Briefing

Zero-emission vehicle deployment: Latin America

This briefing gives an overview of the status of ZEV development in Latin American economies.

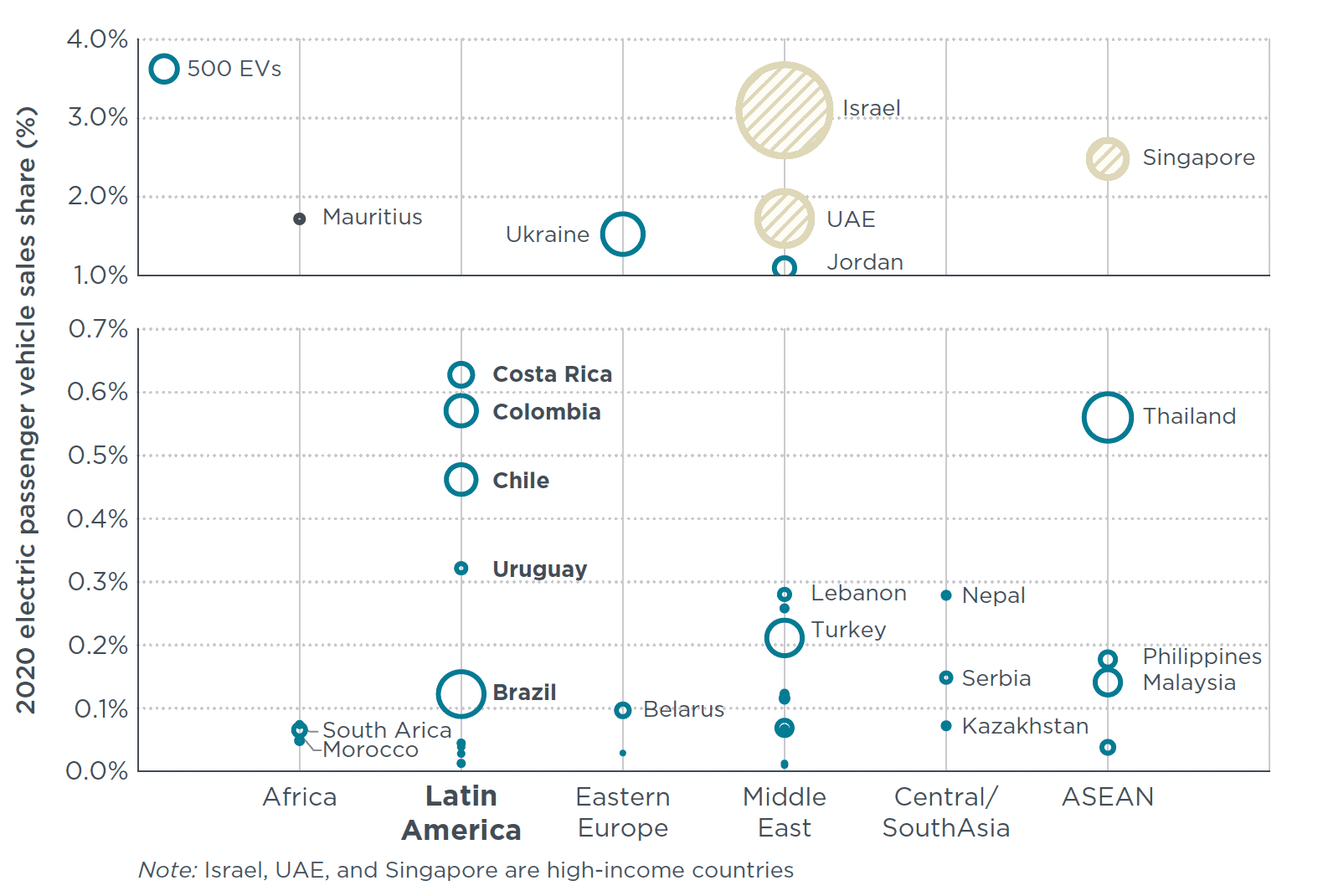

EV adoption is underway in some Latin American markets for the passenger vehicle segment (Figure). The 2020 EV sales shares for passenger vehicles are scaling up in Costa Rica and Colombia at 0.6% each, and in Chile at 0.5%. Mexico and Brazil have higher EV sales but lower market shares due to their bigger market sizes. Mexico is the only ZEVTC member country among Latin American nations but is included in the Figure for a complete review of the region. Similar to developing countries in other regions, electric passenger car uptake is still at a very early stage in the Latin America.

Figure. EV sales share (%) for passenger vehicles of non-ZEV Transition Council (ZEVTC5) countries of key regions for 2020. Mexico is a ZEVTC country but is included for a complete review of Latin America.

Regarding bus segment, Chile and Colombia are home to the largest fleets of electric buses after China. By the end of 2020, Chile’s electric bus stock stood at more than 800 and Colombia had around 500 electric buses, with more on order. Argentina, Brazil, Ecuador, Uruguay, and Mexico have also put 20–70 electric buses into operation. Costa Rica, Panama, Paraguay, and Peru have several electric buses in pilot trials. The Latin American region is the second largest two-wheeler market after Southeast Asia, but the electrification of two-wheelers is in the earliest stages.

With regard to EV policies, several countries in the Latin American region, including Chile, Colombia, Costa Rica, Ecuador, Mexico, and Panama have set non-legally binding targets for ZEV sales or stock, or for internal combustion engine (ICE) phase-out that apply to passenger vehicles, buses, trucks, or other vehicle segments.

Opportunities for electrification, and success stories, are found in the areas of electrification of bus fleets and government fleets; manufacturing & assembly; incentives; charging infrastructure; R&D; and capacity building. Top barriers and challenges are found in insufficient fiscal incentives to reduce the cost of electric passenger cars; inadequate charging infrastructure, weak regulatory policies; lack of ZEV model availability; and lack of public awareness of ZEV technologies, incentives, and charging options.

Latin American markets would benefit from greater collaboration across many areas, including improving ZEV cost-competitiveness through fiscal incentives; developing a dense nationwide network of charging infrastructure; improving EV access through manufacturing and imports; replicating successful financing and business models for scaling ZEVs in fleets; targeted electrification of two-wheelers with battery swapping or renting; launching public awareness campaigns to spark curiosity and dispel myths about regional collaboration and coordination.