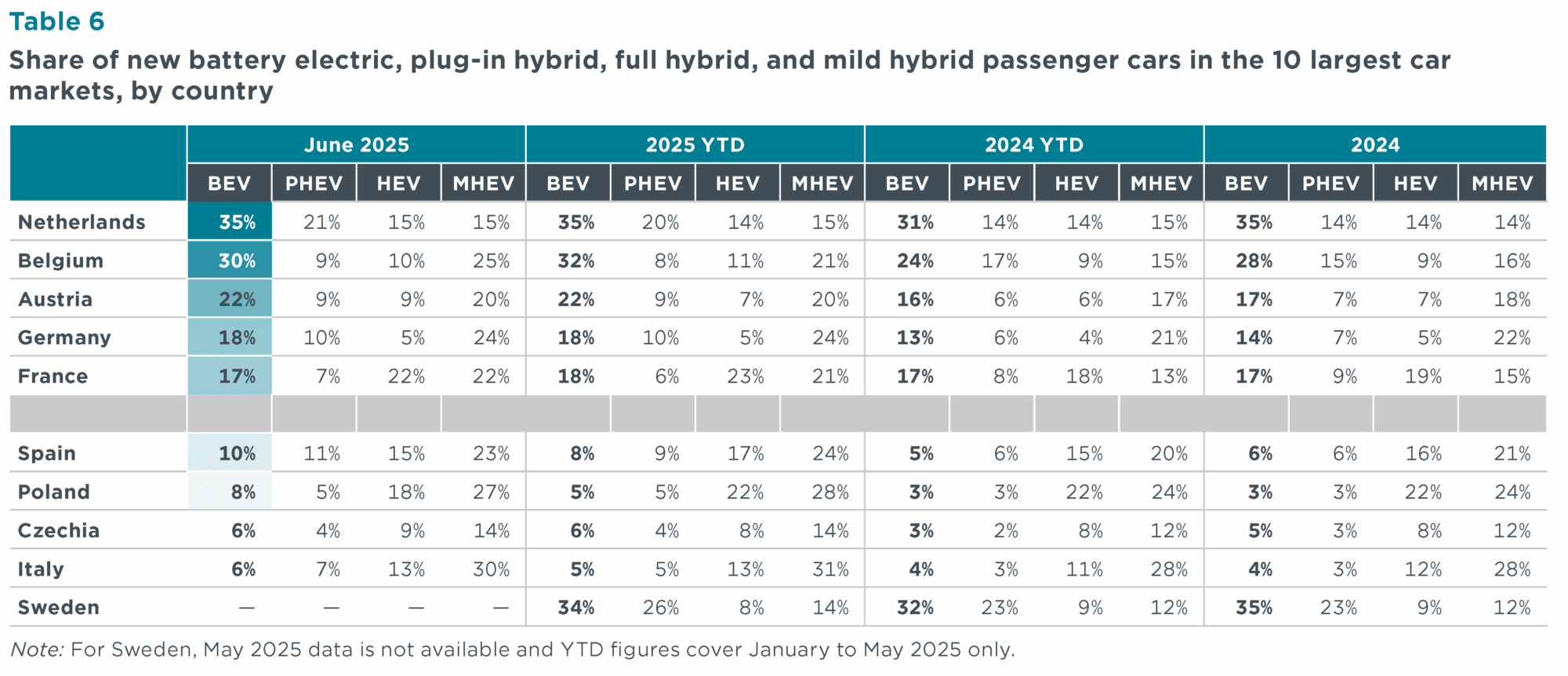

Table 6. Share of new battery electric, plug-in hybrid, full hybrid, and mild hybrid passenger cars by country

Passenger car registrations by owner

Corporate fleets, comprised of company fleets (34%), car dealers and manufacturers (15%), and short-term rentals (14%), made up 63% of the total registrations in April and May 2025, while private cars made up 37% of the market. Short-term rental registrations appear to fluctuate more than other owner types; they ranged from nearly 14% of sales in April and May 2025 to only 6% in the third quarter (Q3) 2024. In April and May 2025, the split of new registrations by owner type largely mirrored that of Q2 2024.

