Blog

Finally catching up: What powers the EV uptake in Germany?

In the run-up to the European Union (EU) 2020/21 mandatory new vehicle fleet CO2 targets, the German passenger car market shows an increasing rate of electrification. This uptake is boosted by rising sales of battery electric (BEVs) and plug-in hybrid vehicles (PHEVs), both to a similar extent. In total, the number of electric vehicle (EV) registrations in Germany from January to October of this year (86,316) surpassed EV registrations in the significantly smaller markets of France (48,231), the United Kingdom (54,337), and Norway (67,653) in the same timeframe. Thereby, Europe’s largest passenger car market also became the largest EV market on the continent in absolute numbers. In relative numbers, the average new car EV share over the past 12 months in Germany (2.8%) caught up with France and the UK (both also at 2.8%) but is still far lower than in Norway (56.1%) or Sweden (11.0%).

In Norway, Sweden, France, and, to a lesser extent, in the UK, EV policies are based on a carrot-and-stick approach: A lower tax or even a cash bonus for EV purchases in combination with a higher tax (malus) for vehicle purchases with higher CO2 emission levels, following a polluter-pays principle. The German EV policy, in contrast, focuses mostly on subsidies and tax breaks without an emissions-based financial counterweight. At the national level, since mid-2016 the German government grants a 2,000 EUR subsidy (Umweltbonus) on the purchase of BEVs and fuel cell EVs, and 1,500 EUR on the purchase of PHEVs with a CO2 emission level below 50 g CO2/km. As a condition, the net list price of the vehicle must be below 60,000 EUR and the car company discounts the purchase price by the subsidy amount. In addition, since January 2019, taxes are reduced for new EVs used as company cars (64% of all new passenger cars in Germany in 2018 are used as company cars.) Apart from these national policies, several German states and cities provide additional EV purchase incentives. The development of the EV charging infrastructure is also supported by subsidies and tax benefits at the national, regional, and local level.

