Using vehicle taxation policy to lower transport emissions: An overview for passenger cars in Europe

Blog

France and Germany: A neck-and-neck race on electric vehicle sales

When it comes to soccer, France and Germany have cultivated a friendly but long standing rivalry. Despite Germany winning more world championships than France, at national matches between both teams France is leading with 14 victories verus Germany’s ten.

A similar race to the top is developing between the two countries when it comes to electric vehicles. Between 2011 and 2018, France recorded slightly higher sales shares of electric passenger cars compared to Germany. But now, according to data for the first ten months of 2019, Germany is a step ahead, with 2.9% of new passenger cars registered being electric compared to 2.7% in France.

Both the French and German teams (aka governments) are employing various tactics to take the lead in electric vehicle sales shares. An upcoming blog post will give an overview of Germany’s current incentive policies intended to spur the electric vehicle market. But what about France?

One key policy of the French government to drive electrification is the bonus-malus vehicle taxation scheme introduced in 2008. It has proven to be one the primary policy instruments in the French transport sector to promote the acquisition of low carbon dioxide (CO2) emission vehicles, such as electric cars, by charging the owners of high CO2 emitting models.

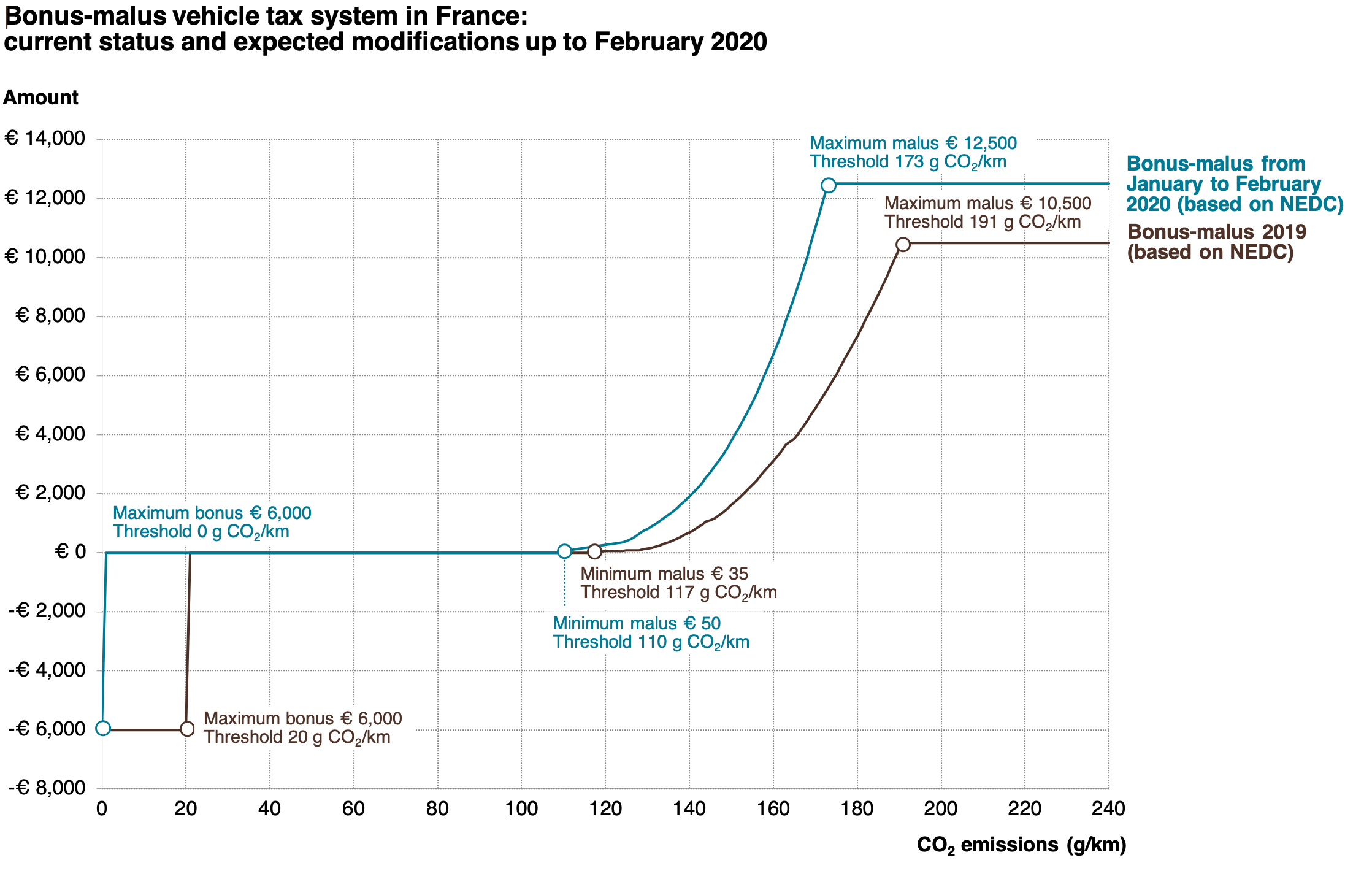

Since its introduction, the bonus-malus system has been adjusted regularly—about every one to two years—to match market developments and balance revenue streams. In 2020, French consumers buying a new car will face two more decisive changes. In January, the CO2 thresholds to determine the bonus-malus tax will be tightened. As a consequence, purchasers of a high emitting vehicle will need to pay significantly higher taxes. Then, in March, the thresholds will be adjusted a second time to more accurately reflect the CO2 emissions of a vehicle, following the new Worldwide harmonized Light vehicles Test Procedure (WLTP).

The first change will involve a shift of the minimum malus threshold, the CO2 level above which vehicle owners have to pay a tax, from 117 to 110 g CO2 per kilometer (km), as shown in the figure below. The maximum threshold that limits the maximum tax a vehicle owner gets charged will also be tightened, by 18 g/km, to 173 g CO2/km. At the same time, the minimum malus to be added to the vehicle’s purchase price will increase from €35 to €50, and the maximum malus will rise from €10,500 to €12,500. The bonus payment will be restricted to only battery and fuel cell cars. Currently, all vehicles below 20 g CO2/km, qualify for a bonus. The maximum bonus will remain unchanged at €6,000.

As a result of the planned changes, purchasers of a high-emitting vehicle will need to pay a significantly higher tax when purchasing a new car from January 2020 onwards. For example, the buyer of a Volkswagen Touareg 3.0 Liter TDI (170 kW, automatic transmission) with a CO2 value of 173 g/km will have to pay an almost € 7,000 higher tax in 2020 compared to 2019.

