Power play: Unlocking the potential for U.S. automotive trade with electric vehicles

Blog

Money makes the world go electric: Why the U.S. government should invest in the electric vehicle industry

In contrast to sluggish sales overall in the automotive industry since the pandemic, sales of EVs continue to increase at a “pedal to the metal” pace. Since our first U.S. Power Play publication in 2021, which summarized automakers’ commitment to electric vehicles (EVs), more automakers have jumped on the EV bandwagon. As part of a new $3.7 billion investment, Ford aims to increase production of its F150 Lightning truck at its Dearborn plant and plans introduce a new electric commercial vehicle. Meanwhile, General Motors will inject $7 billion into its plants in Michigan to boost production of its full-size electric pickups as rivals to Ford’s.

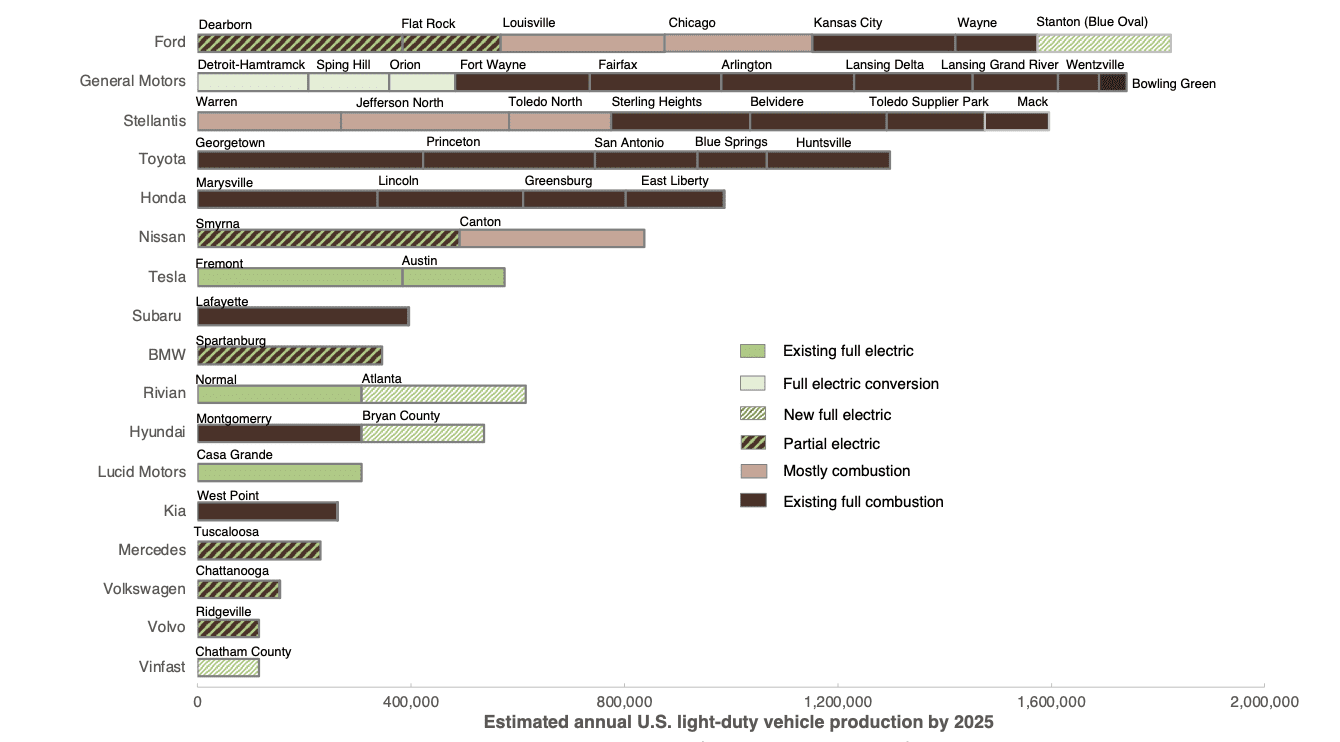

A new tally of electric versus combustion production at U.S. assembly plants is shown in Figure 1, which includes four new full electric plants from Vinfast (a rising Vietnamese all-electric automaker), Ford, Hyundai, and Rivian. Of the 49 passenger vehicle assembly plants shown in the figure, 11 will produce only electric vehicles by 2025. This includes four existing full electric plants (dark green bar), three that are under conversion to full electric (light green bar), and four full electric plants that are under construction (green and white hatch). The rest of the plants, in different shades of brown, are partial electric (approximately one-third of 2025 production will be EVs), mostly combustion (approximately 3% of 2025 production will be EVs), existing full combustion, and new combustion.

