Blog

The next generation of electric vehicles is on the way

Anyone in the market for a new electric vehicle may feel overwhelmed by the multitude of recent automaker announcements unveiling new consumer options. Proponents of electric vehicles are bound to consider this a good thing; there’s a statistical link between the range of models available and EV sales.

The Paris Motor Show last month provided a platform for several flashy electric vehicle introductions. Volkswagen unveiled the “ID” concept model, which is expected in 2020 with a 400 km laboratory test (perhaps approaching 200 mile real world) range and a price around 30,000 euros. Renault revealed the soon-to-be-available 2017 Zoe, which has a 186-mile real-world range and will be priced at approximately 23,600 euros. Smart promoted the coming release of the first electric convertible.

Volkswagen’s concept car, the ID.

Numerous announcements predating the Paris Motor Show add to the parade of new models. The 238-mile Chevrolet Bolt is priced at $37,495 and will be available late 2016. The 215+ mile Tesla Model 3 is expected to cost $35,000 and become available in late 2017. The 200+ mile Nissan Leaf is expected sometime in 2018. Other manufacturers, like Mercedes-Benz and BMW, have announced plans to offer electric versions of their high-volume model series, while Volkswagen plans to develop 30 electric models by 2025. These are a few of many exciting announcements and new model “sneak peeks” happening worldwide. We can infer that automakers (even Toyota, who has been relatively late to the game) increasingly view electric vehicles as an important part of their future revenue streams.

Renault’s longer-range version of its Zoe ZE40.

These splashy introductions go hand in hand with companies’ recent announcements of higher electric vehicle sales targets. Daimler, for example, hopes to reach 100,000 annual sales by 2020. Audi, Mitsubishi, Renault-Nissan, and Volvo have announced electric vehicle sales targets of 10%–20% of sales by 2020, or 25% by 2025. Tesla and BYD have announced plans to increase annual electric-vehicle production volume up to 500,000 units in 2018 and 2020, respectively. Volkswagen has a target of 2–3 million electric vehicles (approximately 20%–25% of sales) per year by 2025.

Opel CEO, Karl-Thomas Neumann, seen with the Ampera-e, the European cousin of the Chevrolet Bolt.

In view of these announcements of electric vehicle model offerings with longer range and increasing affordability, we wanted to know exactly how quickly costs are actually coming down. Will cost reductions enable competitive pricing for high-volume mainstream markets?

The short answer is yes.

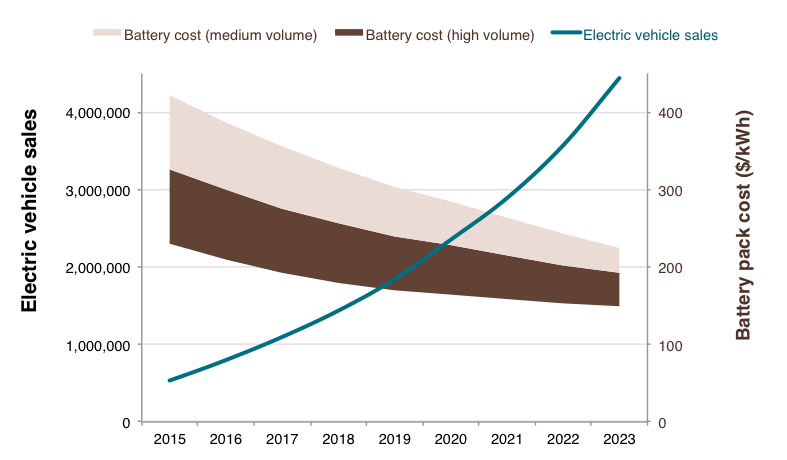

We’re finding that advancements in lithium-ion chemistries combined with greater production volumes are expected to significantly decrease battery pack costs. The figure below shows the estimated decline in battery pack costs (brown, right axis) and the associated increasing sales of electric vehicles (blue, left axis). As shown, global sales were approximately 500,000 in 2015, while industry-average battery pack costs were around $400 per kilowatt-hour. Also shown is the projected cost reduction, down to around $150–$175 per kilowatt-hour in 2020–2023 for high-volume manufacturers. Our analysis is based on the best available bottom-up engineering analyses (see here, here, here, here, and here). Others, like Bloomberg New Energy Finance, suggest that even more dramatic cost reductions are possible.

Figure ES-1. Scenario for estimated electric vehicle sales and battery pack cost

Enabled by falling battery pack costs, automakers are considering different ways to balance price reductions and range increases on their future model offerings. To provide an oversimplified example, battery pack cost reductions from $400 per kilowatt-hour to $150 per kilowatt-hour would translate to a per-vehicle cost reduction of over $8,000 for a 120-mile range vehicle. Alternatively, the same per battery pack cost reductions could allow for vehicle range improvements to 200+ miles while still seeing an overall cost reduction of around $5,000. This example demonstrates manufacturers’ dilemma when considering how to address consumer cost and range barriers.

Electric vehicle metrics like range and cost are expected to continue to dramatically improve over the next few years as the next-generation technology emerges. In fact these developments are happening about five years faster than previous projections, such as those by the National Research Council, suggested. Why? Largely because of recent breakthroughs in lithium-ion chemistries, a better understanding of the linkage between battery pack costs and production volume, and the trend towards much greater manufacturing plant production scale.

Automaker announcements and technology trends indicate an expanding electric vehicle market that continues to address key range and cost consumer barriers. We are starting to grapple with exactly what all these trends might mean for policy. For example, how do these trends affect the need to continue consumer electric vehicle incentives and long-term vehicle efficiency standards in the years ahead? These have been key questions of the ZEV Alliance members and many other governments (e.g., China). We’ll be reporting on these questions later in the year.