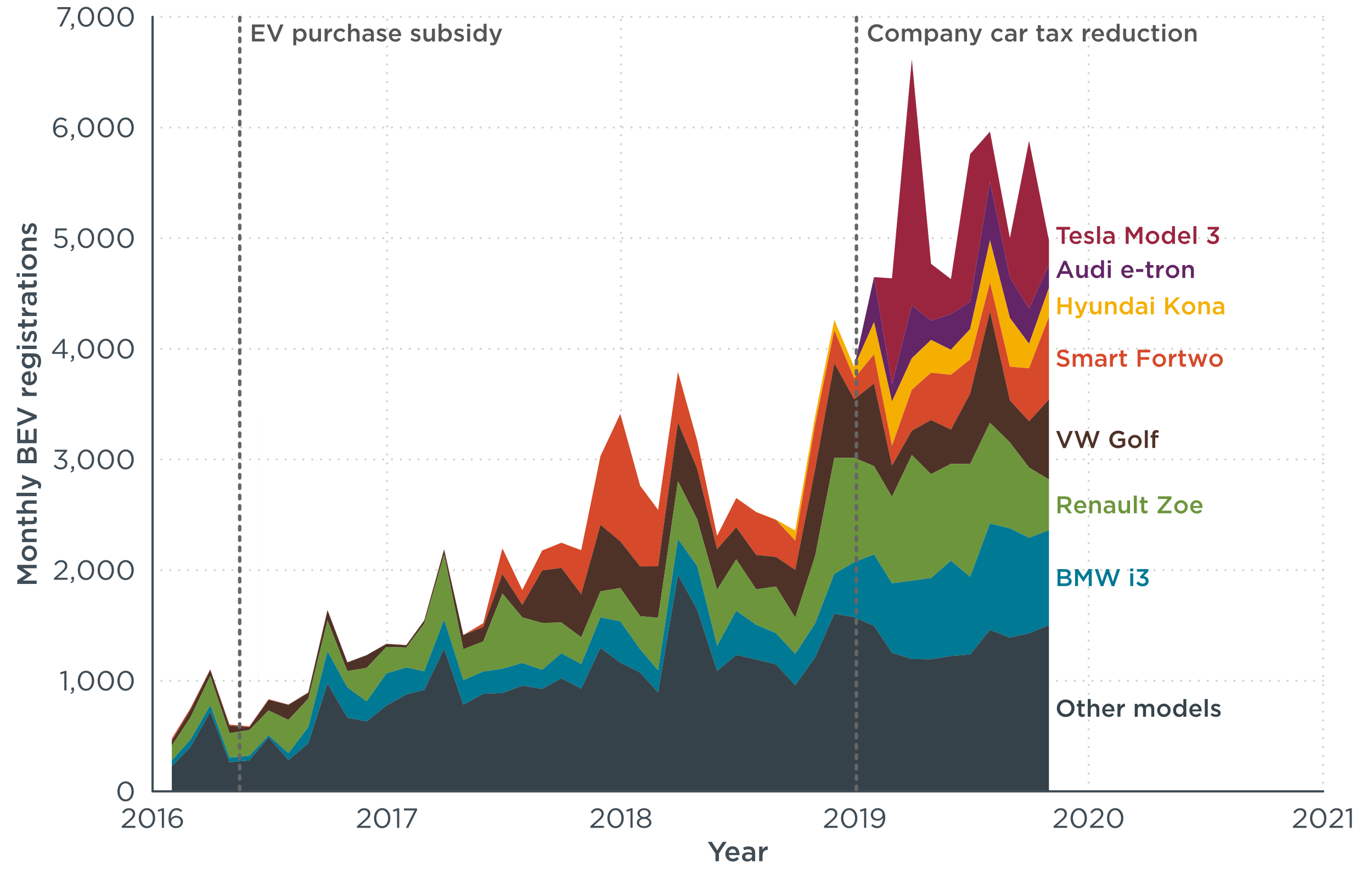

Since the EV purchase subsidy was introduced in mid-2016, the number of new registrations increased from about 1,500 to more that 10,000 per month in October 2019. The patterns of the BEV and PHEV markets, however, are quite different: While BEV registrations steadily rose, PHEV registrations suddenly dropped by 42% in late 2018 before rebounding by around mid-2019. So, what happened?

For BEVs, the increase in registrations strongly correlates with the introduction of new models. For instance, a battery update for the VW e-Golf and the introduction of all-electric Smart Fortwo and Forfour models resulted in a peak of BEV registrations in late 2017 and early 2018. Increased registrations of the Smart Fortwo BEV during this period are partly linked to the vehicles used in the refurbishment of Daimler’s former carsharing service ‘car2go’ in Stuttgart. Since the end of 2018, the BMW i3 and the Renault Zoe were updated with increased battery capacity, Tesla introduced the Model 3, and various manufacturers introduced battery-electric SUV models, like the Hyundai Kona and Audi e-tron. And again, we see the effect of a carsharing fleet being refurbished with BEVs, this time in mid-2019 when VW’s ‘We Share‘ in Berlin acquired 1,500 e-Golfs. The introduction of the reduced company car tax rate for EVs in January 2019 might have helped to spur new model BEV sales, in particular for upper-segment BEVs, such as the Audi e-tron or the Hyundai Kona.

