Global Automaker Rating 2024/2025

Who is leading the transition to electric vehicles?

This third edition of the ICCT’s Global Automaker Rating report assesses how the world’s largest automakers stack up in the transition to ZEVs—that is, battery electric vehicles (BEVs) and fuel-cell electric vehicles (FCEVs). Focused on the top 21 light-duty vehicle manufacturers in the world by sales in 2024, we use 10 custom-built metrics to reflect automakers’ efforts and strategies in transitioning their vehicle fleets to zero tailpipe emissions and decarbonizing manufacturing processes.

AT A GLANCE

Tata Motors is the first automaker to transition from “Laggard” to “Transitioner.” In 2024, Tata introduced new EV models that diversified its offerings. Tata and subsidiary Jaguar Land Rover also ramped up efforts in battery recycling and repurposing in major markets.

Geely and Chery, both in the Transitioners group, showed the most improvement in scores compared with 2023. Geely and Chery increased their ZEV-equivalent sales shares by 12 and 9 percentage points, respectively, while offering new models, and both shifted sales toward high-performing models that improved the average performance of their new BEV fleets.

Automakers based in Japan and the Republic of Korea still lag behind, but Honda and Nissan have made progress. Honda introduced its first BEV model, the Prologue, in the United States, and its sales led to substantial improvements in all BEV performance metrics for the company. Nissan strengthened its ZEV ambition by separating its 40% by 2030 ZEV target from a previously announced target that included conventional hybrid vehicles.

Focused on the top 21 light-duty vehicle manufacturers in the world by sales in 2024, we use 10 custom-built metrics to reflect automakers’ efforts and strategies in transitioning their vehicle fleets to zero tailpipe emissions and decarbonizing manufacturing processes.

In this year’s rating, we introduce a new metric on green steel, update our battery recycling and repurposing metric to consider realized progress rather than just announcements, and update the methodology used to estimate the real-world operation of plug-in hybrid electric vehicles (PHEVs) in China, to reflect the latest research. Nevertheless, the consistency in our evaluation framework enables us to track automakers’ progress from 2023 to 2024.

2024 RATINGS

METRICS

The rating is designed around three pillars—market dominance, technology performance, and strategic vision—including three key changes to the assessment framework:

→ Replacing the renewable energy in manufacturing metric with a green steel metric that evaluates manufacturers’ current steel supply chains and efforts to procure green steel in the future

→ Refining the battery recycling assessment by scoring based on phases of efforts to include partial credit

→ Updated the methodology for estimating China’s real-world electric drive share of PHEVs by adopting the 2025 utility factor curve proposed by the China Automotive Technology & Research Center

