The second phase of China’s new energy vehicle mandate policy for passenger cars

Blog

How will the dual-credit policy help China boost new energy vehicle growth?

(This piece is also published by the California-China Climate Institute, here.)

When China’s national subsidy program for new energy vehicles (NEVs) started in 2013, only 1% of new light-duty vehicles sold were NEVs. (In China, battery electric, hydrogen fuel cell electric, and plug-in hybrid electric vehicles are classified as NEVs.) With the help of subsidies at both the national and local levels, that percentage reached 15.5% in 2021. The year prior, in 2020, China announced a goal of 20% NEV sales in 2025. But as the country will phase out its national purchase subsidy program this year, how will China keep supporting its NEV targets? The main national regulatory approach is the NEV mandate or “dual-credit” policy, and here we’ll analyze its role in shaping NEV growth trends to 2025.

The dual-credit policy is a way of referring to the Parallel Management Regulation for Corporate Average Fuel Consumption and New Energy Vehicle Credits for light-duty vehicles, a regulation adopted in 2018. It’s partially modeled after California’s pioneering Zero Emission Vehicle (ZEV) program and adds a parallel management component that connects manufacturers’ fuel economy performance with their NEV credit performance.

Manufacturers are required by corporate average fuel consumption (CAFC) credit requirements to make fuel-efficient vehicles, and to meet NEV credit requirements, they must produce NEVs. If manufacturers exceed the set targets, they have extra credits; non-compliance, meanwhile, results in deficits. Importantly, and as detailed in Table 1, there is a one-way street via which NEV credits can be used to offset a CAFC deficit, but manufacturers with extra CAFC credits cannot use those to offset an NEV deficit.

Table 1. Compliance pathways in China’s dual-credit policy in the case of a deficit (from Chen & He, 2021).

| Deficit type | Compliance strategies |

| NEV deficit

(Actual NEV credits < NEV targets) |

Purchase NEV credits from other companies.

Use banked NEV credits from own company. |

| CAFC deficit

(Actual CAFC credits < CAFC targets) |

Use banked CAFC credits from own company.

Transfer CAFC credits from affiliated companies. Use banked or current year NEV credits from own company. Purchase NEV credits from other companies. |

NEVs have lower fuel consumption or count as zero fuel consumption and thus automatically lower a manufacturer’s fleet average fuel consumption and help them meet the CAFC targets. Indeed, nearly 80% of NEVs in China are pure electric. Moreover, these vehicles generate NEV credits that not only contribute to NEV compliance but can also form a potential reservoir of credits to be used to achieve CAFC compliance.

To see how this works in practice, let’s look at some empirical evidence. China tightens its fuel economy standards for light-duty vehicles every year, and the total CAFC deficits in the market have grown quickly in recent years. In 2020, total CAFC deficits exceeded credits for the first time, and this means that manufacturers had to use their own banked NEV credits from prior years or purchase NEV credits from others to fill the gap. The fleet average fuel consumption target will continue to be lowered from 5 L/100 km in 2020 to 4 L/100 km in 2025 and the growing demand for CAFC credits will continue to motivate manufacturers to produce more NEVs.

