Investigating the U.S. battery supply chain and its impact on electric vehicle costs through 2032

Press release

Lithium supply may far exceed demand from U.S. light-duty BEVs through 2032, new study finds

(Washington D.C.) February 21, 2024 — Today, the International Council on Clean Transportation (ICCT) released a study exploring the potential for the United States to secure a reliable supply of lithium to keep up with increased sales of battery electric vehicles (BEVs).

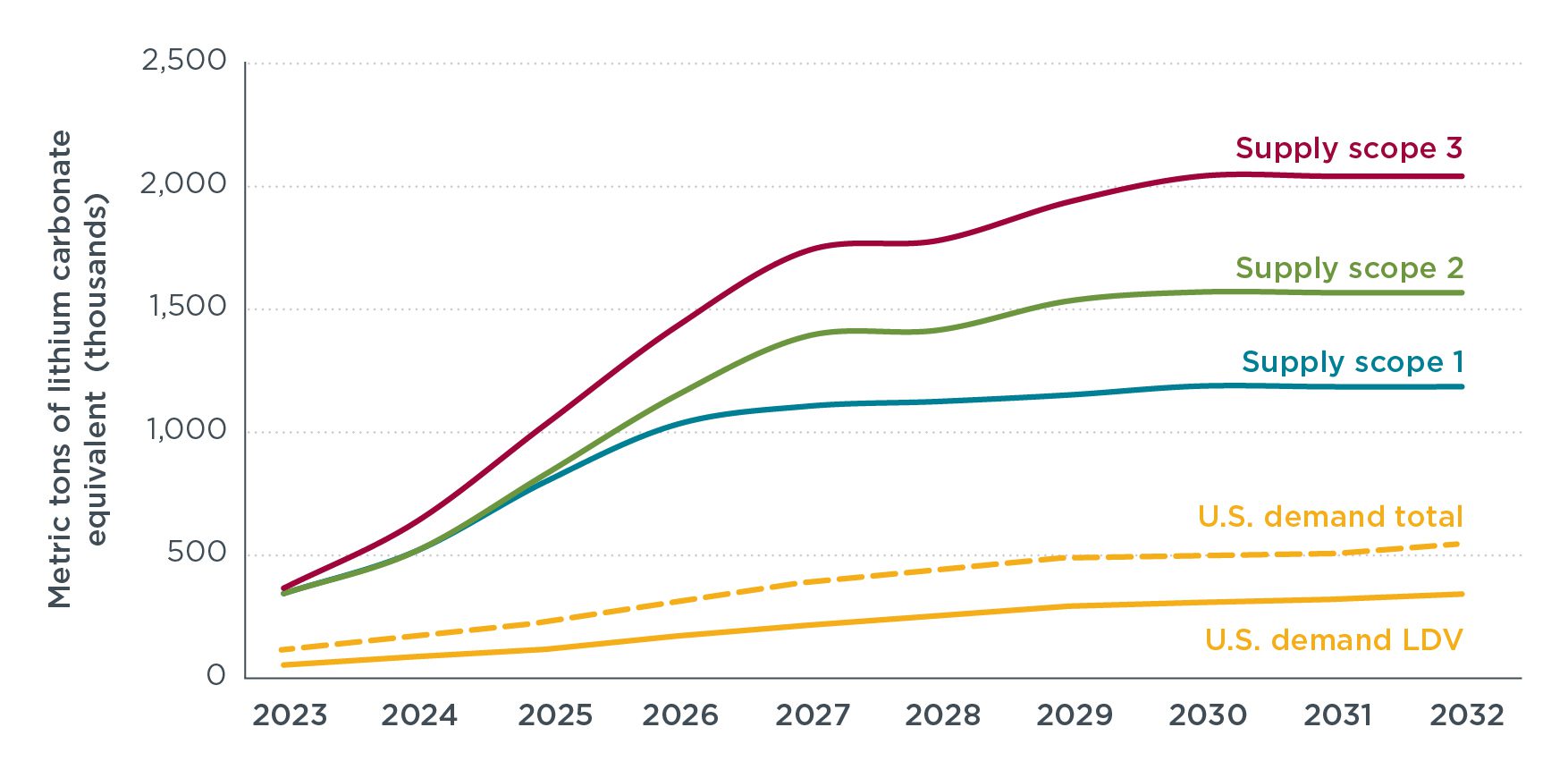

Many batteries and battery materials will be required to supply the climbing sales volumes of BEVs in the U.S., and the auto industry will need to secure a sufficient and affordable supply to manufacture and sell BEVs at prices comparable to their combustion engine counterparts. The new analysis from the ICCT underscores the U.S.’s promising position in meeting the challenges of scaling and securing lithium supply for electric vehicles over the next 10 years by comparing announced lithium supply with projected demand. The report finds that by 2032, annual lithium demand from increased U.S. light-duty BEV sales could increase to around 340 thousand metric tons per annum (ktpa) of lithium carbonate equivalent (LCE). This lithium demand is based on estimates of potential BEV market growth from EPA’s proposed Multi-Pollutant Emissions Standards such that BEVs sales shares could increase to 67% of new U.S. light-duty vehicle sales by 2032. Through identifying three potential scopes for lithium supply, the ICCT concludes that new lithium supply may far exceed lithium demand from new U.S. light-duty BEVs through 2032.

The three potential scopes of new lithium supply are based a detailed assessment of new projects within the United State and in countries with which the U.S. has existing or potential future Free Trade Agreements (FTA) or Critical Mineral Agreements (CMA).

“The transition to electric vehicles requires a lot more battery materials, so it’s important that the supply chain keeps pace with EV market growth. The good news is there’s more than 100 lithium mining and refining projects underway within the U.S. and its trade partners” said Chang Shen, Researcher at the ICCT.

The study finds that many dozens of new lithium mining and refining projects are in operation or planned in the United States and its existing and potential future Free Trade Agreements (FTA) and Critical Mineral Agreements (CMA) partners as of 2023. These projects could lead to about 1,200 to about 2,050 ktpa of lithium supply by 2032, or about 3.5 – 6 times higher than the projected lithium needed for new U.S. light-duty BEVs.

