A story of transition: How Europe’s faring in its move to zero-emission trucks and buses

Blog

Europe’s electric truck market surges, while electric buses power ahead

By now, you’ve probably come across an electric bus, but how about an electric truck? If you haven’t spotted one yet, you’re not alone. Despite the rapid growth in electric truck sales in the EU, with volumes more than doubling every year, they still just account for less than 1% of total sales. So, let’s delve into EU’s market for electric trucks and buses—with the help of some interactive charts—to answer the million-dollar question: Are the current trends good or bad news for the climate? Spoiler alert: It’s a mixed bag.

First, let’s get our truck climate-action facts straight. The EU has committed to a legally binding target of net-zero carbon emissions by 2050 under the landmark European Climate Law. So, all sectors of the economy must deliver. Electric trucks are an indispensable part of decarbonizing road-freight transport (yes, also when looking at the complete life cycle). To bring that technology to the market, the European Commission has proposed a major update to EU’s CO2 regulation for trucks and buses: Almost all new trucks and coaches must cut their CO2 emissions by 90% in 2040, and 100% of city buses must be zero-emissions in 2030.

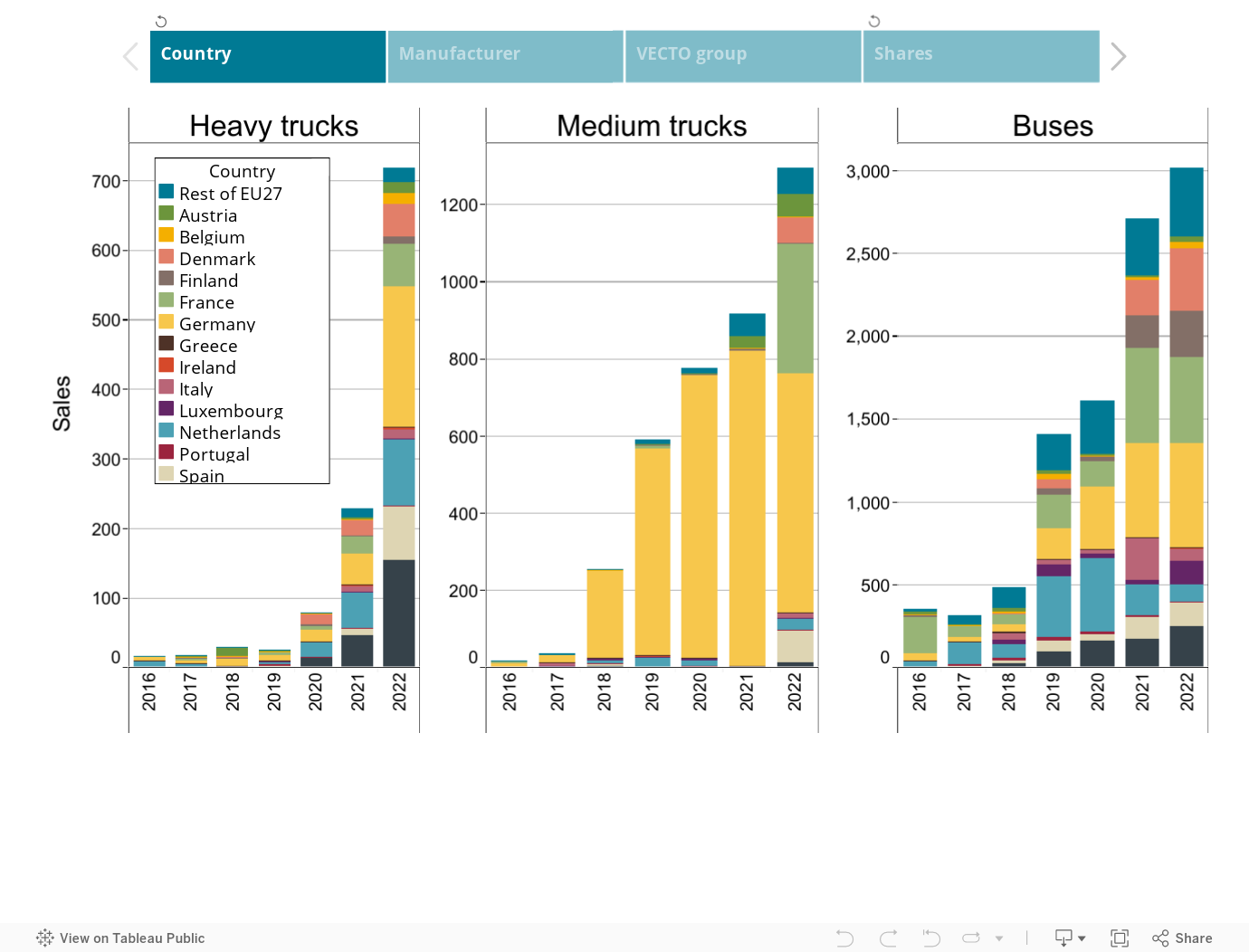

As far as sales, electric city buses are the star of the show. Their market share oscillated around 15% throughout 2021, jumping to almost 30% in 2022, and hitting 40% in the latest quarter of 2023. While some large Member States are still natural-gas-curious (looking at you France), others are unequivocal in their commitment to electric buses (yay, Denmark!). Still, this market share is nothing to boast about. In China, over 90% of new bus sales are electric. This has enabled Chinese manufacturers to set a strong footing in the European market, with BYD and Yutong grabbing 17% of it in 2022. In any case, e-buses have now become the dominant technology, enabling the sector to meet the proposed 2030 target.

Things are not as rosy for trucks, particularly for the heavy ones that move most of our goods. In 2022, about 260,000 heavy trucks were sold. Of those, just over 700 were electric. While this is a substantial growth compared to 2021, when less than 300 e-trucks were registered in the EU, it still amounts to just 0.3%. Germany, Sweden, and the Netherlands were responsible for the lion’s share of the e-trucks sales in 2022, collectively accounting for about 65%.

When slicing the data by manufacturer, the Volvo Group, with its two brands Volvo Trucks and Renault Trucks, was the clear market leader, placing about 55% of electric trucks on EU’s roads. The Traton group, particularly with its Scania brand, captured about a quarter of the market in 2022, exhibiting substantial growth compared to 2021. Daimler Trucks sales of electric trucks stayed at about the same level as in 2021. All three manufacturers are making the transition towards zero-emission trucks a central part of their strategies.