Figure 4. New passenger car registrations by owner for 19 select European countries

Van registrations

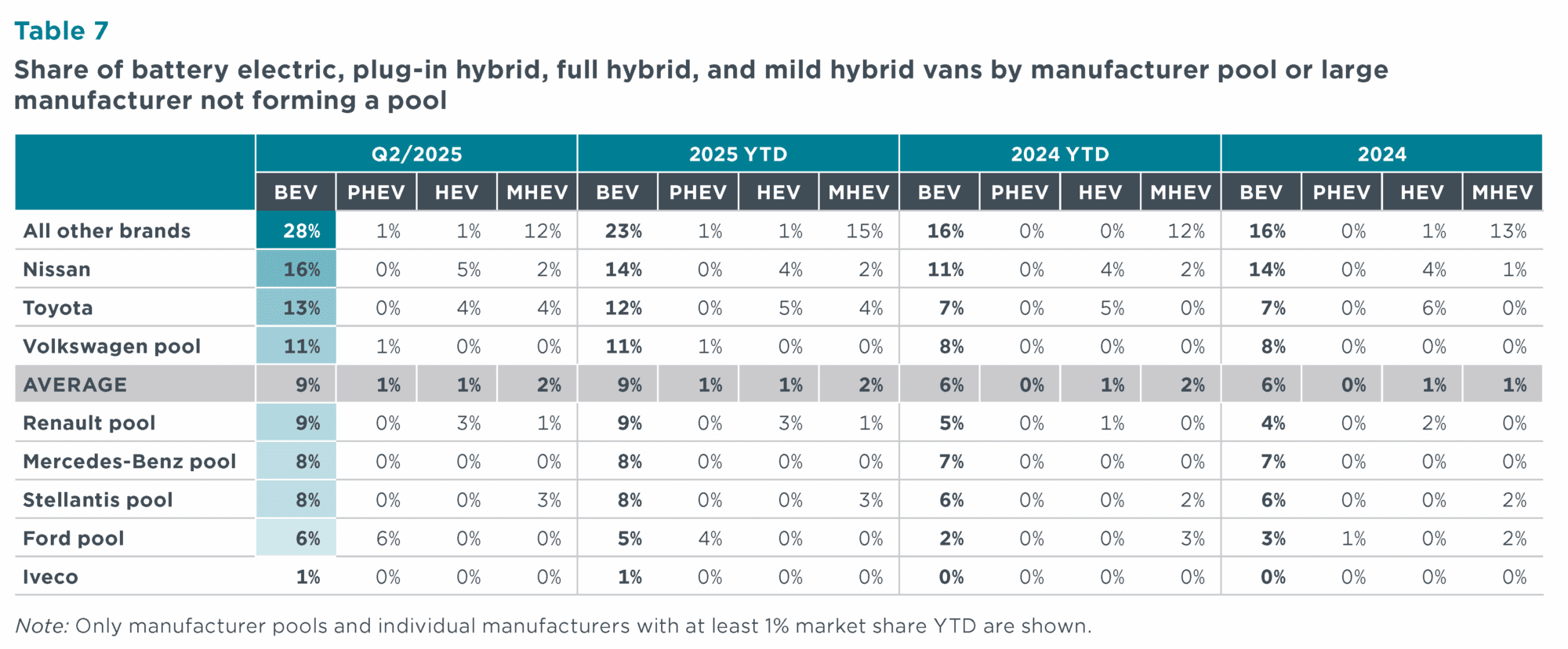

Table 7. Share of battery electric, plug-in hybrid, full hybrid, and mild hybrid vans by manufacturer pool or large manufacturer not forming a pool