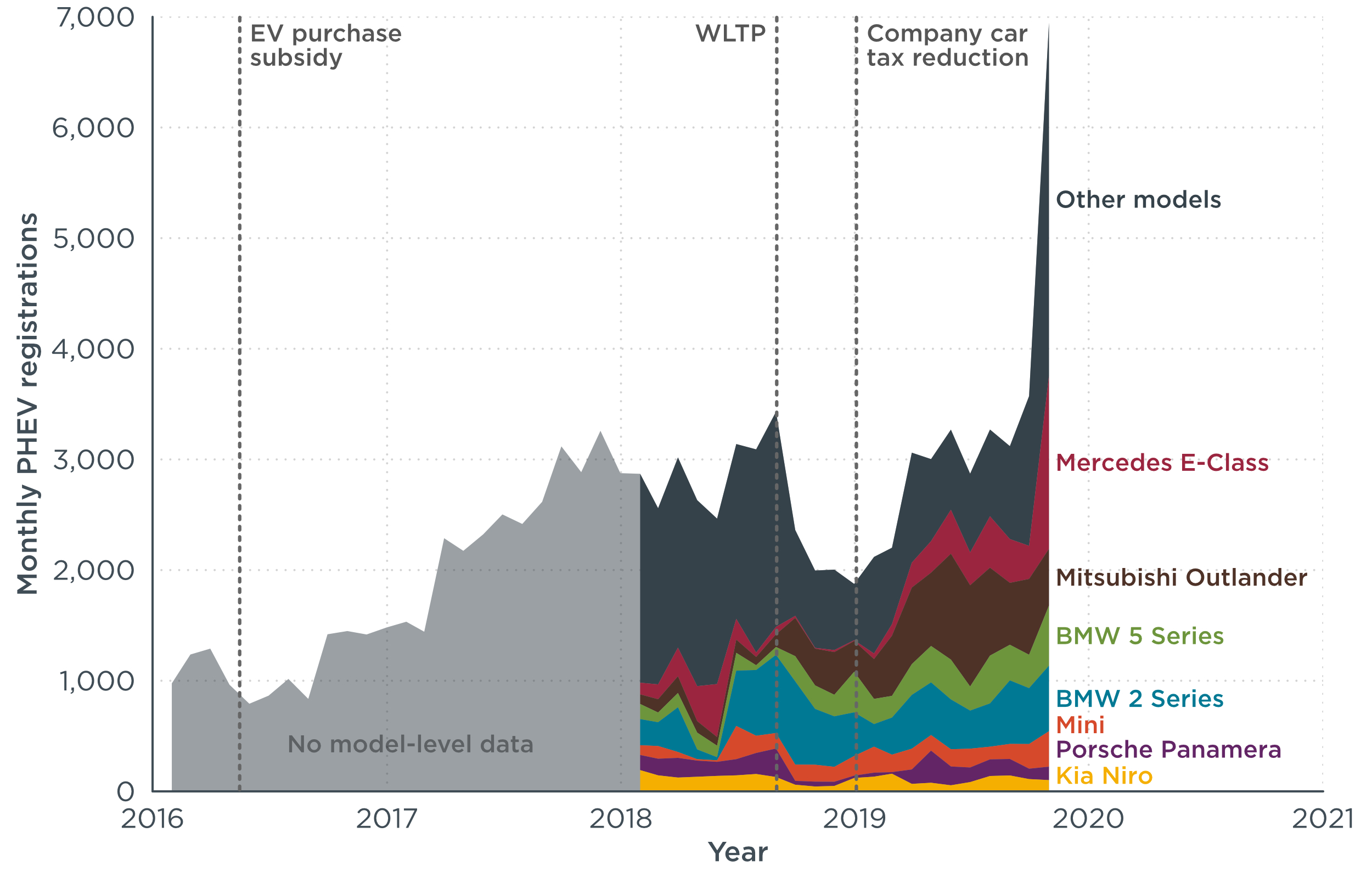

In contrast to the continuous growth of the BEV market, the PHEV registration numbers are more complex. Although we cannot differentiate new registrations of individual PHEV models before 2018, there is an increasing trend towards heavier and more expensive PHEV models such as Mitsubishi Outlander, Mercedes E-Class and BMW 5 Series in 2019. As many of these models are typical for company cars, it is likely that the introduction of the reduced company tax rate in January 2019, showed a stronger impact for PHEVs than for BEVs. The sudden doubling of PHEV registrations in October 2019, mostly comprised of new PHEV model versions of the Mercedes E-Class and C-Class, Porsche Cayenne, and BMW 3 Series, could be a sign that manufacturers are preparing for a stronger roll-out of EVs in order to meet the 2020/21 EU-wide CO2 targets for new cars.

There was a notable dip in new registrations of PHEVs between mid-2018 and mid-2019. This effect can be explained by the introduction of the WLTP in September, 2018. As a result of the new test procedure, type-approval CO2 emission levels for many vehicles increased, and a number of PHEV models turned out to be above the 50 g CO2/km threshold of the ‘Umweltbonus’ subsidy of the German government. PHEV registrations dropped by 42% as popular models, in particular from the Volkswagen Group, such as the Audi A3, VW Golf, VW Passat, Porsche Panamera, and Porsche Cayenne, were temporarily pulled from the market. Other models which still complied with the Umweltbonus subsidy criteria, like the Mini, BMW 2 Series, BMW 5 Series, and the Mitsubishi Outlander, continued to be registered in high numbers. This “WLTP-effect” indicates a strong dependence of the PHEV sales on the Umweltbonus subsidy and illustrates how narrowly the design of many PHEV models met the 50 g CO2/km threshold.

Beginning next year, the German government will increase the ‘Umweltbonus’ subsidy. From 2020 to 2025, the purchase subsidy for BEVs with a net list price below 40,000 EUR, will be increased from 2,000 EUR to 3,000 EUR, whereas the purchase of BEVs with a list price between 40,000 EUR and 65,000 EUR, will be subsidized by 2,500 EUR. Similarly, the subsidy for PHEVs with official CO2 emission values of below 50 g CO2/km will be increased from 1,500 EUR to 2,250 EUR and 1,875 EUR, respectively. In addition, the company car tax rate will be further reduced, from 0.5% to 0.25%, for vehicles with a net list price below 40,000 EUR. For battery electric delivery vehicles, an increased depreciation allowance of 50% will be introduced in 2020. Furthermore, several policy measures to support the extension of private, workplace, and public charging infrastructure were also announced.

In light of these planned tax breaks, in combination with EU-wide fleet targets and the application of ‘super-credits’, it seems likely that the EV uptake rate in Germany will remain high throughout the 2020 to 2021 time period. This is urgently needed, as EV market shares of 8-15% are likely required for VW, BMW, and Daimler to comply with their respective CO2 fleet targets in 2021. Whether the EV market growth in Germany will turn out to be stable beyond 2021 – without a carrot and stick like a bonus-malus system – is debatable and remains a subject for a future blog post.