Now, how do we go from hundreds of electric trucks to hundreds of thousands of them in less than two decades? The answer lies in the confluence of several critical factors working together to propel electric trucks into the mainstream.

Let’s break it down:

First, electric trucks must beat diesel in their economic performance. ICCT’s research has shown time and time again (here, here, and here) that electric trucks can be cheaper to own and run than diesel ones in Europe before 2030, with no extra policy support needed. Dangle a few carrots and wave some sticks—think fiscal incentives, road toll exemptions, and carbon pricing—and electric trucks become the cheapest choice in some European countries already today.

Next up, we need to ensure the widespread availability of charging infrastructure. For fleets doing urban and regional deliveries, private depot chargers can handle a good chunk of their energy needs. Long-haulers, however, will need high-power en-route chargers. Luckily, the recently adopted Alternative Fuel Infrastructure Regulation (AFIR) ensures precisely that. Using ICCT’s charging infrastructure model, we estimate that AFIR will secure about three-quarters of the charging needs of electric trucks by 2030. This strong regulatory pull will boost market forces to bridge any remaining charging gaps.

Lastly—and most importantly—we need to ensure supply. With the demand and infrastructure lined up (talk about enabling conditions!), ambitious truck CO2 standards are needed to secure a steady supply of electric trucks. Truck manufacturers recently indicated that by 2030 they expect electric trucks will have a market share of 60%, with the sector becoming completely fossil-free by 2040. What they now need to make this happen is a leveled regulatory field to boost competition. Finalizing the ongoing legislative process before the European elections in 2024 will provide the regulatory certainty that companies need to plan their development cycles and make those long-term investments to meet the 2040 CO2 targets.

Achieving widespread adoption of electric trucks relies on aligning cohesive regulatory action and industry commitment. As these puzzle pieces come together, we’ll witness a gradual rise in electric truck volumes, transitioning from hundreds to hundreds of thousands. Rome wasn’t built in a day, and neither will the electric truck revolution. The diffusion of technology takes time, even if electric trucks boast lower costs and higher economic benefits. But achieving decarbonization of the road-freight transport in time to combat climate change is within our grasp. We can make this happen.