Briefing

Zero-emission vehicle deployment: Europe, Middle East, and Central & South Asia

This briefing gives an overview of the status of ZEV development in the Eurasian region.

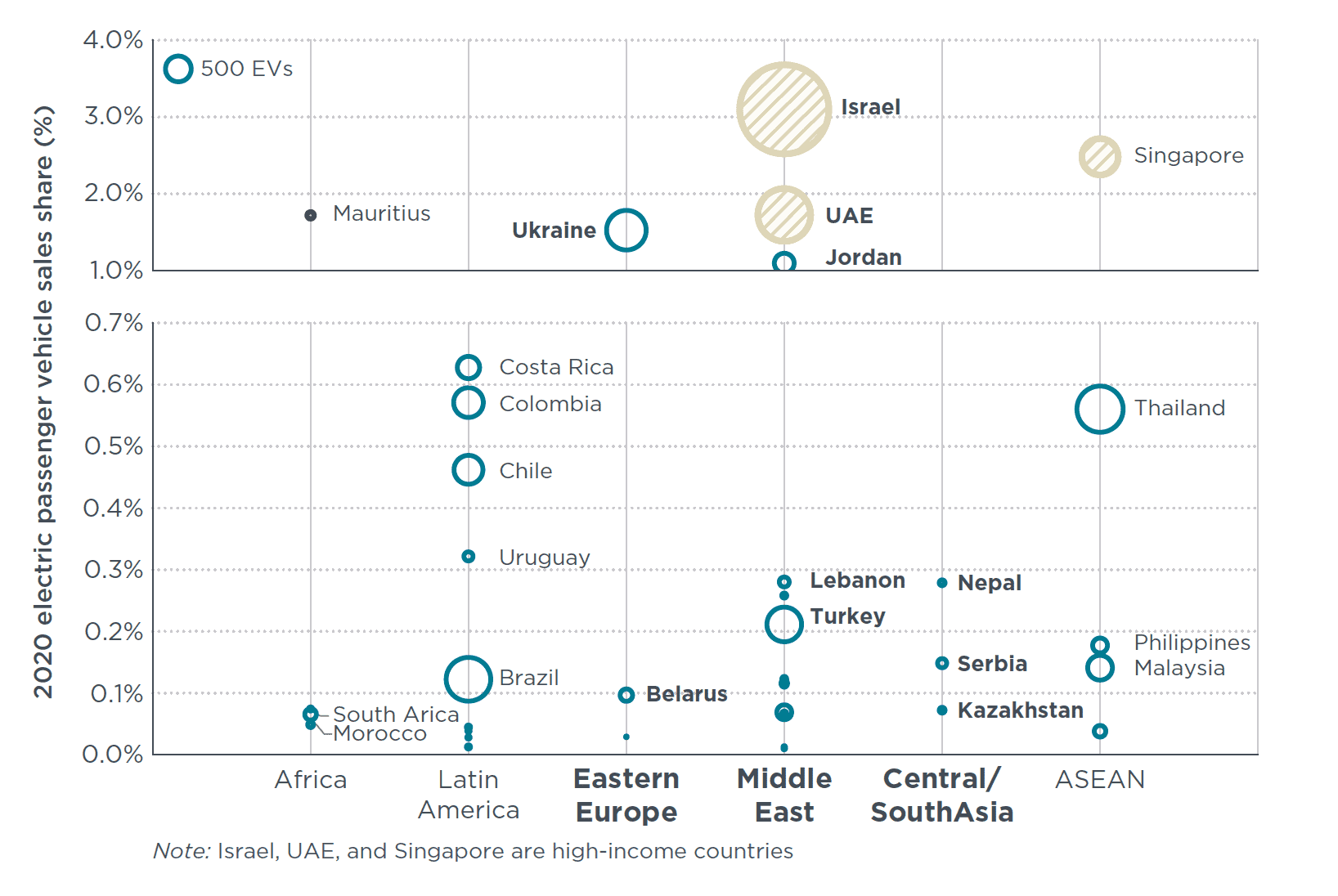

EV adoption is still at a very early stage for most countries in Eurasia, although several countries are scaling up EV sales of passenger vehicles. Ukraine and Jordan have higher EV market shares for passenger cars than other emerging economies, at 1.5% and 1.1%, respectively, as of 2020. Early signs of EV uptake are apparent in Lebanon, Nepal, Turkey, Serbia, and Belarus, with market shares between 0.1% and 0.3%.

Figure. EV sales share (%) for passenger vehicles of non-ZEV Transition Council (ZEVTC4) countries of key regions for 2020.

A few countries in the region have electric bus stock. Kazakhstan has a total of 230 electric buses as of 2020, a minor portion of their total bus stock. Nepal, Serbia, Egypt, Turkey, Ukraine, and Belarus have fleets of 5 to 61 electric buses.

With regard to EV policies, a few Eurasian countries including UAE, Qatar, Israel, Kazakhstan, Pakistan, Sri Lanka, and Nepal have announced non-legally binding EV targets focused on sales, stock, or production; these apply to passenger vehicles, motorcycles, buses, trucks, or other vehicle segments.

The region has a number of EV opportunities and success stories in the areas of manufacturing; import, distribution and assembly; purchase and usage incentives; charging infrastructure; and shared mobility. It also faces several barriers and challenges, including higher EV prices compared to low-cost ICE vehicles, lack of ZEV-related regulations, inadequate charging infrastructure, lack of e-mobility-based businesses in many countries, and lack of public awareness of ZEV benefits and use in the region.

Eurasian markets would benefit from greater collaboration across many areas, including developing ZEV roadmaps, regulations, and ZEV-exclusive supply-based incentives that send clear policy signals; reducing ZEV costs through trade agreements and international financing; integrating infrastructure development with renewable energy and innovative charging solutions; improving ZEV access by incentivizing the automobile industry and establishing standards and regulations; enabling innovative e-mobility business and financing models in shared mobility; and demonstrating ZEV technology through exhibitions, experience centers, and pilot projects to raise public awareness.