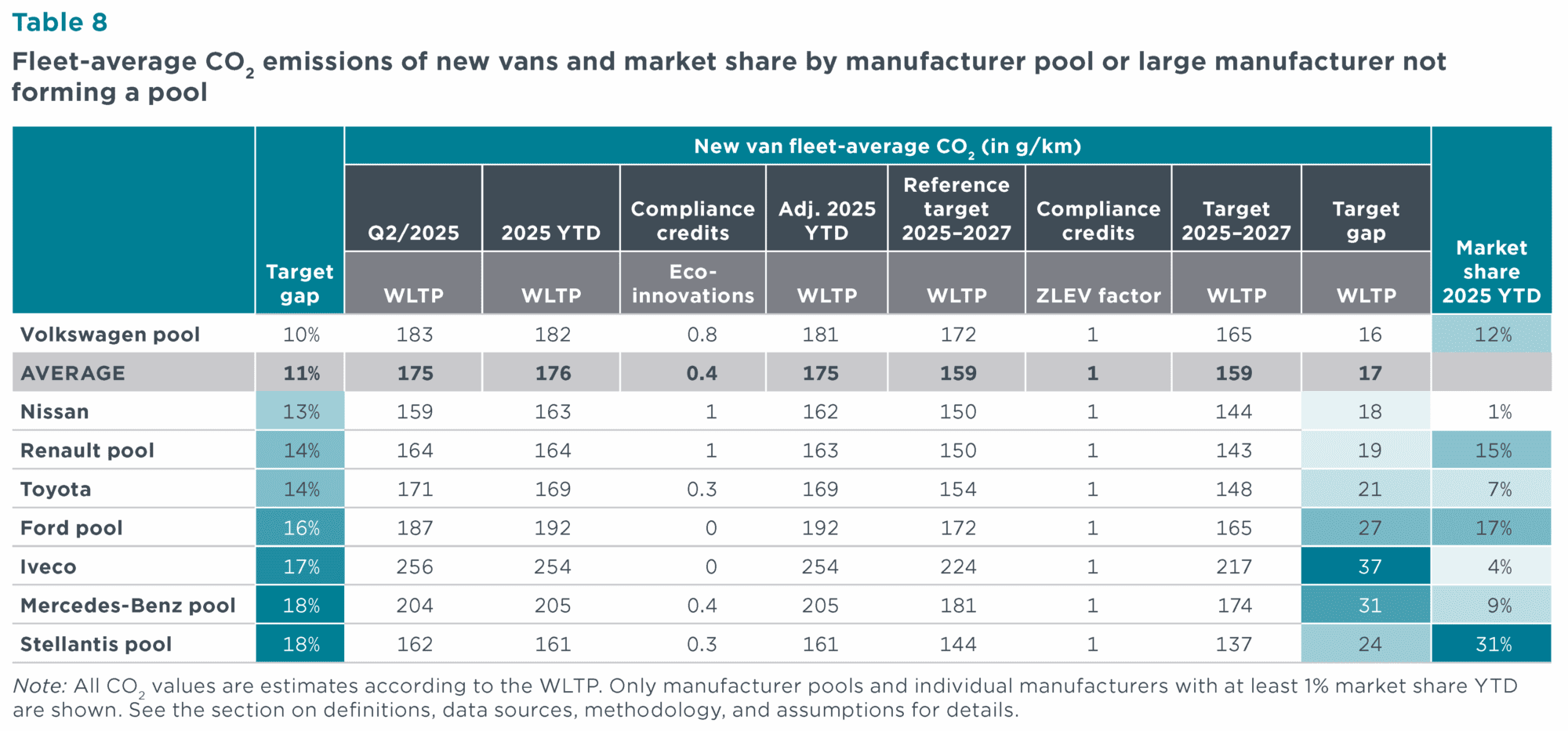

Table 8 . Fleet-average CO2 emissions of new vans and market share by manufacturer pool or large manufacturer not forming a pool