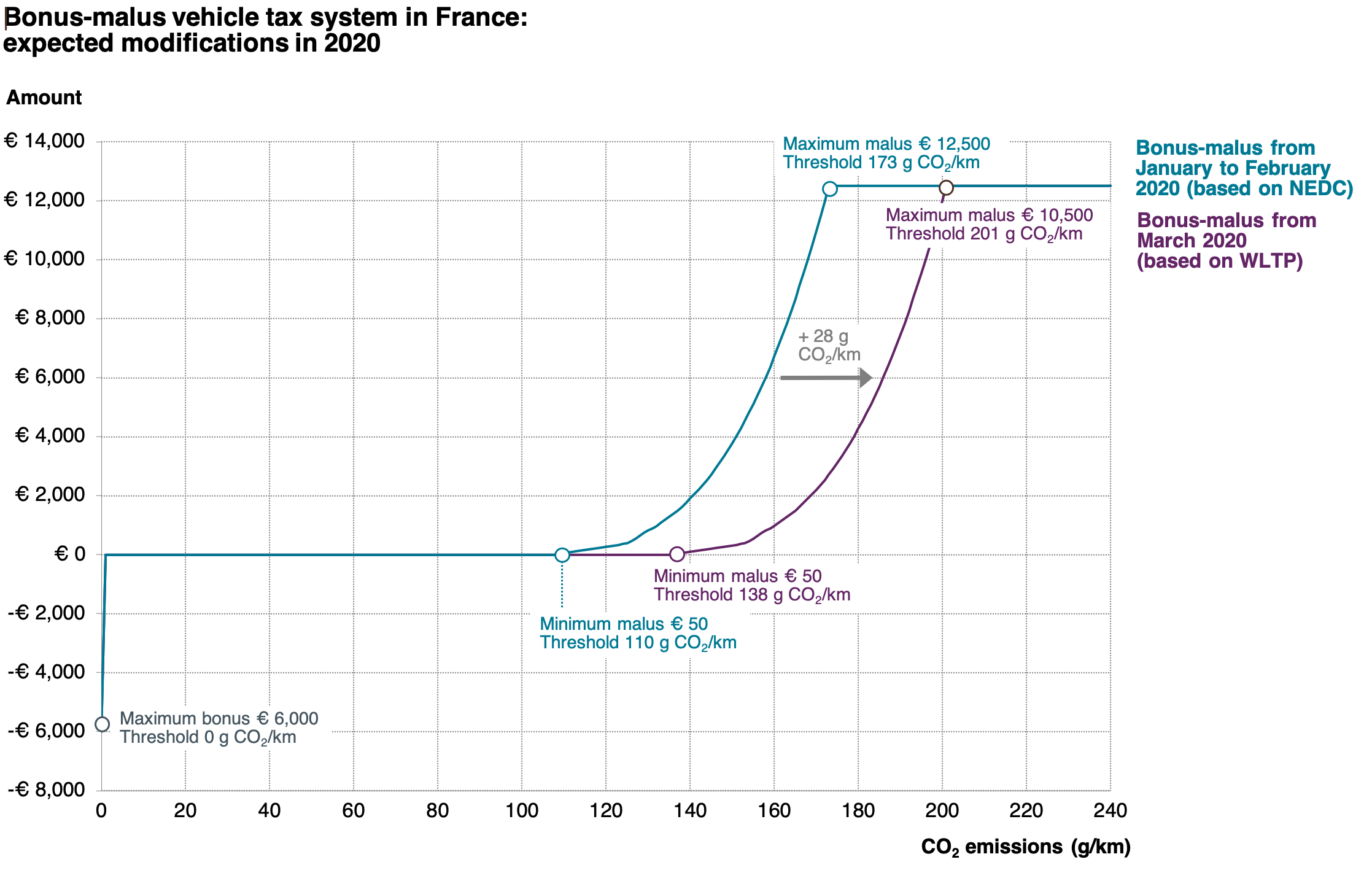

From March 2020 onwards, the second modification to the French vehicle taxation scheme will take into account the increase in CO2 emissions due to the switch from the former New European Driving Cycle (NEDC) based test procedure to the WLTP. The WLTP became mandatory for new vehicles from September 2018 onwards but so far was not reflected in the French vehicle tax system. France will now shift the malus curve upwards towards higher CO2 emissions, as shown in the figure below, assuming a constant offset of 28 g CO2/km. In practice, this means the French government allows a vehicle to emit 28 g CO2/km more during the WLTP than the NEDC while keeping the malus payment the same.

Given that there is currently only limited data available to judge if the NEDC-WLTP ratio is adequate, defining the right CO2 threshold is a challenging task. Therefore, other EU member states such as Germany have decided not to adjust their vehicle tax systems to reflect the change from NEDC to WLTP for the time being, but rather will wait to derive a suitable factor once a stronger dataset becomes available.

The 28 g CO2/km offset defined by the French government could be considered a careful, rather vehicle manufacturer friendly, approach. Early analyses of reported WLTP and NEDC emissions by JRC and TNO suggest a slightly lower offset value of 27 g CO2/km and 25 g CO2/km, respectively. An upcoming ICCT comparison of the manufacturer-reported WLTP CO2 emissions to the values measured for selected vehicles indicates the real effect of WLTP on the CO2 emissions measurement could be even lower than that.

