A conversational guide to Renewable Identification Numbers in the RFS2

Blog

Does biodiesel really need a tax credit?

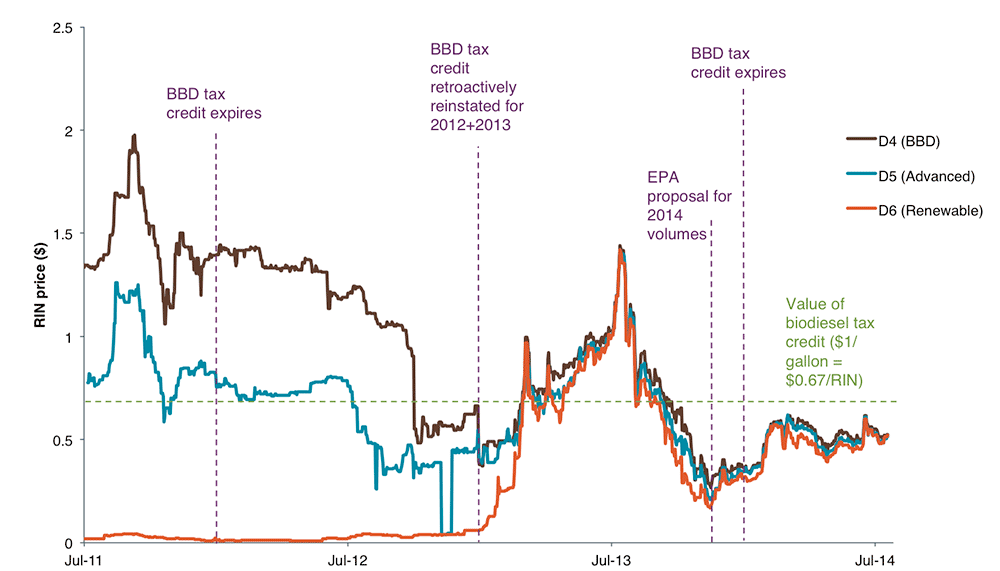

Prices of Renewable Identification Numbers (RINs)—essentially tradable credits used for compliance with the Renewable Fuel Standard (RFS)—have hovered around 50 cents since early this year for all types of biofuel. Two things about this trend are surprising: (1) D6 RINs, mostly reflecting corn ethanol, are this high, and (2) D4 RINs for biomass-based diesel (BBD, i.e., biodiesel) are this low.

Historical RIN prices and biodiesel tax credits.

The RIN prices for different classes of biofuels were never expected or intended to be the same. A RIN basically closes the price gap between what a refiner or blender would be willing to pay for the energy value of a batch of biofuel and the price for which the producer is able to sell it. This additional value support has been necessary to push large volumes of biofuel into the market because biofuel is generally more expensive than gasoline or diesel. Since some types of biofuel are more expensive to produce than others, the RIN price for each type should reflect a specific price premium. Also, the RIN categories are tiered: an advanced RIN can be used to meet the renewable mandate, but not vice versa, so the price of a D6 renewable RIN should never go higher than that of a D5 advanced RIN.

During 2011 and 2012, corn ethanol, which has been relatively cheap, was associated with a low D6 RIN price of 1 to 5 cents. For the most part, advanced ethanol (mostly from sugarcane) and biodiesel have been more expensive to bring to market and so the prices of RINs in the advanced and biomass-based diesel categories have been higher ($0.50–$1.50). Indeed, Congress had been convinced that biodiesel production was so expensive that in addition to support through the RIN price it needed a tax credit of $1/gallon. This is roughly equivalent to adding 67 cents value to every D4 RIN on top of the price on the RIN market.