- ZEV-equivalent sales share

- Class coverage

- Energy consumption

- Charging speed

- Driving range

- Green steel

- Battery recycling and repurposing

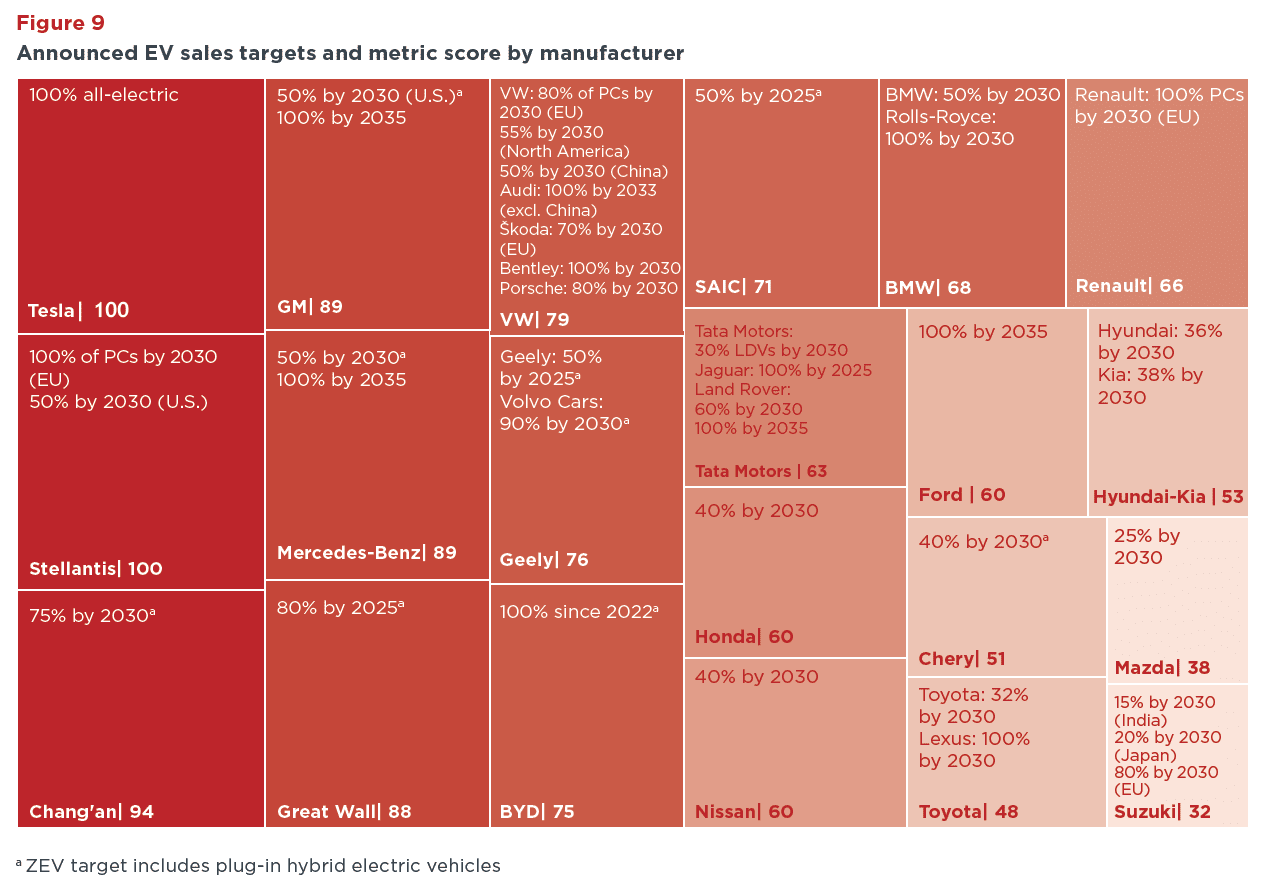

- ZEV target

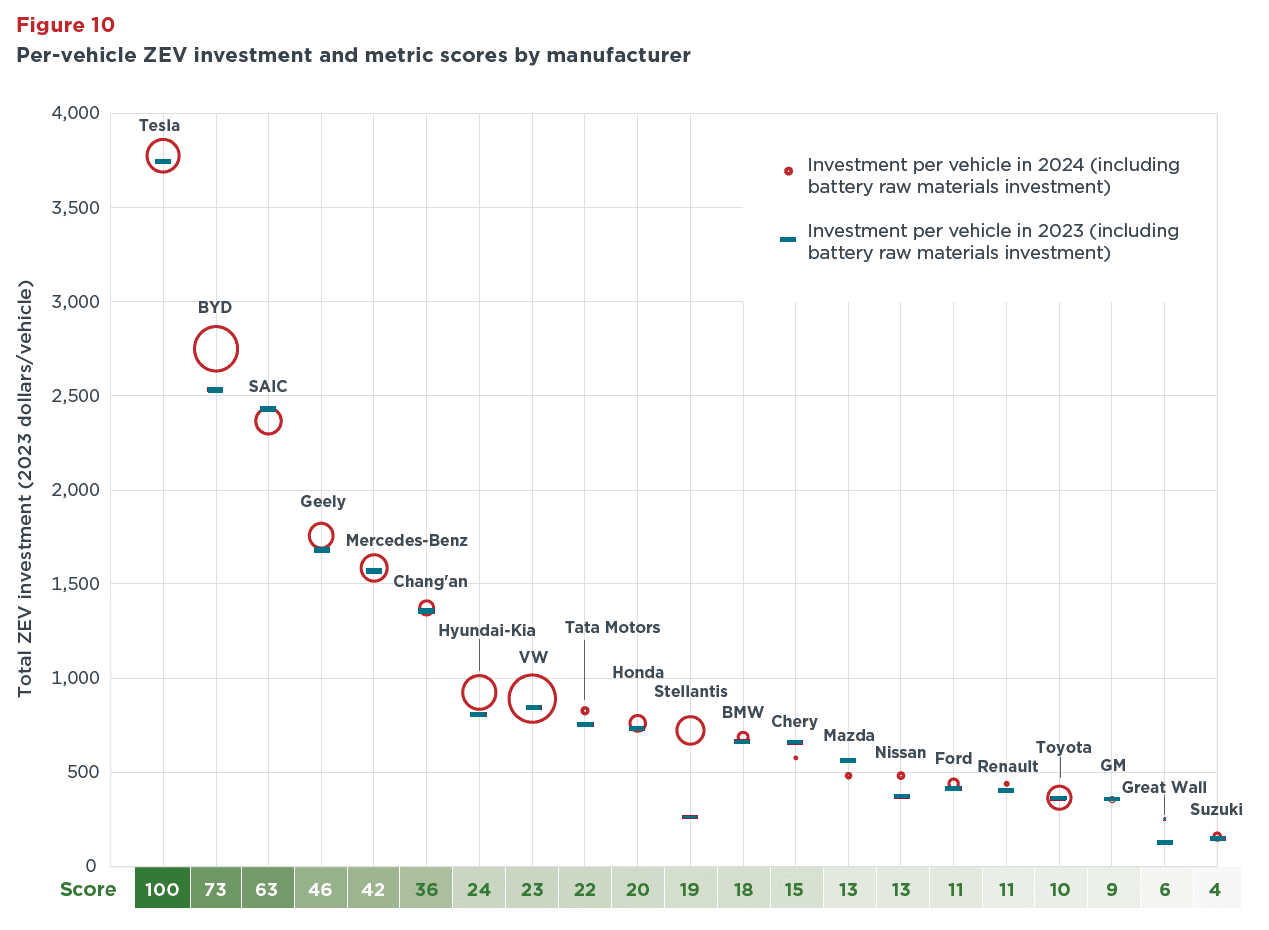

- ZEV investment

- Executive compensation alignment