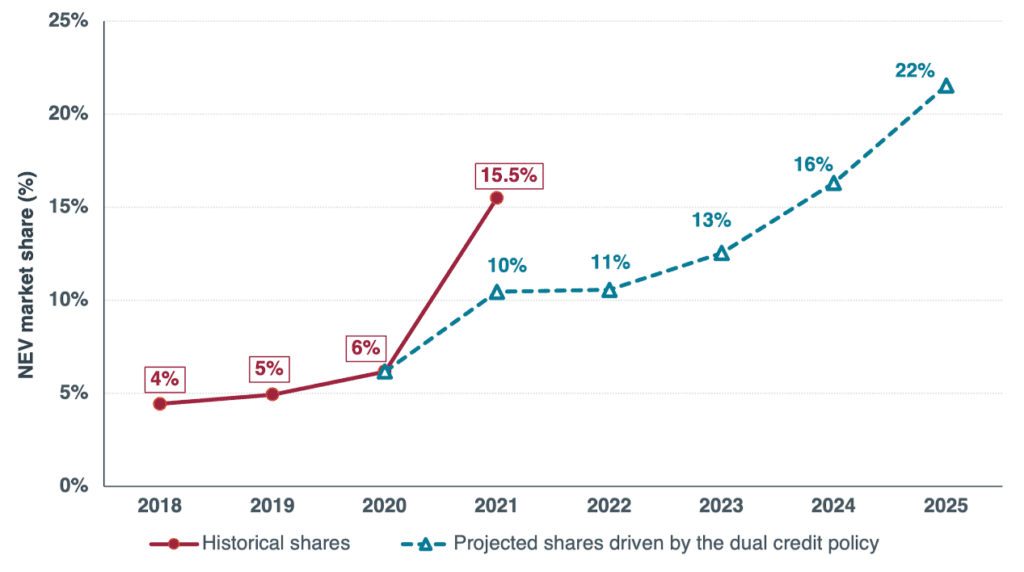

Our analysis in Figure 1 shows that if all manufacturers comply with the dual-credit policy requirements and aim at zero credit deficits, the share of NEVs in new light-duty vehicle sales will grow to 11% in 2022 and about 22% in 2025. In other words, the dual-credit policy alone would double the NEV market share in the next 3 years. As detailed under the figure, this is underpinned by a variety of assumptions that are based on existing trends. Certainly, though, actual NEV sales will depend on factors like consumer demand, model availability, charging infrastructure development, technology advancements, and other NEV incentive policies. As evidenced in 2021, NEV sales exploded in the second half of the year as a result of multiple policy pushes. The NEV sales share of 15.5% from 2021 far exceeds the 10% of sales that we projected would be solely driven by the dual-credit policy. So, looking back, we could say the 2021 NEV credit target was set too low, given there were many parallel incentive policies.

Figure 1. Historical and projected shares of NEVs in new vehicle sales driven by the dual-credit policy, 2018 to 2025. Note: The current dual-credit policy only covers 2021–2023. This calculation assumes that the NEV credit target will grow at the same rate from 2023 to 2025 as it did from 2021 to 2023, which means an 18% target in 2023, 20% target in 2024, and 22% target in 2025. This analysis also assumes that: (1) all auto manufacturers comply with the dual-credit policy requirements and aim at zero credit deficits; (2) from 2021 to 2025, the fuel economy of conventional vehicles will follow the average decline rate of the last 5 years (-1.68%) because of consistent changes in engine and transmission technologies; (3) the sales of conventional vehicles will decline by 7.2% per year, which is the average rate in the last 4 years; and (4) the average range of battery electric vehicles will be 350 km, 400 km, and 450 km in 2021, 2022, and 2023 and stay at 450 km thereafter. If the actual ranges are lower than these values, the share of NEVs will be higher than shown.

But are manufacturers motivated to comply with the dual-credit policy when there are currently little or no penalties for noncompliance? Companies that failed to meet the credit requirements in China were not identified to the public until 2021 and even now, we don’t know whether their failure had any consequences. In contrast, California charges $5,000 per ZEV credit in the case of a deficit.

Under situations of weak enforcement, manufacturers are typically only going to be motivated to comply if they can benefit from a given policy. How does that apply here? Well, based on calculations from Tesla’s reporting of regulatory credit revenues and ZEV credit balances from participating U.S. states, each ZEV credit was worth $2,169 in the United States in 2017. (After 2018, Tesla stopped separating ZEV credits from other regulatory revenues in its reporting.) Based on the 2017 value, an electric vehicle with 3–4 credits could thus generate between $6,507 and $8,676 for the manufacturer. That compares favorably with the $7,500 U.S. federal tax credit that’s gradually being phased out. In China, however, revenues from NEV credits have been below subsidies in previous years and were only beginning to be on par in 2021. Tesla received direct subsidies of CNY 15,840 ($2,481) from the Chinese government for each Model Y it produced in 2021. Meanwhile, because the Model Y is assigned 4.59 NEV credits under the dual-credit policy, it’s worth CNY 11,934 ($1,870) – CNY 13,311 ($2,085) in the current credit market. (This is based on the China Automotive Technology & Research Center’s estimate that the credit price was in the range of CNY 2,600 – 2,900 in 2021.) After China ends the subsidies in 2022, credit revenues will be the main financial benefits for NEV producers.