Figure 1. Estimated annual U.S. light- duty vehicle production by 2025 (updated June 2022)

Many automakers have agreed that they can no longer step on the gas in building internal combustion engine (ICE) vehicles. For example, GM, Ford, and Stellantis have urged the federal government to lift the cap in the federal tax credit for EVs, which would help lower EV prices and benefit manufacturers and consumers alike. Several tax credit design changes can “enhance the effectiveness of the federal dollars” to advance automaker interests in producing more electric vehicles and ensure that the EV market for the average buyer can grow in tandem.

How does the federal government ensure that it is supporting automakers and U.S. consumers in the transition? It has deployed several policies to encourage automaker investments, including the federal tax credit and the Advanced Technology Manufacturing Loan. To date, the latter program has loaned $8 billion (out of $17.7 billion of total funding) to support the production of more than 4 million advanced technology vehicles, including battery electric vehicles from Tesla and Nissan. In addition, the U.S. Department of Energy (DOE) launched several initiatives to support and advance the domestic battery industry in 2021, including a National Blueprint for Lithium Batteries 2021-2030, and the creation of two consortiums, Li-bridge and the Federal Consortium for Advanced Batteries.

Despite the recent positive EV market developments, the United States still has miles to go in the EV transition. Our recent research has demonstrated that the U.S. light-duty and EV markets are behind those of China and Europe. The United States was the biggest net vehicle importer in 2019 among all the major markets, which means it imported more vehicles than it exported. In 2021, the U.S. Transportation Equipment sector (including motor vehicles and motor vehicle parts) posted a trade deficit (the difference between exports and imports) of $141 billion. Meanwhile, China and Europe developed several policies and incentives to support the growth of their EV markets, including tightened CO2 standards, additional EV incentives amid the 2020 COVID-19 economic downturn, and strong support for the domestic battery manufacturing industry. The United States risks conceding global EV market share to other countries if it falls behind them in EV industry investment.