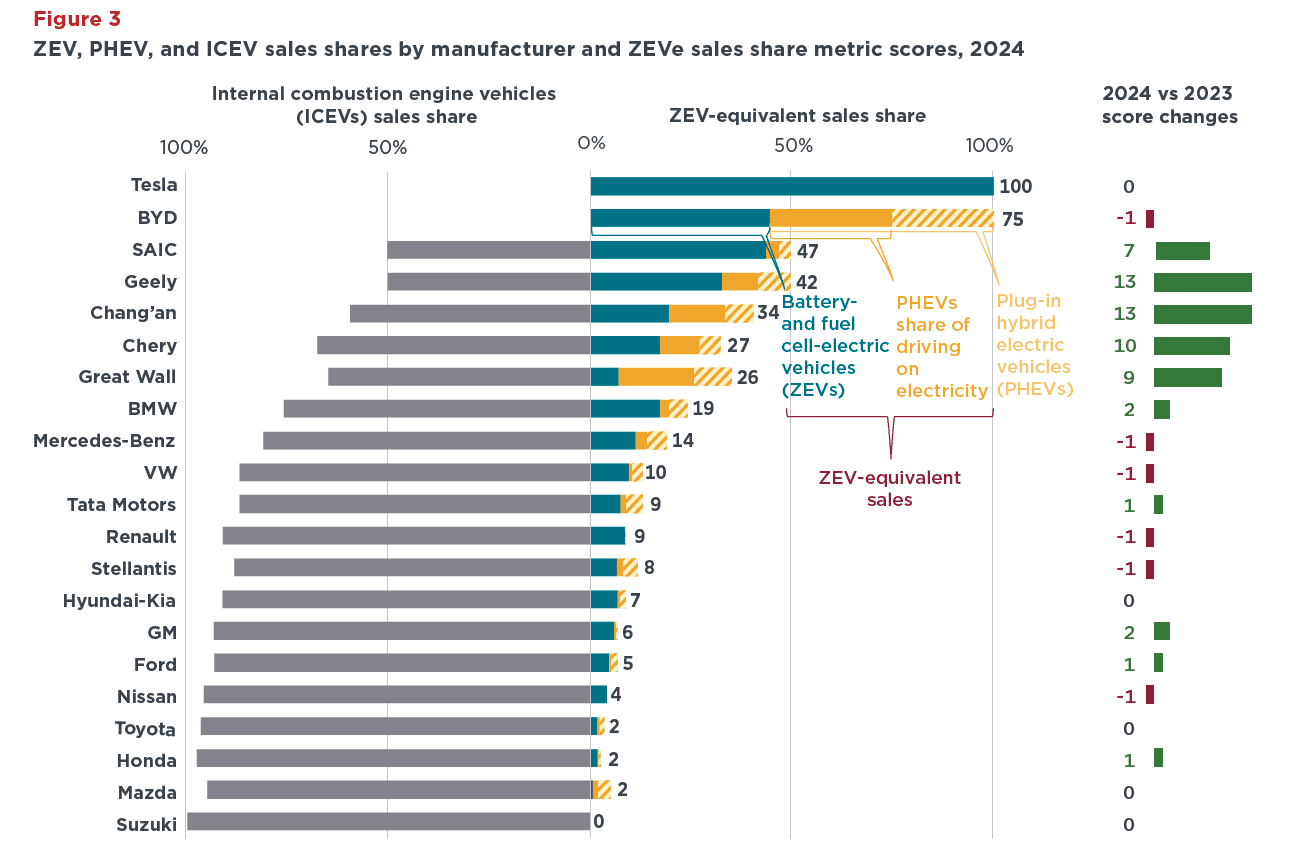

ZEV-equivalent sales share is the fraction of each manufacturer’s LDV sales that are BEVs, FCEVs, and PHEVs. Each PHEV was adjusted as a percentage of a ZEV using an adjustment factor based on the real-world electric drive share of PHEVs, estimated from recent studies.