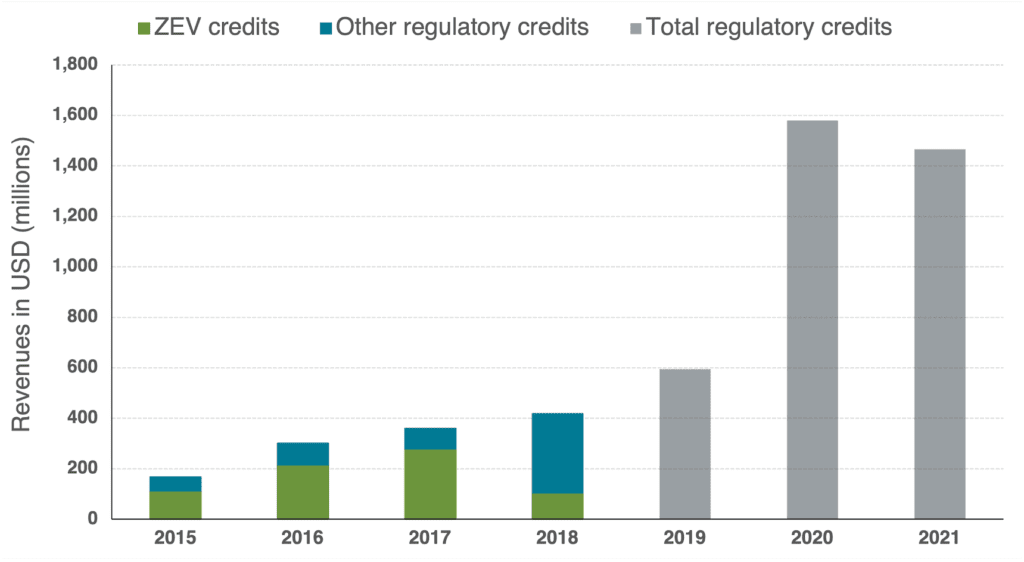

Indeed, Tesla is a great example of how manufacturers can benefit from various regulatory credits. As shown in Figure 2, Tesla’s revenues from credits steadily increased to more than $1.4 billion in 2020 and 2021. In 2020, Tesla made an annual profit for the first time thanks to $1.58 billion in revenues from regulatory credits. This included gains from ZEV credits and greenhouse gas credits in the United States, NEV credits in China, manufacturer pooling in Europe to comply with the CO2 standards, and more. Tesla is illustrative of how regulatory credits can achieve multiple benefits, including revenues that surpass direct subsidies for manufacturers, reduced fleet-average CO2 emissions, and growth in the electric vehicle market. With China’s dual-credit policy, domestic electric vehicle manufacturers such as BYD and SAIC will also be able to benefit from trading in the credit market.

Figure 2. Tesla global revenues from regulatory credits between 2015 and 2021. Source: Tesla Annual Financial Results.

Granted, the dual-credit approach has its limits. One of them is the perverse incentive for manufacturers to not improve the fuel efficiency of conventional vehicle fleets. This is an inherent consequence of the unidirectional credit flow from NEV to CAFC and suggests the Chinese government is encouraging the fast deployment of NEVs at the cost of internal combustion engine fuel efficiency. The dual-credit policy has thus far proved to be effective in promoting NEVs and is expected to be crucial to meeting China’s NEV 2025 goal of 20%. And with additional supportive policies, China can achieve even higher NEV pentration than that. As we’ve estimated, in 2021, the dual-credit policy requirements led to a 10% NEV sales share, while the actual NEV penetration in the market was 15.5%. Therefore, creating more stringent NEV credit targets for the next few years would better project the potential of policy synergies.