This price picture changed in 2013, with a skyrocketing price for renewable RINs that lasted for most of the year and was widely thought to be a manifestation of blendwall anxiety (for example see this Reuters article) possibly combined with the impact on corn ethanol production costs of high corn prices following the drought of 2012. The idea is that faced with the volume of ethanol required by the RFS rising to meet a de facto 10% limit on the amount of ethanol that can be blended in gasoline, refiners and blenders started stockpiling RINs to avoid being caught out of compliance if they were unable to blend the requisite amount of ethanol in 2014. As noted above, because sugarcane ethanol and biodiesel can be used to meet the Renewable fuel mandate as well as the Advanced and Biomass-based diesel volumes, the price of a Renewable D6 RIN becomes a price floor for the D4 and D5 RINs. As an anxious market thrust up the D6 price in early 2013, it quickly rose above the historical price of the D4 and D5, from which point all three prices moved together. Eventually, the release of an EPA draft volume rule in late 2013 that proposed lowering the 2014 ethanol mandate appeared to calm the RIN market: prices declined and a price spread between biofuel categories crept back in, albeit with prices still much closer than in the past. However, in early 2014 the renewable RIN price rose again, and once again eliminated any significant price spread between RIN types. The fact that they’ve remained elevated since that point suggests refiners and blenders are again preparing for a potential future RIN shortage, perhaps suggesting that they fear the EPA will go back on its initial proposal and raise the ethanol mandate for 2014.

To bring us back to the tax credit, notice that Biodiesel (D4) RIN prices are still tracking D6 RIN prices. The Biodiesel Income Tax Credit has a tumultuous history of expiring and being reinstated, twice retroactively. This tax credit expired most recently on December 31, 2013 and has (so far) not been reinstated. Now, if biodiesel producers really needed a $0.67/RIN tax credit in order to sell biodiesel competitively in 2013, what would we expect to see in 2014 now the tax credit has expired? Unless the cost profile of biodiesel production has changed dramatically (and we have no reason to believe it has), we would expect to see the D4 RIN price increase by $0.67 from 2013 to 2014 to compensate for the loss of the tax credit. This didn’t happen. In fact, the average D4 RIN price this year has been lower than in any other year of the RFS.

There are a few ways that this behavior might be fully or at least partly explained. A first possibility is that the biodiesel industry is currently producing at a loss, in the hope/expectation that the tax credit will again be retroactively restored. It’s happened before and it’s being proposed again this year, so maybe biodiesel producers are keeping prices low despite low RIN prices in order to keep sales volumes up, hoping to cash in later. Whether or not most biodiesel companies have enough cash on hand to heavily subsidize sales for so many months is another question.

A second possibility is that the market is simply oversupplied with D4 RINs, and that therefore biodiesel producers will not be able to cover costs until supply falls back in line with demand. In this case, the market element of the RFS is working by ensuring that the least efficient producers will have to improve their margins or fall by the wayside.

However, there’s also a third possibly: that the tax credit isn’t necessary anymore. Technologies tend to get more efficient and cheaper over time. In fact, this was part of the logic of RINs—provide support to emerging biofuel technologies as they need it, and when biofuel prices come down RIN values would fade away. Maybe biodiesel production technology has gotten so much better since 2011—when the industry had both high D4 RIN prices and a tax credit—that it doesn’t need much of either of these supports anymore.

In April of this year, the Senate Finance Committee proposed restoring the biodiesel tax credit along with the cellulosic producers tax credit in a bill that has stalled and may not be voted on before the November elections. The biodiesel tax credit obviously has some support, especially from senators whose states are major producers. However, the behavior of RIN prices is starting to make it look as if the biodiesel tax credit is not only redundant (as the RFS should guarantee supply volumes) but may actually be driving windfall profits for the biodiesel industry—a transfer of wealth from taxpayers to biodiesel producers with little marginal benefit to the public.

We’ve argued in the past that cellulosic biofuels need solid, long-term support to bridge the valley of death to commercialization, and that for these high-capital-expenditure, first-of-a-kind facilities the cellulosic producers’ tax credit is an important complement to the RFS. In contrast, biodiesel is an established industry with low capital costs and a well-understood business model, and we don’t see any evidence that it still needs this extra support. Reinstating this tax credit would certainly serve the interests of the biodiesel industry, but the RFS—and the rest of the country—are fine without it.