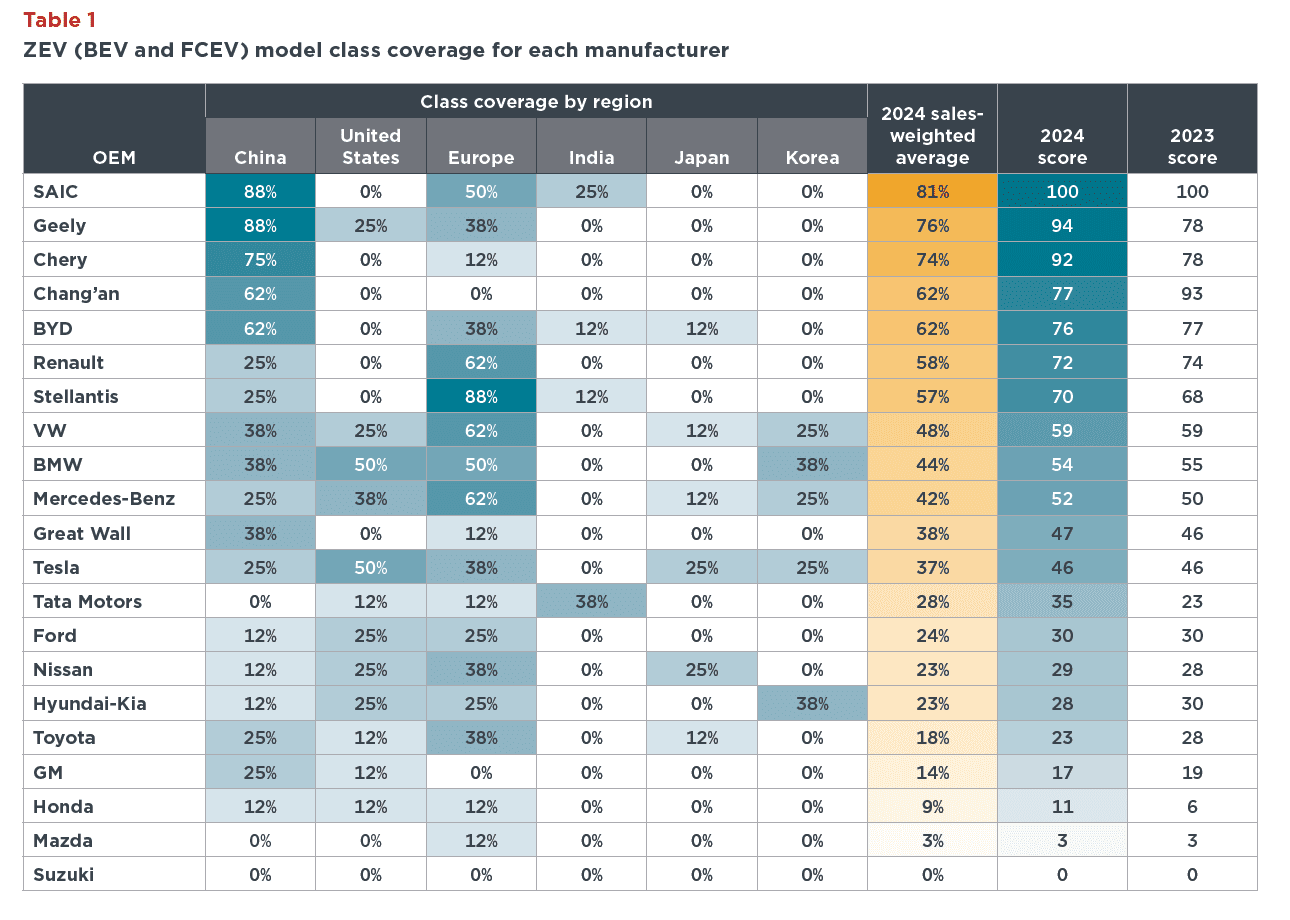

ZEV class coverage reflects the share of eight LDV classes, ranging from mini/ subcompact car to light truck, that are covered by model offerings from each manufacturer. To differentiate a manufacturer’s ZEV offerings by market, we considered a class to be covered if the manufacturer sold at least 1,000 ZEV units in one market.

