A Guide for the Perplexed to the Indirect Effects of Biofuels Production

Blog

Isn't that a lot of biodiesel?

EPA’s recently released proposal for 2014-2017 Renewable Fuel Standard (RFS) volumes includes a substantial amount of growth for biomass-based diesel (BBD). The proposal is for 1.7, 1.8, and 1.9 billion gallons of BBD in 2015, 2016, and 2017 respectively – so each year the mandate is 100 million gallons higher than the year before. BBD includes biodiesel from animal fat, yellow grease and canola oil, but it’s dominated by soy biodiesel, and edible soy oil is likely to supply most of the increase. That’s fairly aggressive growth already, but EPA expects actual BBD production to exceed this. The advanced biofuel (read: BBD + sugarcane ethanol) and renewable fuel (read: advanced biofuel + corn ethanol + a bit of imported palm oil biodiesel) volumes are likely higher than can be reached by the combination of the proposed BBD mandate, ethanol supplied as E10 and E85, and imports of grandfathered palm biodiesel. Something needs to fill that gap, and EPA expects the gap filler to be even more biodiesel, up to 2.1 billion gallons in 2016 to be exact. That is a lot more than the 1.6 billion gallons of BBD produced in 2014!

Can we actually achieve this level of growth in biodiesel and renewable diesel? There’s no shortage of capacity to turn vegetable oils into biodiesel – we have enough capacity to churn through at least 2.8 billion gallons of biodiesel per year. But where will the feedstock come from?

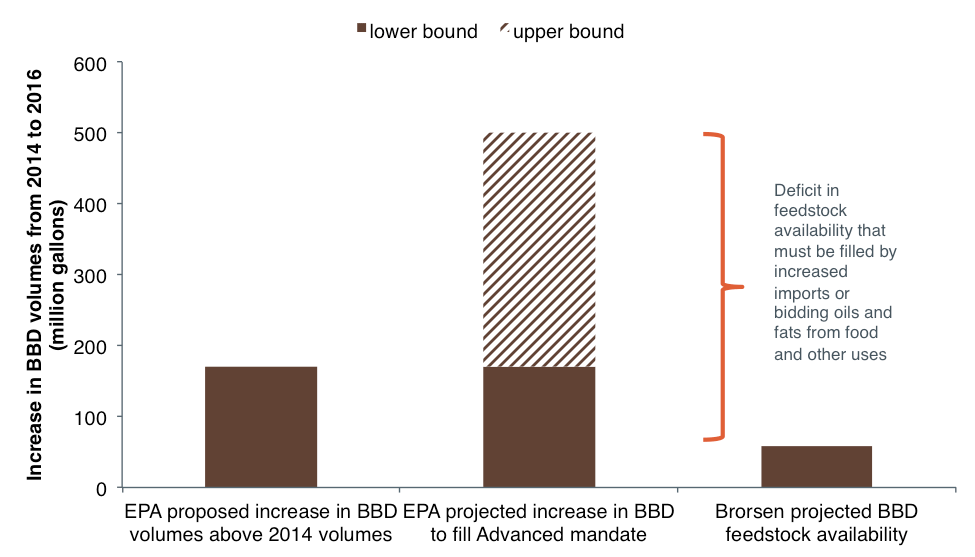

A new technical analysis by economist Wade Brorsen takes a deeper look at the supply of BBD feedstocks in the U.S. – that includes soy and canola oils, inedible corn oil from corn ethanol production, used cooking oil, animal tallow, and other recycled fats and oils. Based on past trends, USDA agricultural forecasts, and a bit of optimism about increases in waste oil collection, this study projects the rate of growth in feedstock supply that can be used to support increased BBD production without major interference in other markets. The result of this assessment is a lot lower than 2.131 billion gallons in 2016. In fact, Brorsen concludes that we will only have enough extra feedstock to produce 30 million more gallons of BBD in 2015 than we did in 2014, and this feedstock growth rate declines over time (we will have 29 million more gallons in 2016, and a 25 million gallon increase in 2017). This growth rate, that can be sustainably supported by available feedstock, is much less than the annual 100 million gallon BBD increase proposed by EPA, and far lower than the growth of up to 251 million gallons per year from 2014-2016 implicit in the ambitious advanced mandate. The figure below shows this contrast. Biodiesel already consumes roughly one-quarter of U.S. soy oil production (if we included renewable diesel it would be more), and the gap between EPA’s max scenario for BBD consumption and Brorsen’s estimate of feedstock availability would increase biodiesel usage to 40%.

Increase in BBD volumes from 2014 to 2016 in EPA’s proposed BBD volumes; EPA’s range in the quantity of BBD expected to be used in their scenarios to fill the Advanced mandate; and BBD volume increase that can be supported by feedstock growth from Brorsen (2015) (million gallons).

Why isn’t more BBD feedstock available? For the obvious reason that people are already using those fats and oils – in food, animal feed, soaps and detergents, and other industrial uses. Brorsen argues that food consumption in particular is inelastic, which basically means we’re not going to eat less. If total demand for fats and oils increases much faster than supply, this will undoubtedly drive up prices (even without a drought like we had in 2012). In a previous blog we presented an analysis by Yin Qiu that showed increases in soy oil prices drive palm oil imports in the U.S., and we know palm expansion is highly associated with massive CO2 emissions from drainage of tropical peatland. Growing the BBD mandate faster than the ability to increase the US domestic feedstock supply is therefore liable to increase food prices without delivering any carbon savings.

We have submitted comments to the EPA in which we suggest that setting the BBD, advanced and renewable mandates at a lower level would be more compatible with available feedstock supply. In the longer term, a better way to deliver greenhouse gas reductions through biofuels in the U.S. is through increased supply of cellulosic biofuels, where there is much less risk of driving deforestation and causing instability in food prices. We’ve previously argued that stronger support mechanisms are needed to grow this nascent industry.