Blog

Sustainable aviation fuels: What does real leadership look like?

It’s a heady time for true believers in sustainable aviation fuels (SAFs)—fossil jet fuel replacements that are derived from biological or renewable electricity feedstocks. The governments of the EU, UK, United States, and California are starting to adopt clear policies to promote SAFs, but these range from inadequate to enlightened. Who’s showing true leadership on SAFs? The International Air Transport Association (IATA), which represents airlines globally, says it’s the United States, and that Europe lags. But they have it exactly backwards.

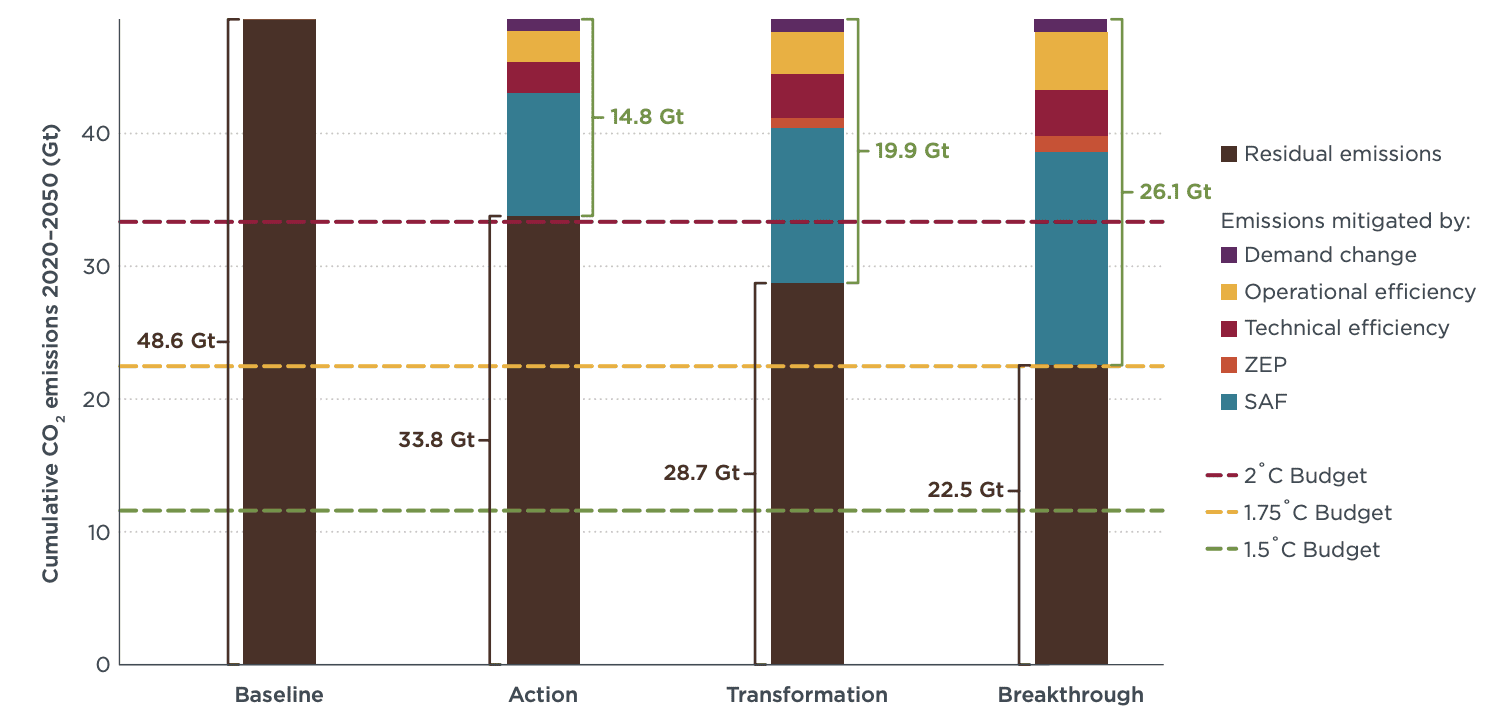

Let’s start with a point of agreement. Nearly all analysts conclude that SAFs will play a key role in any net-zero future for aviation. Like today’s conventional jet fuels, SAFs are energy-dense; each tonne packs a punch, which makes long-distance air travel possible. And as “drop-in” fuels, SAFs can be used in today’s aircraft with few modifications, making them key to mid- and long-term decarbonization, particularly of long-haul flights. That’s why ICCT’s aviation 2050 report, which examined several decarbonization scenarios, concluded that SAFs are likely to contribute the majority of future CO2 reductions in a decarbonized future for aviation (Figure 1, teal bar segments).

Figure 1. Cumulative global aviation CO2 emissions by scenario and measure, 2020-2050

Where analysts disagree is on how to scale SAFs in the near- to medium-term. To date, SAF uptake has been deeply disappointing. Airlines used just 100 million liters of alternative jet fuel in 2021 – less than one percent of IATA’s 2020 goal. This sluggish progress is the result of high costs (2 to 5 times the 2019 price of conventional jet fuel), feedstock constraints, and sustainability concerns about first-generation biofuels.