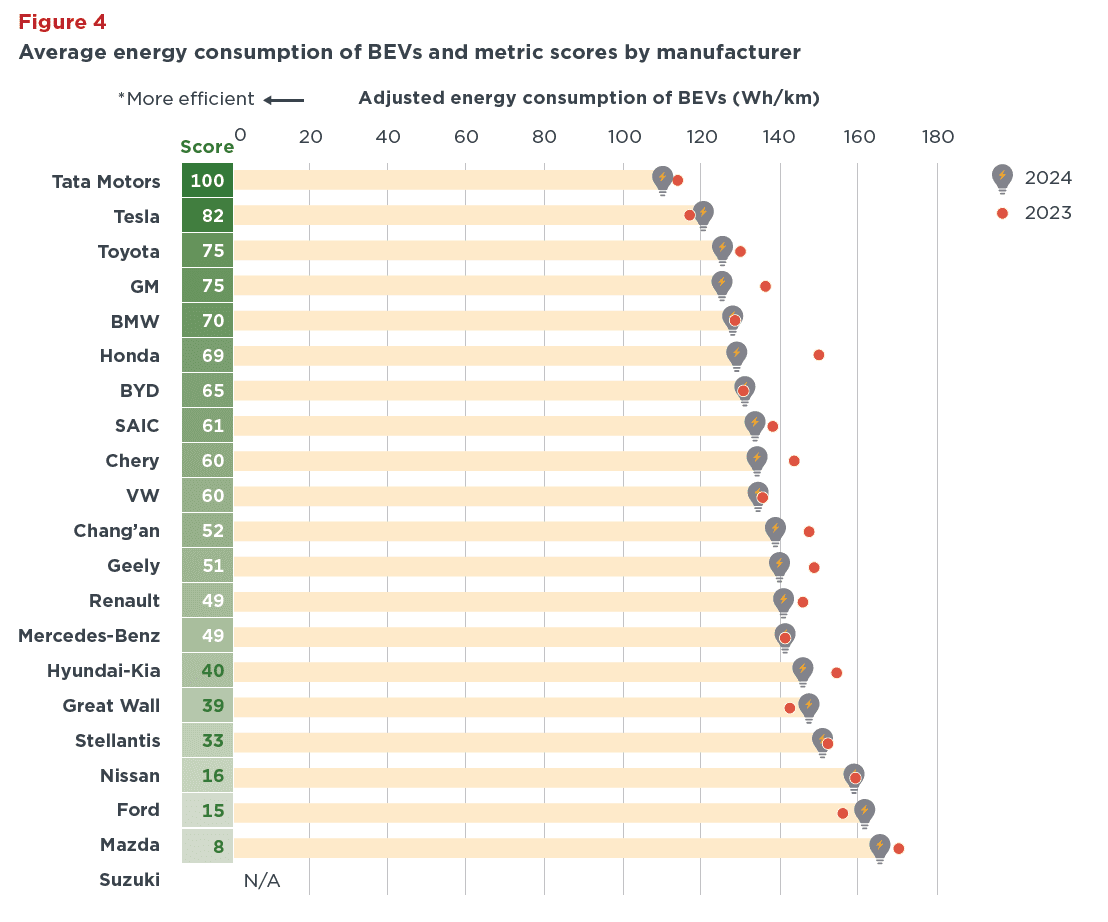

Energy consumption is the sales-weighted average of certified energy consumption of BEVs sold by each manufacturer, adjusted by vehicle weight and normalized to the same test cycle in units of watt-hours per kilometer (Wh/km).

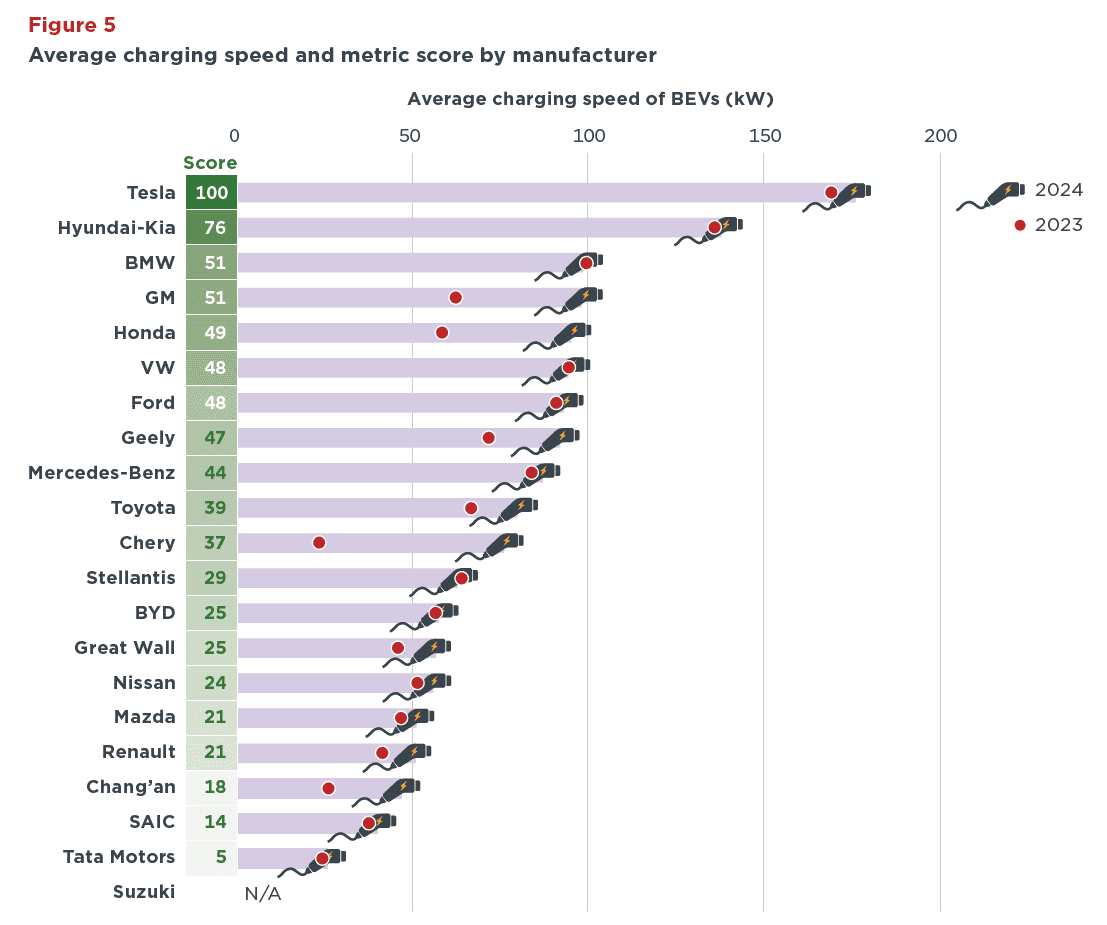

Charging speed is the sales-weighted average of charging speed of BEVs sold by a manufacturer, in kilowatts (kW).