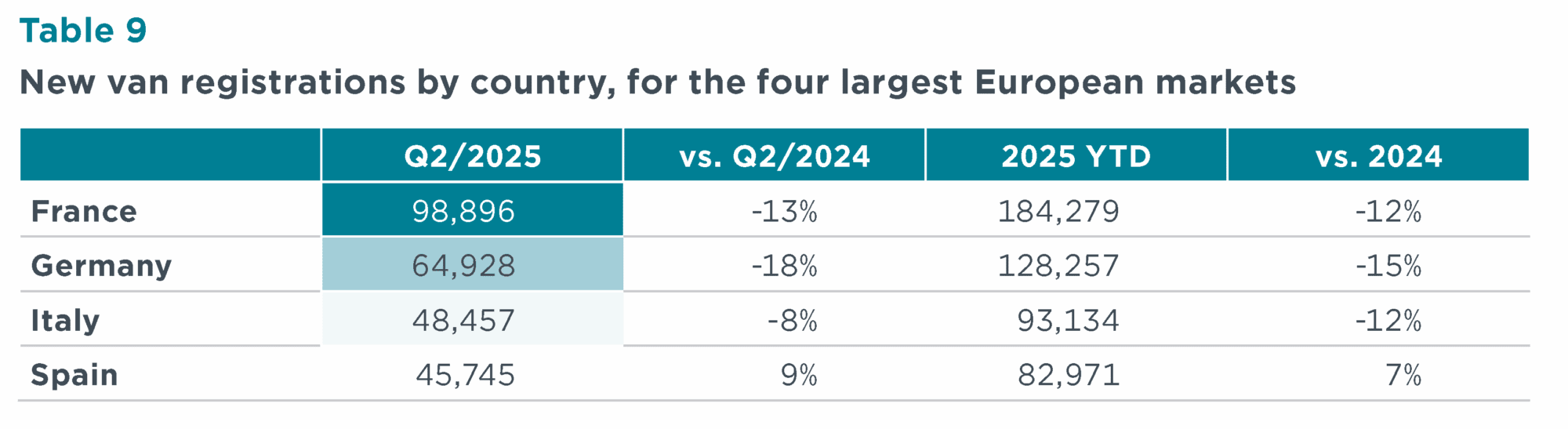

Table 9. New van registrations by country, for the four largest European markets

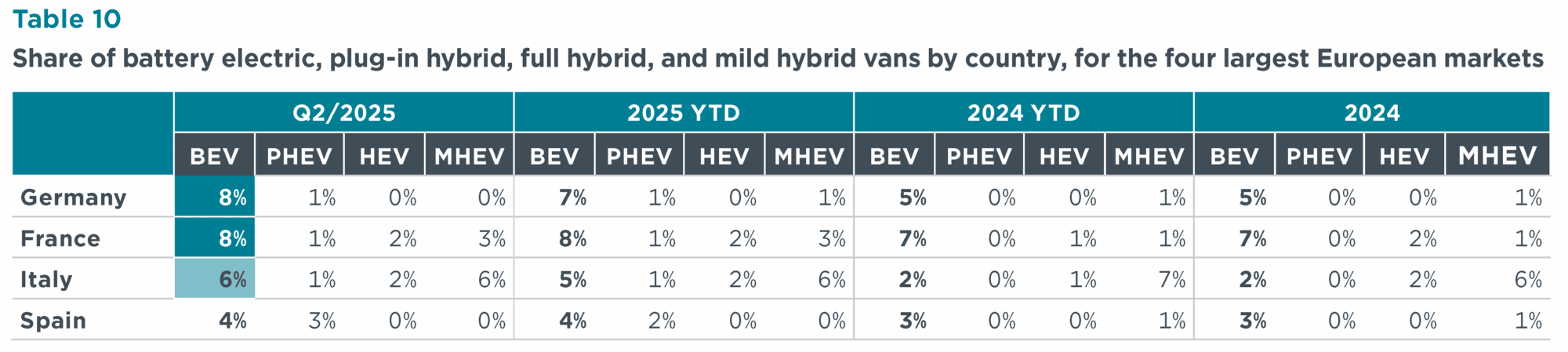

Table 10. Share of battery electric, plug-in hybrid, full hybrid, and mild hybrid vans by country, for the four largest European markets

Spotlight: Charging infrastructure development

Figure 5. 22 kW-equivalent publicly accessible charging points installed per thousand passenger cars and vans, by type of power output and country by the end of June 2025

This publication is a collaboration between the ICCT, IMT-IDDRI, and ECCO think tank.