Driving electrification: A global comparison of fiscal policy for electric vehicles

Report

Using vehicle taxation policy to lower transport emissions: An overview for passenger cars in Europe

Transport emissions of carbon dioxide (CO2) have not decreased nearly as much as CO2 from all other sectors in Europe. Together with emission limits, taxes can help accelerate reductions by giving consumers incentives for buying low-emission vehicles, creating a market-pull effect. Our report provides an overview of vehicle taxation policy across Europe to inform how governments might induce consumers to opt for low-emission vehicles and reduce CO2 emissions of national vehicle fleets.

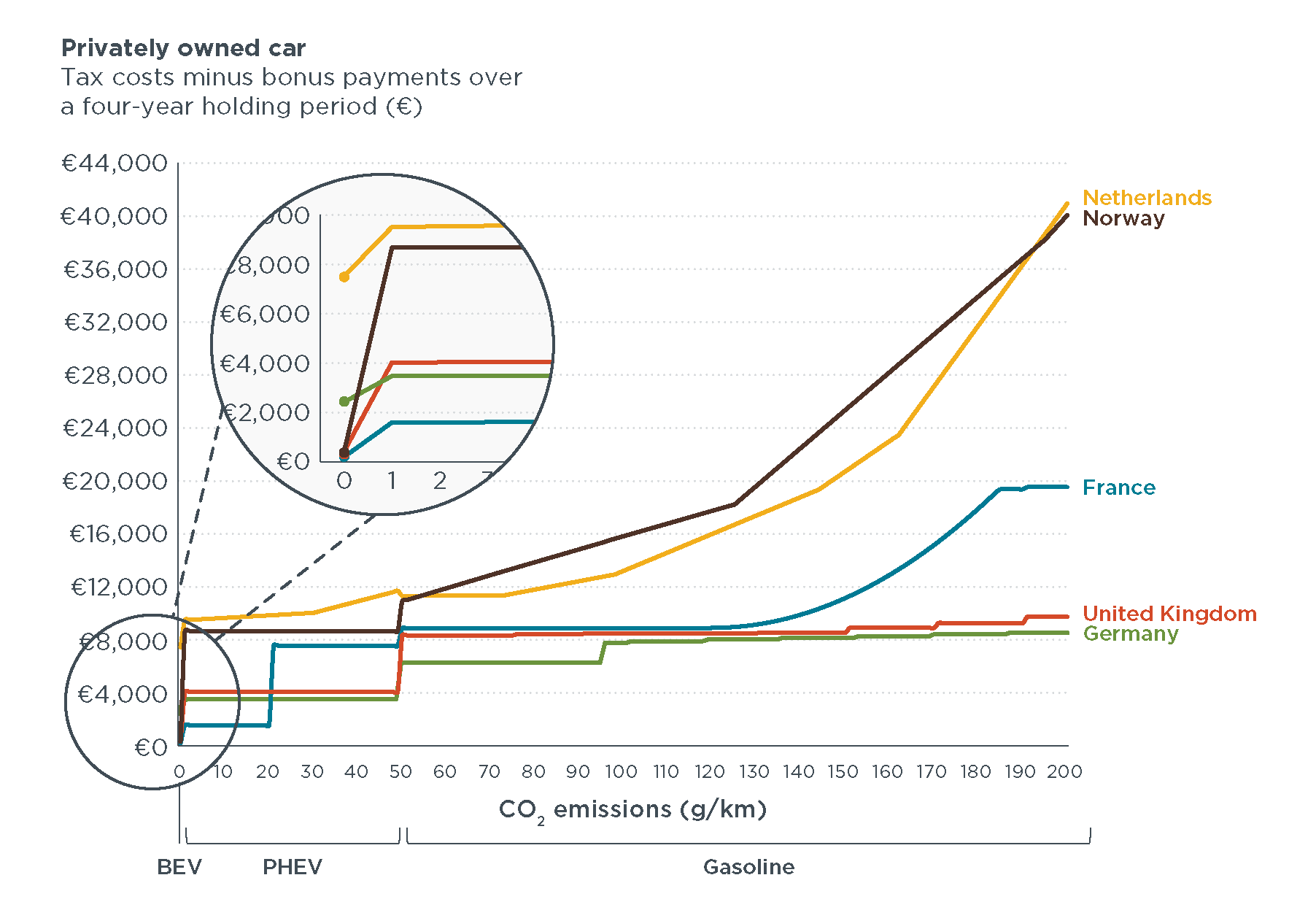

Markets such as Germany and the United Kingdom offer consumers comparatively fewer tax benefits for low- compared with high-emission vehicles in the 0–200 grams (g) CO2 per kilometer (km) emission range assessed for this report. The tax payment curve is relatively balanced in these two markets, with minimal cost increases for owners of cars emitting more than 50 g CO2/km in the case of the United Kingdom or more than 95 g CO2/km for Germany. The arc of the tax payment curve is more dynamic in France. It starts as a step-wise function, similar to the curves in Germany and the United Kingdom, but it then exponentially increases if a car emits more than 119 g CO2/km, with tax payments capped at 191 g CO2/km. The Netherlands and Norway show the greatest variations in tax-payment curves. In the Netherlands, the four-year tax payment is piecewise linear in the 1-49 g CO2/km range and also above 50 g CO2/km. Between 50 g CO2/km and 78 g CO2/km, taxes for a gasoline car are lower than for a plug-in hybrid electric vehicle (PHEV) emitting 49 g CO2/km. In Norway, the tax payment curve also is a step-wise function up to 50 g CO2/km. Between 70 g CO2/km and 200 g CO2/km it is piecewise-linear, with the most significant slope change at 126 CO2/km. The four-year tax advantage of a zero-emission vehicle over a car emitting 200 g CO2/km is the lowest in Germany at about €6,000 and the highest in Norway at almost €40,000.

Based on our findings, the following recommendations may encourage the purchase of low-emission passenger cars via taxation policy:

- Create significant tax advantages for low-emission vehicles at the point of purchase. Tax payments or tax advantages at the point of purchase have a stronger influence on consumer choice than annual tax payments.

- Ensure continued tax benefits for low-emission vehicles during their use. Lower taxes and lower total costs for consuming electricity compared with higher taxes and total price at the pump for gasoline and diesel fuel can serve as an incentive for consumers to opt for a car with an electric drive train.

- Account for the emissions of a vehicle as part of the company-car tax system. Company cars play an important role in Europe as they make up the highest proportion of new-car registrations in markets such as France, Germany, and the United Kingdom.

- Balance and regularly re-adjust the tax system to be self-sustaining. To ensure a self-sustaining tax system, vehicle-related taxes need to take into consideration all vehicles, ensure that high-emission vehicles generate the tax revenue to provide tax breaks for low-emission vehicles, and be adapted annually or every two years to account for changes in market structure.

Vehicle specifications for the battery electric vehicle (BEV), plug-in hybrid electric vehicle (PHEV)

and gasoline bands are based on comparable VW Golf models. Applicable for the tax year 2018

(starting April 2018).