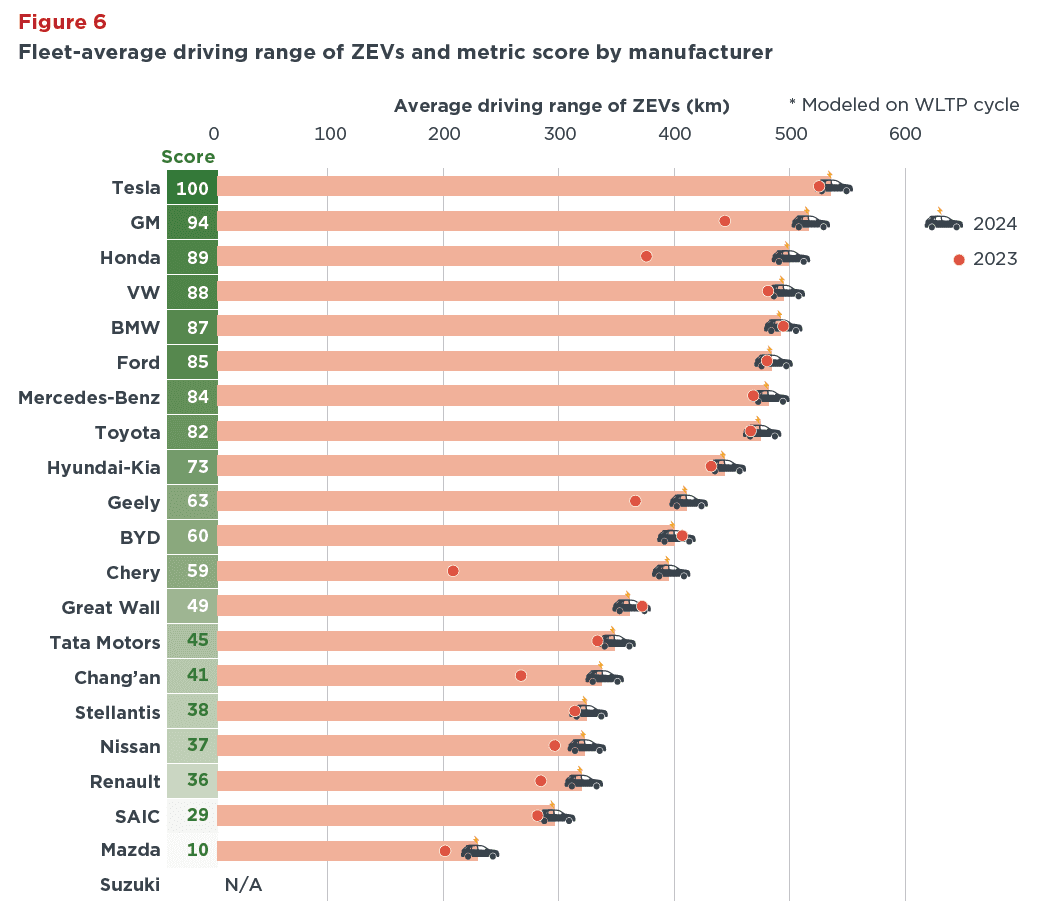

Driving range is the sales-weighted average of certified driving range of ZEVs sold by a manufacturer, normalized to the same test cycle and in kilometers (km).

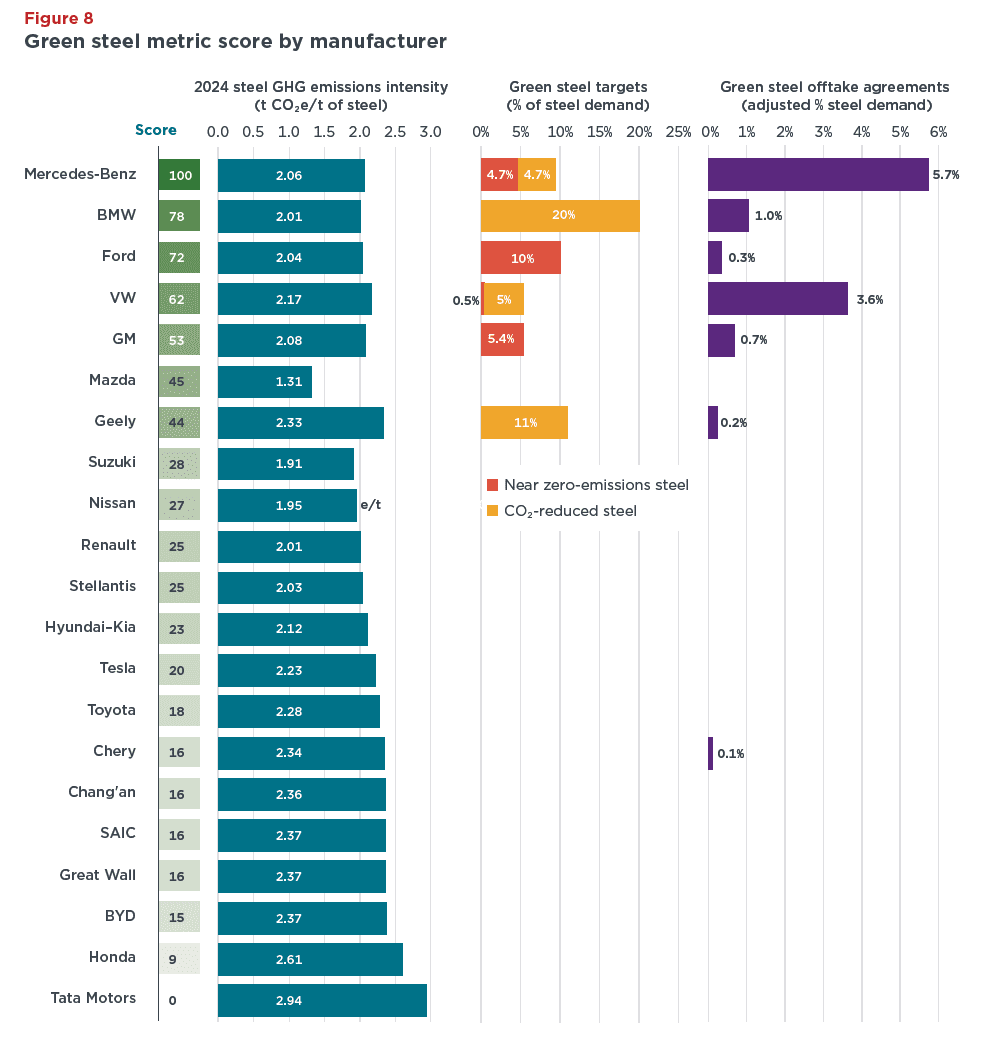

Green steel reflects manufacturers’ efforts to procure steel that has lower emissions during production compared with conventional steel production methods, with the goal of eventually sourcing steel that is free of fossil fuels.