Nevertheless, the airline industry remains bullish on SAFs, despite being famously fuel-price sensitive. The core problem is that airlines won’t voluntarily pay more for fuel, and everyone knows it. And Econ 101 argues that capital won’t flow to investments that are unlikely to generate revenue. It’s a basic chicken and egg dilemma.

It’s completely understandable that airlines can’t voluntarily muster demand for SAFs. IATA’s solution: claim that the problem is one of short-term supply, rather than long-term demand. This is just silly. The nickels and dimes that airlines are throwing at SAF today are insufficient to increase supply and build true markets. Instead, they are about burnishing airlines’ images by showing that they are active in ESG (environment, social, and governance) issues. Do the math: the 125 million liters of SAFs purchased last year cost the airlines around $250 million, assuming $2 per liter. That’s about 0.1% of total jet fuel expenditures, based on 250 million tonnes of fuel consumed, at $146 per barrel.

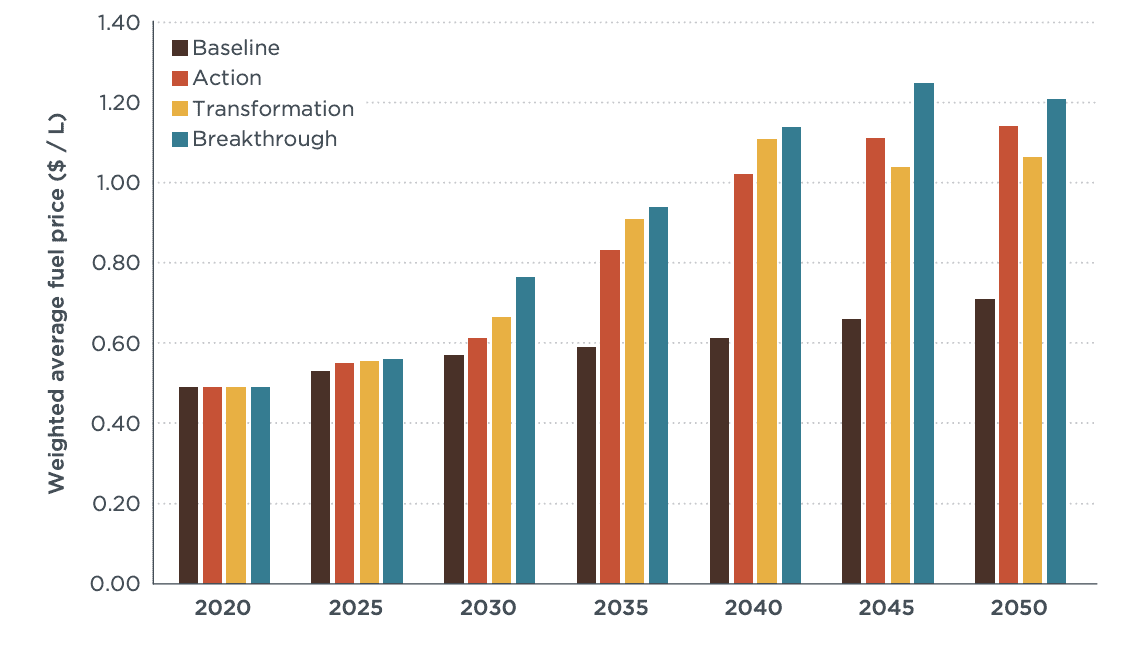

This is peanuts, and nowhere near the level of commitment required. According to our recent zero-emission aviation report, SAF blending consistent with a 1.75 degree C global temperature cap (our Breakthrough scenario) would increase fuel costs in 2030 by approximately 35% (Figure 2). How many airlines, operating in a competitive market, would voluntarily pay that premium? Zero.

Figure 2. Effects of SAFs on carbon pricing and average fuel price

In truth, scaling SAFs is largely about guaranteeing demand. This can be done in several ways, including mandating their use (as the EU is doing) or paying airlines to use them (the emerging US approach). Guess which strategy IATA prefers?

As my ICCT fuels colleagues argue, the EU is assembling a comprehensive suite of policies to accelerate SAF markets under its “Fit for 55” package (as is the UK, under its “Jet Zero” policy.) It’s a 3-legged policy stool: a SAF mandate with robust feedstock criteria, carbon pricing with revenue recycling, and fuel tax reform. At the heart of the EU’s approach is the “Polluter Pays Principle”—the idea that emitters should bear the cost of addressing their pollution. Hostility to this idea is what really motivates IATA.

By contrast, the US approach to SAFs, as illustrated in Biden’s “SAF Grand Challenge”, is an aspirational policy to produce 3 billion gallons of SAFs in the US by 2030. (This updates previous, unmet U.S. goal of introducing 1 billion gallons of SAF in 2018.) The new goal would be supported by a blender’s tax of up to $1.75/gallon under the Senate’s Inflation Reduction Act. U.S. NGOs have raised questions about the blender’s tax credit—namely that it’s a short-term incentive that will shuffle crops and other biofuel feedstocks from the road sector to aviation, with little net benefit. In contrast, EU policy is targeted squarely at promoting the best SAFs by establishing a stable long-term market for them.

So, to review. The EU is developing a comprehensive, concrete policy framework to promote the best SAFs, paid for by the polluters themselves. The US is considering short-term subsidies for airlines that may do little to unlock new supply. Which looks like leadership to you?