Update on electric vehicle costs in the United States through 2030

Briefing

The surge of electric vehicles in United States cities

This briefing paper analyzes 2018 electric vehicle uptake in the United States and the policy factors that are driving it. The paper catalogues forty-three unique city, state, and utility electric vehicle promotion actions and their implementation across the 50 most populous U.S. metropolitan areas in 2018. The work identifies exemplary practices across various state and local policies, public and workplace charging infrastructure, consumer incentives, model availability, and the share of new vehicles that are plug-in electric.

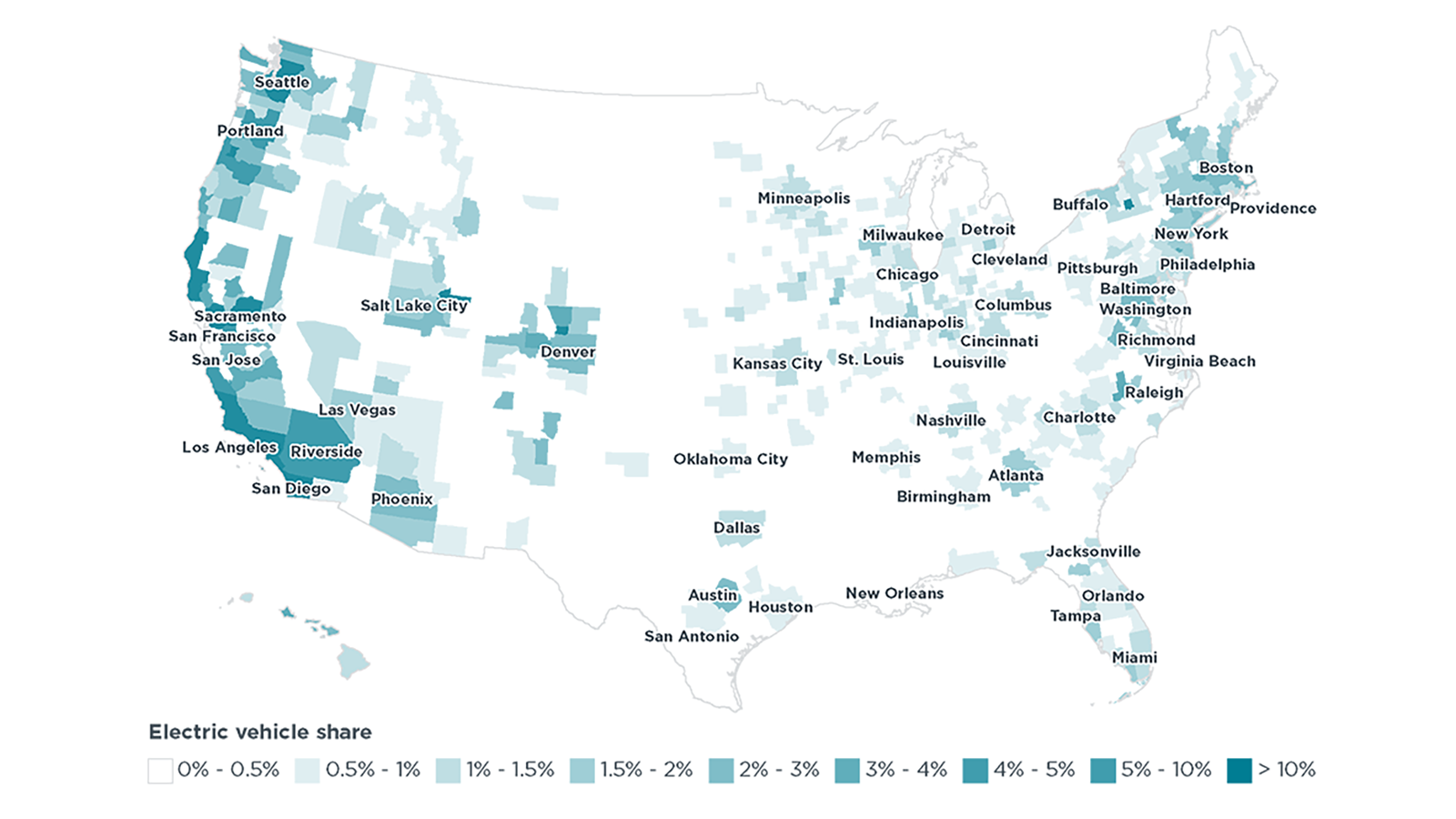

The figure illustrates the share of new vehicle registrations that are plug-in electric (both fully electric and plug-in hybrid) across U.S. metropolitan areas in 2018, with the 50 most populous areas labeled. The San Jose area had the highest electric vehicle market share at 21%, followed by other California cities, Seattle, and Portland at 4% to 13%. Overall, the share of new vehicles that are plug-in electric in these 50 areas was 2.7%, compared to 1.0% elsewhere.

Based on the analysis, the authors offer four main observations:

States, cities, and utilities continue to develop comprehensive electric vehicle policy packages. Various state and local authorities are reducing consumer purchase barriers with policy, incentives, infrastructure buildout, and awareness campaigns. States adopting California’s ZEV regulations catalyze the market, expand model availability, and provide assurance for charging infrastructure investments. In 2018 and 2019, Colorado is adopting similar ZEV regulations, and New Jersey and Washington State have signaled their commitment to electric vehicles by joining the International Zero Emission Vehicle Alliance. Markets like Atlanta, Austin, Columbus, Denver, New York, Portland, Seattle, Washington, DC, and those in California continue to construct and implement their own electric vehicle promotion policies to help reach their emission-reduction goals.

Greater diversity and availability of electric vehicle options is essential to continued growth. The top five electric vehicle markets by volume, representing over 40% of all U.S. 2018 electric vehicle sales, each had at least 33 electric vehicle models available. However, across major U.S. markets, about half of the population has access to 14 or fewer electric models. According to the analysis, expanded model availability in more vehicle segments is key to continued market development. For example, the newly-available long-range Tesla Model 3 had approximately 130,000 sales in 2018, or half of all 2018 BEVs sales and greater than all U.S. electric vehicles sales in 2015.

Consumer incentives remain important. Electric vehicle prices have greatly decreased even as their electric ranges have increased. Yet, incentives remain important to reduce electric vehicles’ upfront cost. Consumer incentives, typically worth $2,000 to $5,000, were available through 2018 in nine of the 11 major metropolitan areas with the highest uptake. The exceptions are Seattle, where the state incentive expired in May 2018, and Washington, DC, where some drivers benefit from nearby Maryland’s state incentive. Incentives like carpool lane access and preferential parking policies benefit electric vehicle drivers in Nashville, Phoenix, Raleigh, Salt Lake City, and many areas in California. As the federal $7,500 electric vehicle tax credit begins to phase out for some manufacturers, continued state, city, and utility incentives will remain important.

Electric vehicles and the charging infrastructure network grow in tandem. Even though most charging occurs at home, electric vehicle market shares are typically larger where there is greater availability of public regular, public fast, and workplace charging infrastructure. Markets with high electric vehicle uptake have at least 400 public charge points per million people. By contrast, half of the U.S. population lives in markets with charging infrastructure at least 60% below this benchmark. In the top electric vehicle markets, about 10 to 25% of the available public charging is fast charging. The top electric vehicle markets also typically have at least 150 workplace charge points per million people, and San Jose, with the highest electric vehicle share in 2018, had about 9-times this value.