The study estimates that the United States would account for approximately 17% of this mining capacity and 27% of this refining capacity. Countries with existing FTAs and CMAs like Australia, Canada, Chile, and Peru would account for 56% in mining and 47% in refining capacity. Potential countries for future CMAs, such as Argentina, would account for 28% of mining and 21% of refining capacities considered in this analysis. The study compares potential supply with demand and finds that supply is likely to meet or exceed demand under all supply scopes.

The study also generates hypothetical price scenarios of three key battery materials (lithium, cobalt, and nickel), from 2023 to 2032, then develops a bottom-up battery cost analysis to identify the impact of charging raw material prices on battery pack-level costs and apply those battery cost estimates to assess the impact on new BEV prices through 2032. These methods yielded the following additional results:

- Battery pack and BEV costs are linked to raw material prices, but substantial continued battery and BEV cost reductions are expected under most raw material price scenarios.

- The IRA incentives in the United States for battery production and BEV purchases accelerates the timing for purchase price parity by about three years.

“Continued battery and electric vehicle cost reductions are needed for widespread consumer adoption. Our research shows a clear path to price parity, and the IRA incentives are making that happen even faster” said Pete Slowik, the ICCT’s U.S. Passenger Vehicles Lead.

Considering announced lithium supply, anticipated cost reductions of batteries, and IRA incentives, the results of the ICCT’s study highlight the promising position of the United States lithium supply to keep up with estimates of potential market growth from EPA’s proposed Multi-Pollutant Emissions Standards while achieving continued expected cost reductions and cost-competitiveness with combustion engine vehicles. This is an encouraging sign for the increased presence of BEVs and the path to a greener future.

– end –

Media Contact:

Kelli Pennington, communications@theicct.org

Publication details:

Investigating the U.S. battery supply chain and its impact on electric vehicle costs through 2032

Authors: Chang Shen, Peter Slowik, Andrew Beach

Download: [link]

About the International Council on Clean Transportation

The International Council on Clean Transportation (ICCT) is an independent research organization providing first-rate, unbiased research and technical and scientific analysis to environmental regulators. Our mission is to improve the environmental performance and energy efficiency of road, marine, and air transportation, in order to benefit public health and mitigate climate change. Founded in 2001, we are a nonprofit organization working under grants and contracts from private foundations and public institutions.

Find us at:

www.theicct.org

Twitter LinkedIn YouTube

Keep up with our research by signing up for our newsletters.