Briefing

Zero-emission vehicle deployment: ASEAN markets

This briefing gives an overview of the status of ZEV development in the ASEAN economies.

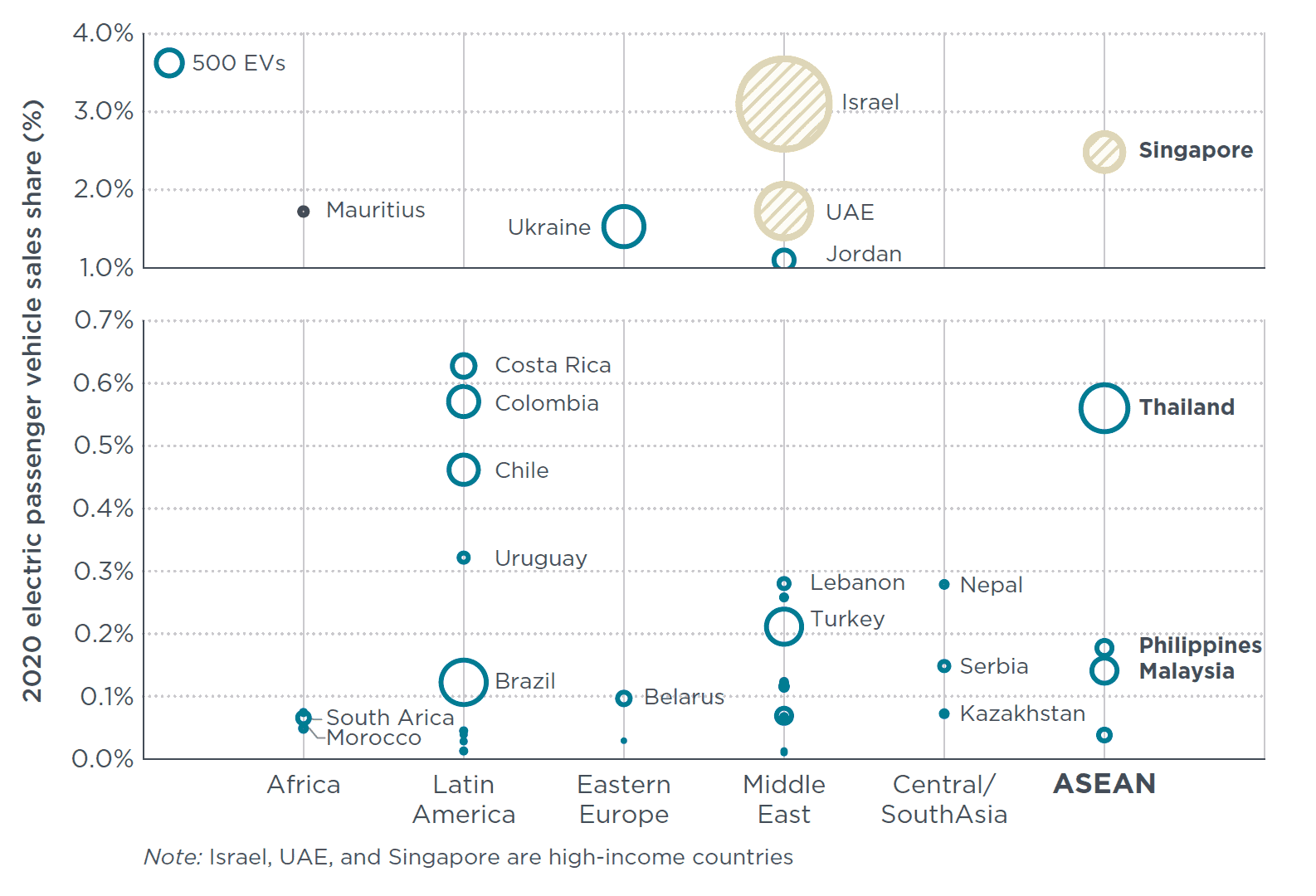

The EV share in ASEAN markets varies between 0.04% and 0.6% for passenger cars, as of 2020. (Figure.) The ZEV transition in ASEAN countries is fastest in the 2&3-wheeler segment. As of 2020, Vietnam had 262,000 electric 2-wheelers, for a sales share of 8.3%, followed by Philippines at 1.4%, Indonesia at 1.1%, and Malaysia at 0.8%. As of 2019, the Philippines had 3500 e-trikes that are used as public or private transportation.

Figure. EV sales share (%) for passenger vehicles of non-ZEV Transition Council (ZEVTC5) countries of key regions for 2020.

A few countries in the region have a small stock of electric buses. Thailand had a total of 215 electric buses as of 2020, representing 0.14% of its bus stock overall. Electric buses in Singapore, Malaysia, Philippines, and Indonesia total 2 to 35.

With regard to policies, a few ASEAN countries, including Brunei, Indonesia, Malaysia, Thailand, and Singapore have announced non-legally binding EV targets focused on sales, stock, or production; these apply to passenger vehicles, motorcycles, buses, or other segments. Some targets include provisions for hybrid vehicles and low-emitting vehicles; hence they are not exclusive to EVs.

Opportunities and success stories in the ASEAN markets are found in EV and battery manufacturing; deployment of charging infrastructure, electric 2&3 wheelers, and other low-speed EVs; implementation of purchase and usage incentives; bus electrification; and raising public awareness.

The ASEAN region also faces several challenges in accelerating the transition to ZEVs, including higher EV prices compared with low-cost ICE vehicles, lack of ZEV-related regulations that would convey a strong signal to auto manufacturers regarding adoption of ZEV technology, insufficient charging infrastructure, lack of technical expertise related to EV batteries and EV production and operation, and lack of public awareness of ZEV benefits and operation/usage in the region.

ASEAN markets would benefit from greater collaboration, including in developing a ZEV roadmap, regulations, and exclusive ZEV supply-based incentives that send clear policy signals; introducing consumer-based ZEV incentives through budget-neutral mechanisms or international financing; promoting targeted electrification of 2&3 wheelers with battery swapping or renting; improving ZEV access by incentivizing manufacturers and establishing standards and regulations; enabling innovative e-mobility business and financing models in shared mobility; demonstrating ZEV technology through exhibition, experience center, and pilot projects to raise public awareness; and establishing a robust region-wide network of charging infrastructure.