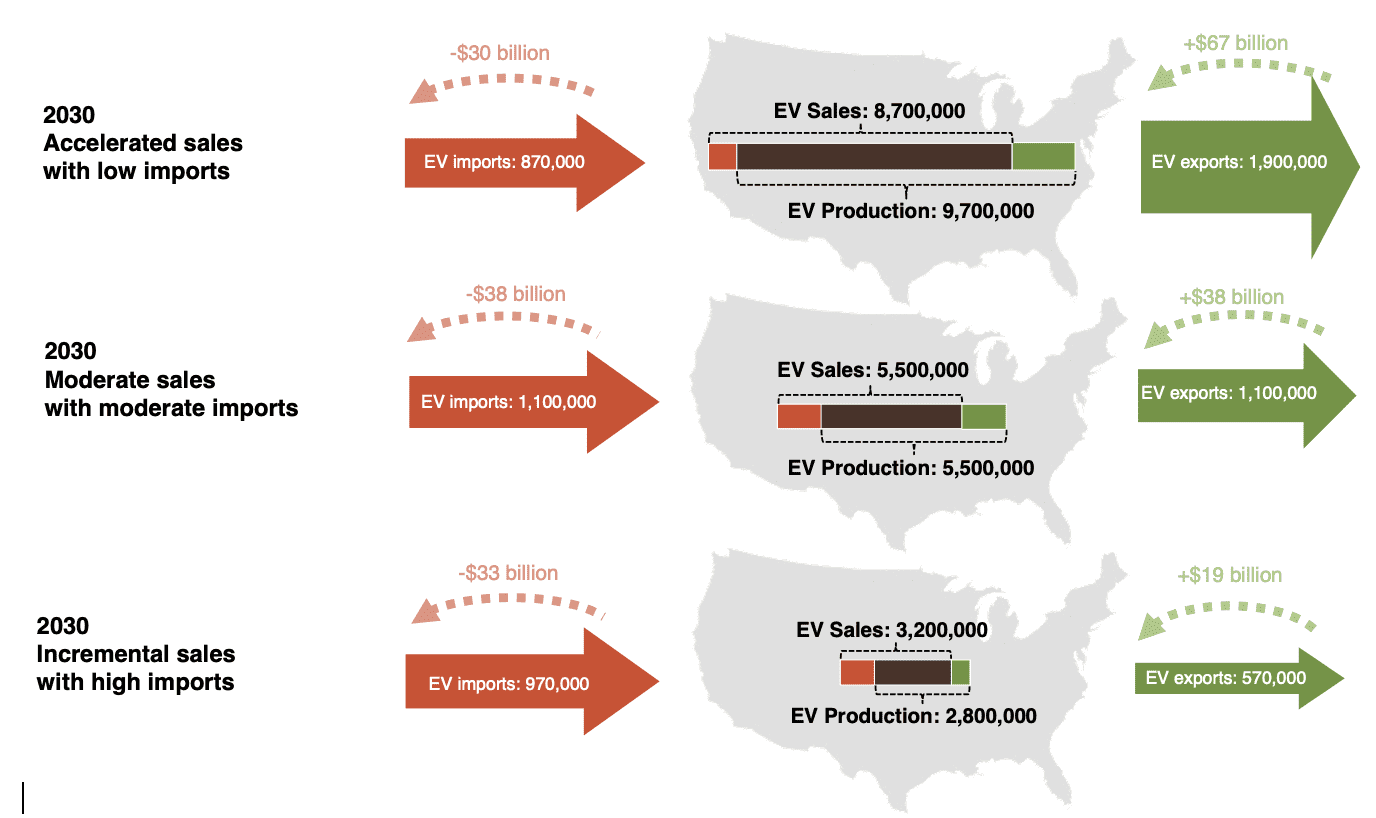

The new study also analyzed the opportunity for the U.S. automotive industry to flip the country’s passenger vehicle trade balance by capitalizing on the EV momentum. Based on the global light-duty vehicle manufacturing competition and trade dynamics, we developed nine market growth scenarios, across which the United States wholesale EV production, sales, exports, and imports were compared. In our best-case scenario, in which almost all U.S. assembly plants are converted to EV production, the United States reaches 50% EV sales in 2030, importing just 10% of electric vehicles, and the U.S. trade surplus for EVs totals $188 billion cumulatively from 2021 to 2030. The surplus in 2030 alone is roughly $37 billion in this best-case scenario, as revenue from EV exports ($67 billion) vastly exceeds the cost of imports ($30 billion), shown in the first scenario in Figure 2, “Accelerated sales with low imports.” In our “Moderate sales with moderate imports” scenario, in which the United States reaches 30% EV sales and imports 20% of that in 2030, the U.S. trade balance zeros out. The last scenario shown in the figure, “Incremental sales with high imports,” demonstrates 10% EV sales and 30% imports, resulting in a deficit of $14 billion in 2030. In all nine scenarios, we assume that U.S. EV export volume falls from close to 50% of EV production in 2020 to approximately 20% of that by 2030 . To put the trade balance figures into perspective, note that the U.S. trade balance in Agricultural products in 2021 was roughly +$42 billion, and in Minerals & Ores was +$14 billion.

Figure 2. U.S. electric vehicle market metric volumes and trade revenue in three 2030 scenarios

The federal government’s continuing investment in key EV industries also has the potential to create more jobs upstream and downstream in the supply chain. It is estimated that by 2025, close to 60,000 employees will be working on EVs. At the same time, an Economic Policy Institute (EPI) study found potential job losses associated with transitioning vehicle assembly and production from ICEVs to BEVs because BEVs require fewer parts, and thus require less time to assemble than ICEVs. To mitigate this job loss, the study suggests an increase in domestic battery and vehicle manufacturing and a decrease in reliance on imports. The study shows that close to 150,000 jobs could be created by 2030 if battery electric vehicles make up 50% of light-duty vehicles, the United States assembles 60% of its light-duty vehicles sold, and domestic EV powertrain production reaches 75% of EV powertrain used in U.S. EV manufacturing. These conditions are somewhat aligned with those assumed in our best-case scenario, in which EVs (including battery and plug-in electric vehicles) make up 50% of light-duty vehicle sales, with 73% assembled domestically (updated from the June briefing to reflect the new plant tally in Figure 1). This means that jobs created under our scenario with additional similar investment in domestic EV powertrains could be on par with the 150,000 estimates in the EPI study.

The United States is at a crossroads. It can either let the world pass it in EV manufacturing and rely on imports indefinitely, or leverage the disruption that comes with electrification to reposition the U.S. as a global leader in EV manufacturing, bringing economic benefits and jobs to U.S. shores. Strong federal regulations, support policies, and consumer incentives are critical for influencing automakers’ investment decisions. Direct financial investment, such as grants, loan guarantees, or subsidies reserved for domestic EV manufacturing would help drive more assembly plant conversions, new plant construction, and domestic battery manufacturing. To paraphrase longstanding wisdom, money makes the world go electric.