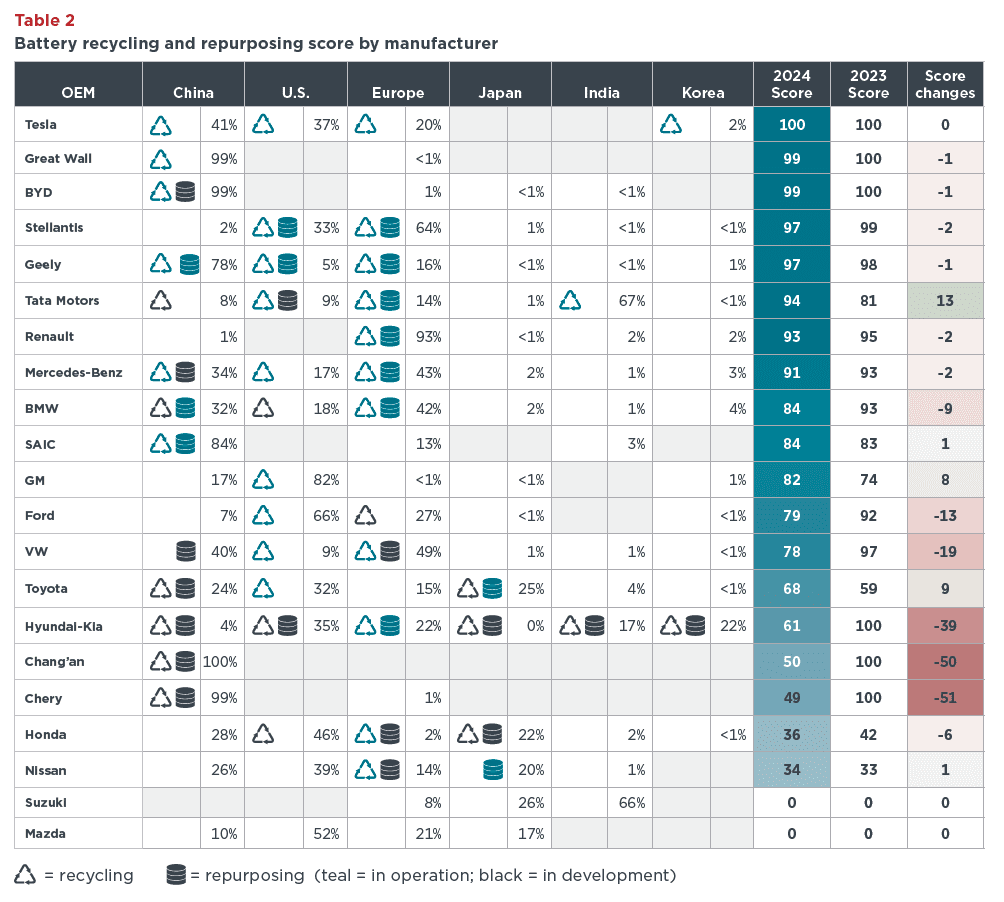

Battery recycling and repurposing assesses whether manufacturers have planned or implemented battery recycling or reuse projects.

ZEV target is based on each company’s stated ZEV sales share targets and dates and their degree of alignment with the ZEV sales shares needed to keep global warming below 2 °C. We evaluated mid-term 2030 targets and long-term 2035 targets if a manufacturer had both, and this allowed us to track progress throughout the transition.

ZEV investment includes total announced investments in ZEV and battery production sites, battery raw materials, charging infrastructure, and ZEV research and development relative to an automaker’s size.

