Electric vehicle capitals: Showing the path to a mainstream market

Briefing

Update on the global transition to electric vehicles through 2019

By the end of 2019, electric vehicles have been deployed in over 100 countries. With dramatic growth through 2019, passenger electric vehicle sales surpassed 7 million roughly twice as fast as it took conventional hybrids to do so, despite having greater cost and infrastructure barriers to overcome. China’s cumulative passenger electric vehicle sales through 2019 reached 3.66 million, accounting for 48% of the global stock. Other top ten markets in terms of cumulative sales of passenger electric vehicles include the United States, Germany, Norway, the United Kingdom, the Netherlands, France, Canada, Japan, and Sweden. All of these markets have regulations, incentives, charging infrastructure deployment, and consumer promotion actions to spur electric vehicle uptake. There have been approximately 18,000 cumulative hydrogen fuel cell vehicle sales globally from 2013 through 2019, with most of these sales in the United States (44%), South Korea (28%), and Japan (20%). Cumulative sales of heavy-duty electric vehicles were less than 1 million through 2019, with over 98% of which occurred in China.

Electric vehicle shares of new passenger vehicle sales are increasing, reaching a record-high of nearly 3% globally in 2019. Norway achieved an electric vehicle share of 58% in 2019, ranking first globally. This is the first time ever that electric vehicle share of a national-level market exceeded 50%. Nine metropolitan areas have deployed more than 100,000 passenger electric vehicles through 2019. The top two cities, Shanghai and Beijing, both had more than 300,000 passenger electric vehicles. China accounted for six of the top ten local-markets for passenger electric sales in the world.

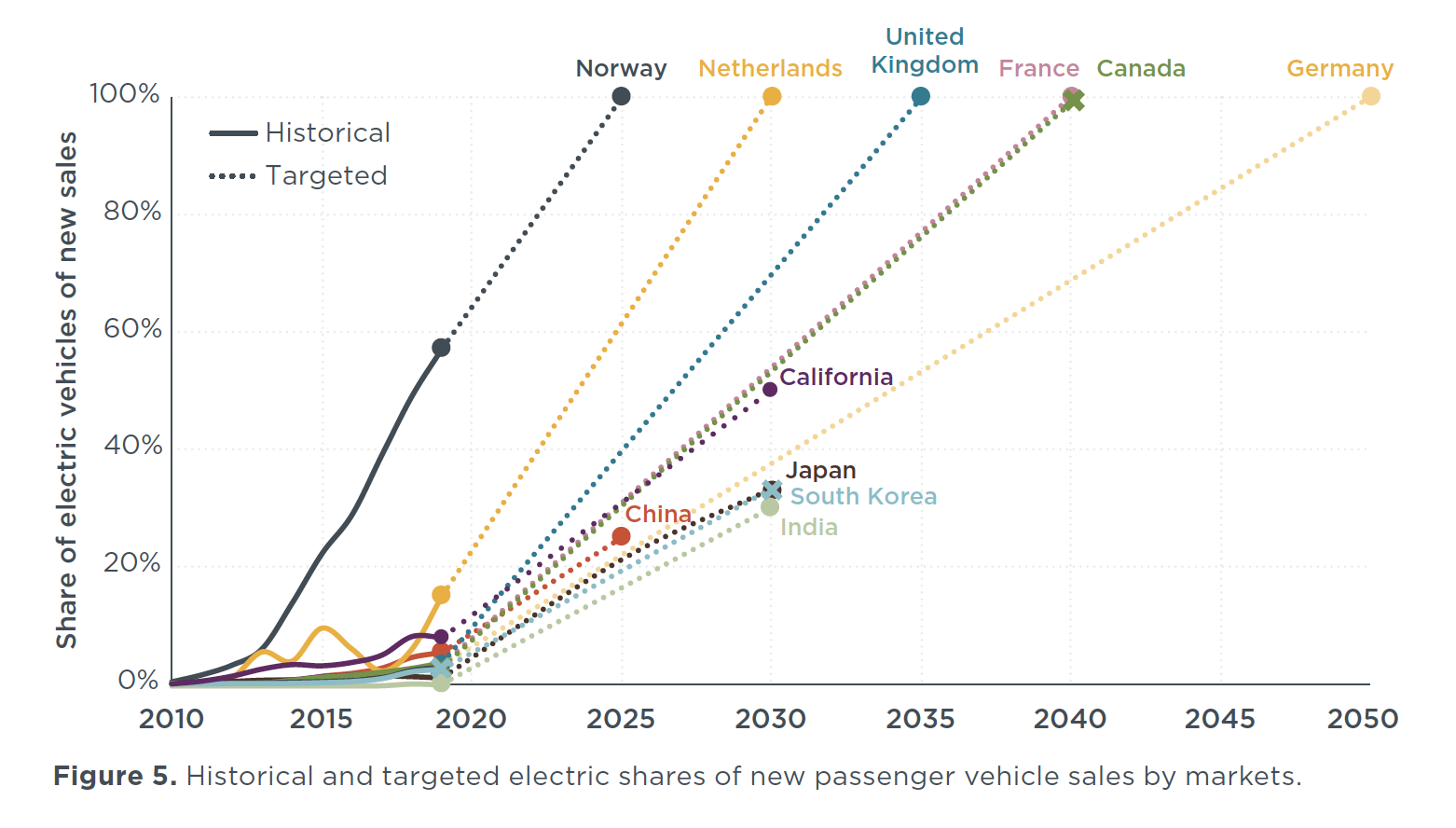

More than a dozen countries have proposed timelines to transition to all zero-emission vehicles within the next three decades. In addition, many states and provinces have set more aggressive goals than their national governments, and cities, in particular, have been targeting a much faster transition.

Governments at all levels have leveraged a variety of policy tools to overcome EV barriers and stimulate the market. The policy measures include regulations to ensure high EV model availability, financial incentives to make EVs cost competitive, charging infrastructure to ensure EVs are convenient, and campaigns to increase consumer awareness. The highest EV-uptake markets have all such actions in place, and they also tend to learn from international cooperation platforms to accelerate their transition to electric vehicles. Although regulation at the EU-level has been implemented through 2030, European governments have by and large not converted their 100% zero-emission goals to enforceable laws. The other top markets of China and the United States have several pioneering local markets, but otherwise are due for updated policies to ensure they are on paths toward a full transition to zero-emissions.

Although progress has been made through 2019, the global transition to electric vehicles is still at an early stage. Norway is the only country that appears to be truly on track to meet its electric vehicle goal. If Norway continues to grow at its current rate, it could achieve its 100% electric vehicle share goal in 2025. The other jurisdictions with vehicle electrification ambition will need to make significant progress to meet their targets. Continued policy support, as well as innovations in vehicle technology and progress in infrastructure build-out, will be needed to accelerate growth rates and ensure that the goals for full vehicle electrification are achieved.