Report

Review and Comparative Analysis of Fiscal Policies

Governments worldwide are increasingly looking to fiscal policy to enhance and reinforce standards-based approaches to reducing vehicle emissions. The taxes, fees, rebates, and other instruments in use or proposed vary significantly in what they measure, their stringency, timing, and other details. That makes comparison across jurisdictions challenging, though it is essential to evaluating the relative benefits of different approaches and isolating best practices.

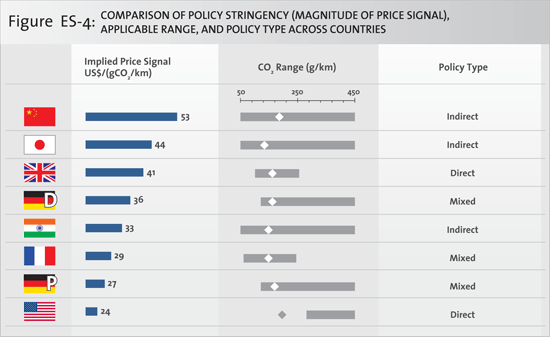

This report analyzes three types of taxes and incentives applied to new private passenger vehicles in eight of the world’s leading auto markets: (1) those that vary directly with vehicle CO2 emissions or fuel economy; (2) those that vary with a vehicle attribute related to CO2 emissions, such as engine size or vehicle weight; (3) those designed to promote alternative fuels or vehicles (e.g., ethanol, hybrids). It develops a quantitative comparison of the strength of the price signal created by each charge or incentive. To compare the price signal across such a varied set of fiscal instruments, the authors calculate equivalent marginal CO2 rates as measured by U.S. dollar assigned to each marginal gram of CO2 emitted from one kilometer of driving.

Overall, European nations tend to have higher CO2 efficiencies, as they tend to have more direct (though typically discontinuous) CO2-based fiscal measures. Japan’s policy is nearly as efficient, because the various components of its tax scheme collectively function closely to a linear CO2 tax. Policies in China and India are significantly less efficient because both policies primarily link to vehicle engine size, and U.S. policy is the least efficient because it affects only a very limited number of models in the market.

The report also proposes a set of qualitative criteria for fiscal policies aimed at encouraging the purchase and manufacture of low-CO2-emission vehicles. Most importantly, the authors argue that taxes and incentives should be directly linked to vehicle CO2 emissions. Attribute-based charges cannot provide a consistent incentive to lower CO2 emissions, because manufacturers could at least theoretically change vehicle designs to minimize or avoid penalties without actually lowering emissions. A direct CO2-based system, on the other hand, assures an incentive to reduce vehicle CO2 emissions.

As this report highlights, countries have not optimized fiscal policies to drive down CO2 emissions from passenger vehicles across the new vehicle fleet. By linking incentives to CO2 emissions rather than vehicle attribute, price signals could be made stronger and policies more robust, and converting fixed taxes and fees to CO2-based incentives would further enhance the price signal for CO2 without necessarily changing the overall tax burden significantly.

Attachments

ICCT_fiscalpoliciesES_feb2011_Ch.pdf

ICCT_fiscalpoliciesES_feb2011_Sp.pdf