Press release

Contracts for Difference could help to expand ultralow-carbon fuel production in California [press release]

While there is a strong need to bring down the greenhouse gas emissions from transportation fuels, existing incentives for ultralow-carbon fuel production don’t do enough to bridge the gap and bring those fuels into full-scale commercial production. One of the biggest factors holding back investment in next-generation fuel production is the investors’ perception of policy and market uncertainty for alternative fuels.

A new study released today by the International Council on Clean Transportation argues that a Contracts-for-Difference (CfD) policy, similar to a policy already implemented in the United Kingdom to support renewable electricity, could provide the necessary confidence to spur investors to support larger projects. The new policy would be funded by California’s Greenhouse Gas Reduction Fund and provide price-certainty to ultralow-carbon fuel producers.

A CfD works by contractually setting a price floor on a unit of qualifying, ultralow-carbon fuel with a specific producer. Whenever the market value of that finished fuel (i.e., the sum of its sale price and any applicable credits and subsidies) is lower than that price floor, the guarantor of that contract (in this case, California) would pay the difference between those two values. As in the U.K., the price floors would be set via a reverse auction, wherein interested producers compete for contracts by bidding down the strike price to the lowest price their project could support.

The study finds that a CfD can be a cost-effective method to support new fuel production by leveraging the spending of other, existing policies. So long as the strike price is relatively close to the sum of a fuel’s sale price and existing incentives, this policy’s spending can be minimized. The CfD only kicks in whenever the policy or market conditions drop the value of fuels and incentives—whenever conditions are good, the program can actually accrue funding to prepare for future downturns.

“We found that the perceived value of many existing financial incentives is much lower than their face value,” says Nikita Pavlenko, a fuels researcher with the ICCT and a co-author of the study. “What this means is that investors discount the present day values of policies to account for future uncertainty. A CfD acts as a type of insurance or hedge against that kind of risk.”

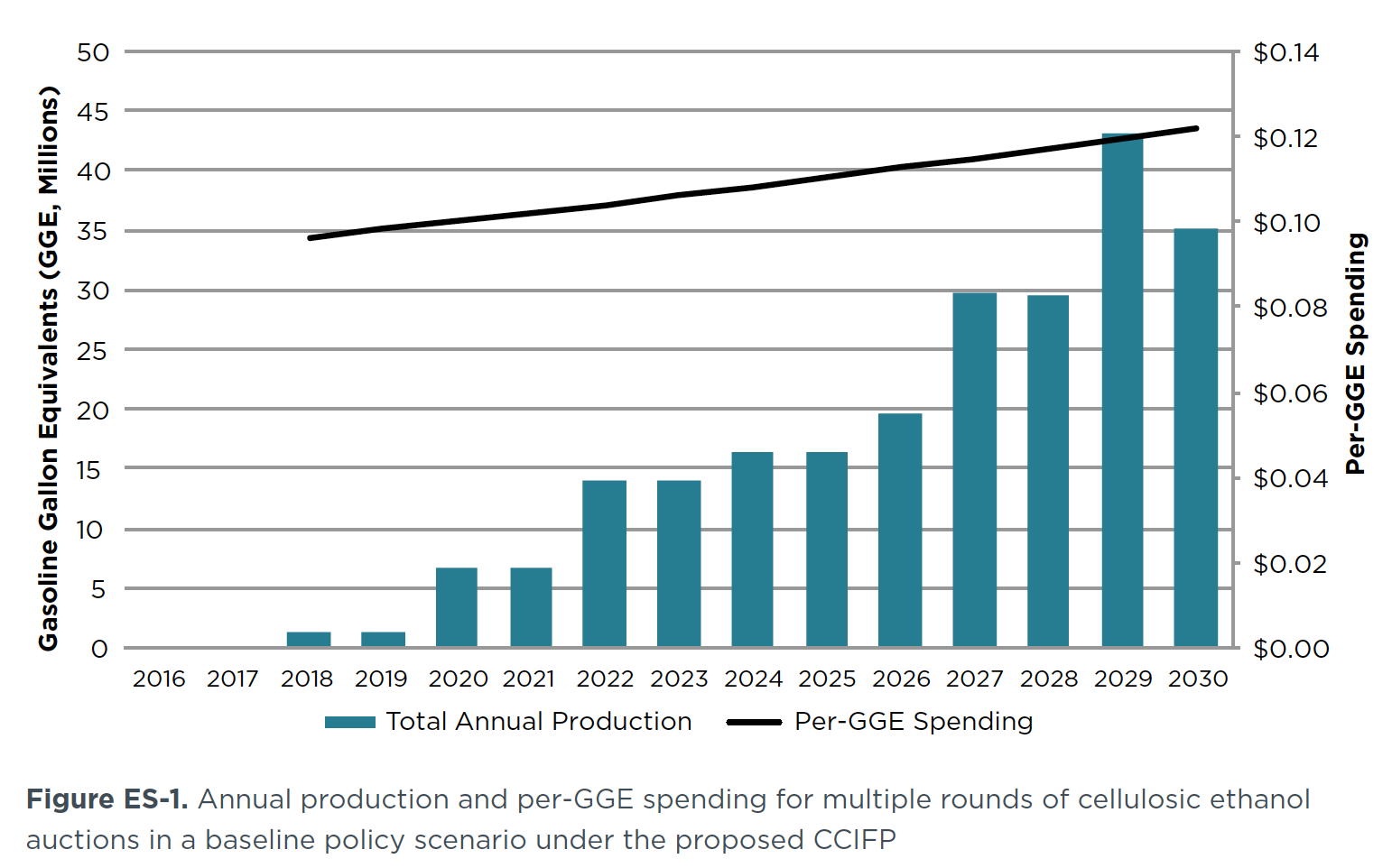

The cost model developed in the study suggests that in a business-as-usual baseline policy scenario, assuming the Renewable Fuel Standard (RFS) and Low-Carbon Fuel Standard (LCFS) exist through 2030, a CfD policy could accrue revenue and support additional and larger projects over time. While the CfD fund would underspend annually in order to accrue funding to protect against liabilities during down years, the volume of fuel supported would grow from 4 million gasoline gallon-equivalents (GGE) of cellulosic ethanol in the first auction to nearly 50 million GGE of annual production by 2028.

Publication details

Development and analysis of a durable low-carbon fuel investment policy for California

Authors: Nikita Pavlenko, Stephanie Searle, Chris Malins, and Sammy El Takriti

Contact: Nic Lutsey, ICCT fuels program director