Will California rise to the Biden administration’s SAF Grand Challenge?

Briefing

Drawbacks of adopting a “similar” LCA methodology for U.S. sustainable aviation fuel (SAF)

At present, the primary policy lever to meet the United States’ ambitious targets for sustainable aviation fuel (SAF) is a tax credit in the Inflation Reduction Act (IRA). However, more than a year after the IRA was passed, the Biden administration has yet to decide on the methodology or methodologies that may be used to determine which SAFs meet the required 50% reduction in greenhouse gas (GHG) emissions over their life cycle and can thus receive financial support. The IRA states that a fuel’s GHG emissions are to be defined and certified in accordance with the life-cycle assessment (LCA) adopted by the International Civil Aviation Organization for the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) or “any similar methodology” that satisfies criteria in the Clean Air Act. This briefing highlights key differences in the way indirect emissions are treated in CORSIA and the Greenhouse Gases, Regulated Emissions, and Energy Use in Technologies (GREET) methodology that appears to be favored by some in the aviation biofuel industry.

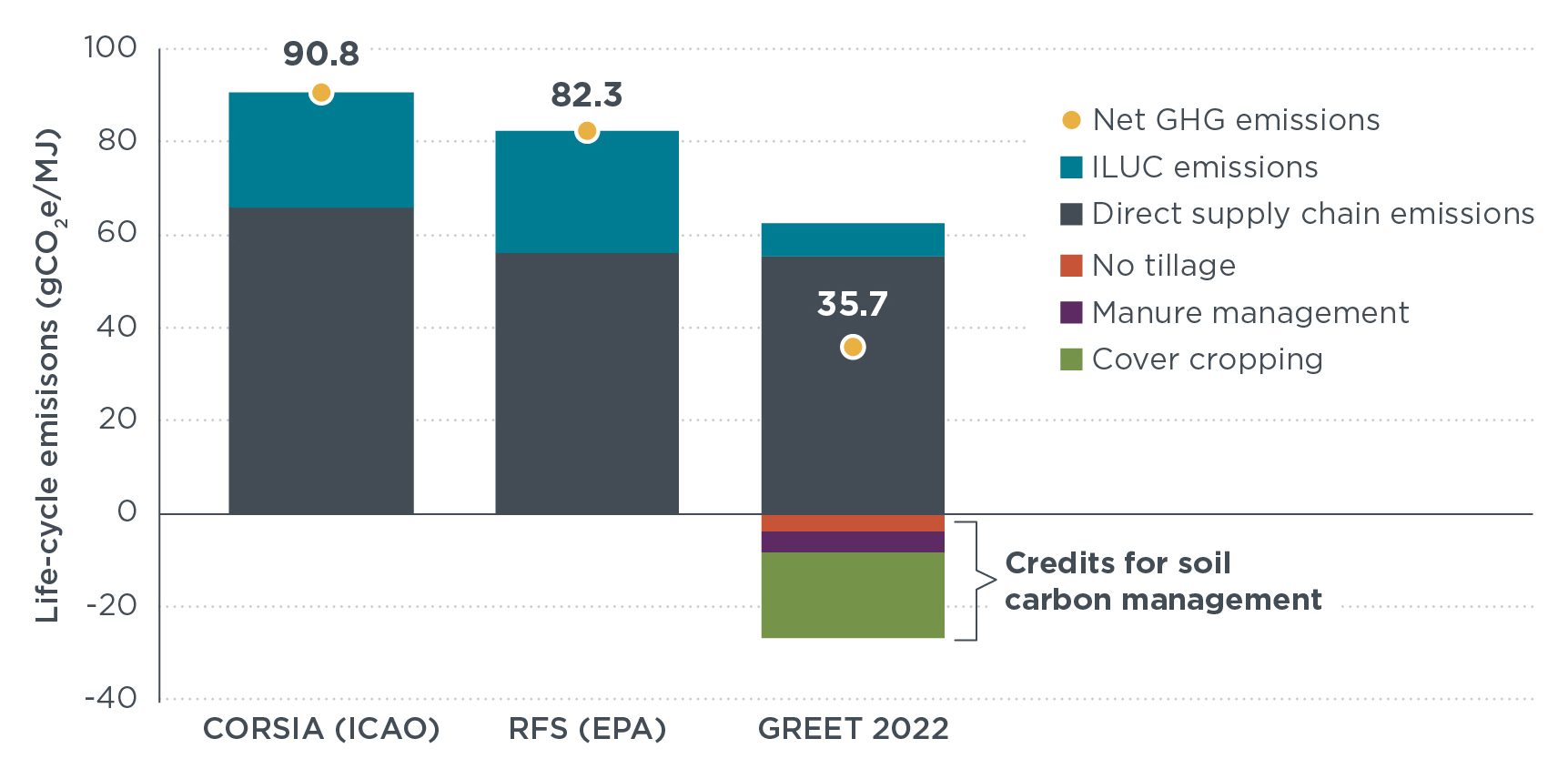

As shown in the brown bars in the figure below, the supply chain LCA emissions estimated in GREET and CORSIA are closely aligned. But emissions from indirect land-use changes (ILUC) and soil organic carbon credits from land-management practices differ widely due to assumptions in the underlying models. These indirect emissions cannot be easily verified by regulators like the Treasury Department or easily demonstrated by producers, and thus there is the risk that using GREET would widely diverge from the CORSIA approach and existing U.S. fuel policies. Adopting GREET as a “similar” LCA methodology for SAFs in the IRA could incentivize fuel pathways with uncertain GHG reduction benefits.

Figure 3. Life-cycle emissions estimates for corn ethanol-to-jet.