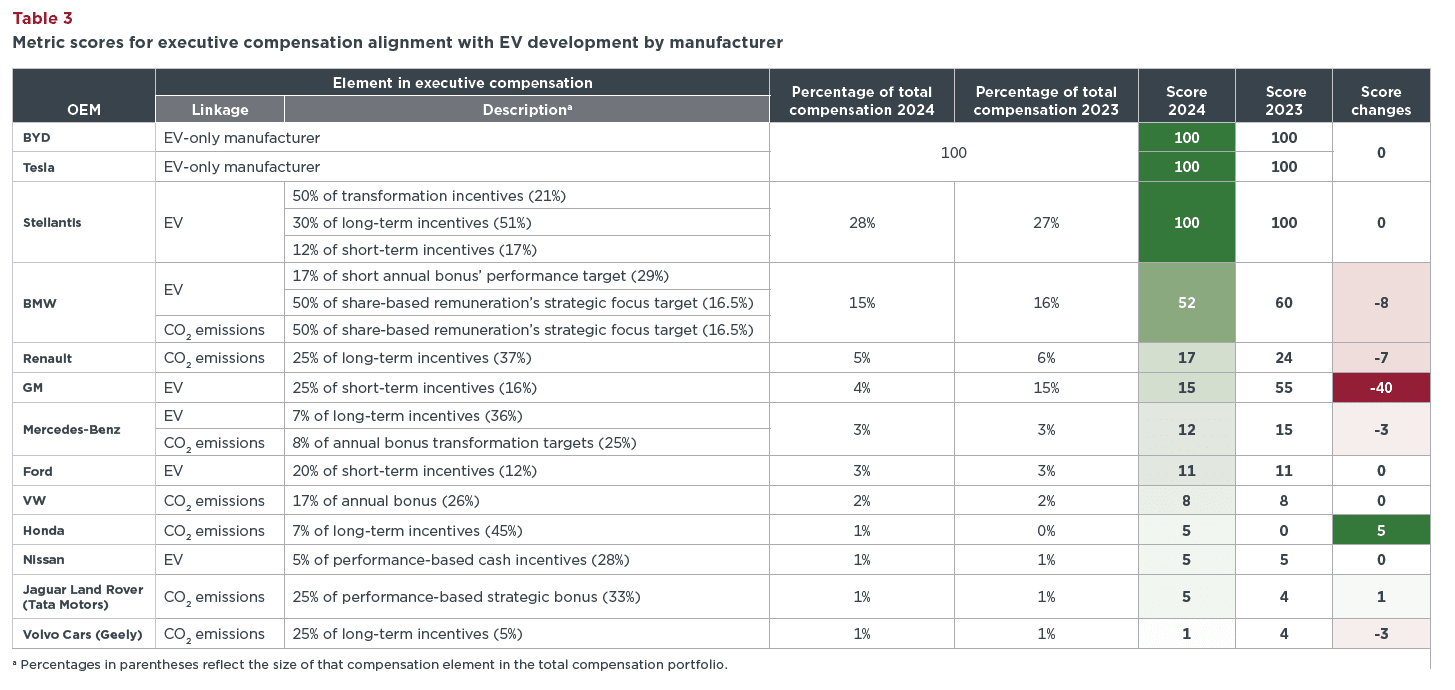

Executive compensation alignment reflects the extent to which an automaker’s top executive’s pay is tied to EV development. A manufacturer is awarded points for linking its executive compensation to parameters associated with EVs and carbon dioxide (CO2) emissions.

Notable trends

China-based automakers are far ahead in ZEV market dominance. Geely, SAIC, Chang’an, Chery, and Great Wall increased ZEV-equivalent sales shares by 6–12 percentage points from 2023 to 2024 while other automakers made much more limited progress or recorded declines. Geely and SAIC reached 50% EV (BEV and PHEV) sales shares before applying our adjustment factors for PHEVs and both met their 50% EV by 2025 target 1 year ahead of schedule. That China-based automakers also make up the entire top 5 in ZEV class coverage suggests that a wider variety of offerings supports their higher EV sales. Besides Geely and Chery, Tata Motors and Honda were the only automakers to diversify their ZEV model offerings compared with 2023.

There was widespread improvement in ZEV performance. Most automakers scored higher on average ZEV performance, including ZEV energy consumption (16 out of 21 improved), charging speed (16 out of 21), and ZEV driving range (17 out of 21). These gains were underpinned by the introduction of new, high-performance ZEV models and market shifts toward more efficient, faster-charging, and longer-range ZEVs. For instance, GM and Honda introduced high-performance EV models in their limited EV offerings and it led to a big increase in their scores. Geely, Chang’an, and Chery, which already offered a diverse range of EV models, improved substantially with new high-performance EV lines or shifts toward premium brands.

Automakers that showed more effort in transitioning to renewable energy for manufacturing in our previous ratings received relatively higher scores on the new green steel metric in this rating. These include Mercedes-Benz, BMW, and VW. In addition, Ford and GM performed well on the green steel metric due to better public disclosure of information related to relevant aims and efforts. All five of these automakers have made some commitment to using green steel in manufacturing by 2030, by setting targets and/or securing offtake agreements.

In terms of automakers’ strategic vision for ZEVs, 2024 was mixed. Although Nissan made progress by announcing a ZEV-only target and Chang’an and Hyundai-Kia slightly raised their EV targets, Ford, Tata Motors, Dacia (Renault), Mini (BMW), and Volvo Cars (Geely) rolled back or removed their ZEV targets. None of the 21 automakers significantly increased their ZEV investments in 2024. For the first time, Honda linked its executive compensation to a carbon dioxide emissions metric. In contrast, GM removed EV development from the long-term incentives component of its executive compensation plan.

MEDIA CONTACT

Kelli Pennington, Global Communications Manager, and Zifei Yang, Program Lead, ICCT communications@theicct.org

DISCLAIMER

This ICCT report is intended for informational purposes only. Although the ICCT has endeavored to organize and present data from multiple third-party sources in an even-handed and neutral fashion, the selection, interpretation, weighting, and presentation of the metrics in this rating reflect the subjective assessments and opinions of the ICCT. Additionally, while the ICCT has only used data sources it believes to be reliable, taken steps to verify such data with automakers, and identified its sources in the interest of transparency and verification, it cannot state that the data compiled and published by others is accurate. This report should not be construed otherwise.