Is the Renewable Fuel Standard inadvertently driving up U.S. palm oil imports?

Blog

Is the EPA setting biodiesel mandates too high?

Regulators’ recent proposal for 2017-18 Renewable Fuel Standard (RFS2) mandates continue the EPA’s trend of requiring increased blending of biomass-based diesel (BBD, a category that includes biodiesel and renewable diesel). Under the Energy Policy Act of 2005, which introduced the RFS2 program, the federal government requires transportation fuels to contain minimum volumes of renewable fuel in four nested categories: renewable fuel (20% greenhouse gas (GHG) reduction required), advanced biofuel (50% GHG reduction, a subset of renewable fuel), BBD (50% GHG reduction, a subset of advanced biofuel), and cellulosic biofuel (60% GHG reduction, a subset of advanced biofuel).

For 2018, the agency plans to require an increase of 100 million gallons of BBD over 2017, for a total of 2,100 million gallons. An even greater increase will most likely be required depending on how the renewable and advanced biofuel mandates are set. The renewable and advanced biofuel volumes are typically met mostly by ethanol, but in recent years pressure from the blend wall has limited use of ethanol in gasoline. Setting volumes for these categories higher than what can easily be consumed under the blend wall will thus incentivize use of BBD, which is blended in diesel rather than gasoline and is not currently approaching the biodiesel blendwall on a national average.

Increased BBD mandates may seem like a good thing, based on the original legislation’s goal of reducing reliance on imported fossil fuels. But a closer look at how the mandate will have to be met suggests otherwise. The BBD mandate may actually be harmful for two reasons:

- The inelastic demand for biodiesel feedstocks caused by a mandate can cause significant price and supply shocks to agricultural commodities.

- A mandate that is too high could result in increased imports of feedstock and fuel to meet the volume requirements.

Previous ICCT research has shown that increases in soy oil prices are associated with a rise in palm oil imports – and expansion of palm oil production in Southeast Asia results in tremendous increases in GHG emissions.

To determine what level of BBD increase could be supported without worsening these negative effects, we performed a technical analysis examining the availability of domestically produced biodiesel feedstocks. We used production and consumption projections to calculate future availability, and we identified several important production and consumption trends.

We found that vegetable oils and animal fats are projected to increase as agriculture and livestock production increase. However, the production of yellow grease (from used cooking oil) cannot be expected to rise without the introduction of household collection programs and public awareness campaigns. We also expect that the production of inedible corn oil will most likely remain constant as corn ethanol production levels off.

It is important to remember that increased production and increased availability of feedstocks are not the same thing. There are several industries besides biodiesel that consume large amounts of these feedstocks. For example, vegetable oils, the main input to biodiesel production, are consumed in edible products at a rate almost triple that of use in biodiesel. Vegetable oils are also used in livestock feed, oleo chemicals, and other industrial products. Animal fats are used heavily in the production of livestock feed and industrial products. Yellow grease and inedible corn oil are also used in livestock feed. These other industries must be considered when assessing how much feedstock can be used for biofuel.

It’s a common belief that the production of biodiesel can be increased sustainably by using resources that are otherwise being wasted. However, with the exception of trap grease (which is currently too expensive to convert to biodiesel), all available resources are already being used in other industries, with very little waste. If resources that are already in use are diverted to biodiesel, then different fats or oils will have to be substituted. Unfortunately, in many cases the substitute is palm oil because of its low price and elastic supply.

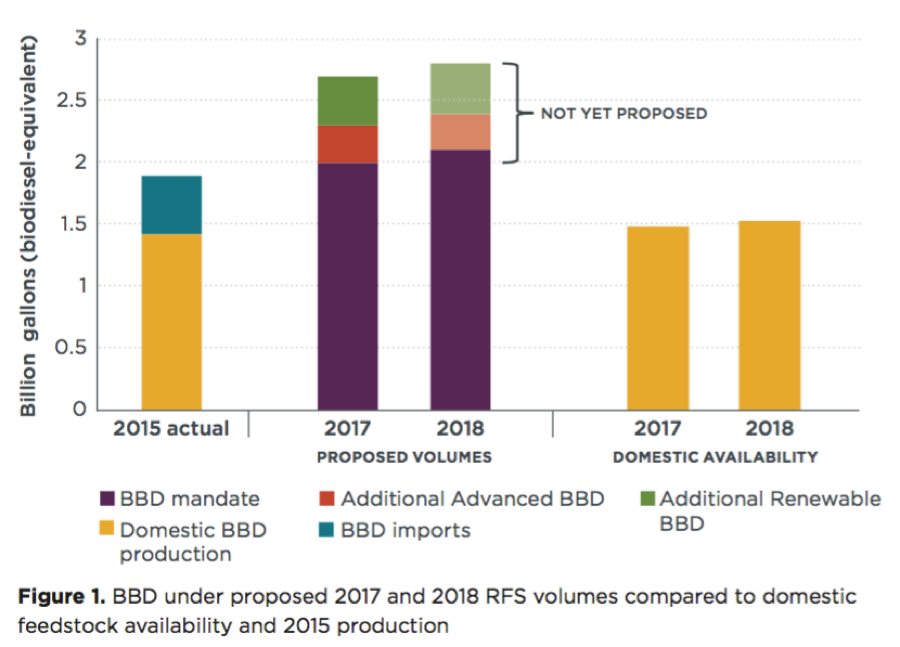

We still expect production of fats, oils, and greases to increase faster than consumption, resulting in a net gain in feedstock availability. We project that an increase of 120 million biodiesel-equivalent gallons of feedstock will be available in 2018, compared with 2015, as shown in the figure below. But the EPA has mandated a BBD increase of more than three times that volume (370 million biodiesel-equivalent gallons) over that period.

Moreover, the amount of BBD needed to satisfy the proposed 2018 requirements is likely to be greater than the amount specified in the BBD mandate. Because of the ethanol blend wall, or the amount of ethanol that can be blended into gasoline, BBD is expected to fulfill the increased mandates for advanced and renewable biofuels in addition to the BBD mandate. The gap between total BBD volume implied by the mandate and what can be produced using domestically available feedstock must be filled either by greatly increased imports of feedstock and/or BBD or by feedstock switching (likely to palm oil) in non-fuel sectors.

Based on our analysis, we believe that the BBD mandate is unsustainably high and should be reduced to more closely reflect domestic feedstock availability. Minimizing both indirect impacts on nonfuel sectors and imports of BBD fuel and feedstock should be a priority for the RFS to achieve its goals of reduced GHG emissions and dependence on foreign energy.

When the RFS program was established, Congress intended for a shift by this point from first-generation biofuels toward cellulosic fuels, or ethanol derived from plant fibers rather than seeds and grain such as corn. We have submitted comments to the EPA recommending lower mandated volumes for all categories besides cellulosic. Cellulosic biofuels have the greatest potential for reducing GHG emissions without negative impacts on other industries and should represent most of the growth in future RFS mandates.