The impact of the NEDC-WLTP ratio selected for adjusting the vehicle taxation system should not be underestimated. As an example, the purchaser of a vehicle emitting 140 g CO2/km according to NEDC would be subject to a malus of about €1,900 from January 2020. The French government assumes that the same vehicle would emit 168 g/km according to the WLTP, therefore charging the same malus payment of €1,900. However, with the NEDC-WLTP offset in reality being only 3 g/km lower—25 g/km instead of 28 g/km—the malus would only be €1,500. As consequence, there is a risk of overestimating the impact of the WLTP and thereby reducing the steering effect for incentivizing consumers to opt for low emission vehicles.

Given the uncertainty around a fair NEDC-WLTP ratio, France’s move to adjust its vehicle taxation system therefore seems brave or even dangerous, depending on perspective. A safer option might be to maintain the NEDC CO2 tax threshold until the next revision of the French bonus-malus system, most likely to take effect in 2021. By then we will have more clarity on accuracy of the NEDC-WLTP ratio in practice.

Jeopardizing the impact of the bonus-malus taxation system could pose a risk for France’s ambition to remain a leading market for electric vehicle sales. Neighboring markets such as Germany have increased the level of incentives for electric vehicles. If it becomes less costly to buy a high-emitting vehicle in France, consumers could opt for a conventional instead of an electric car. So how will France ultimately perform in this neck-and-neck electric vehicle sales race against Germany? We will follow up on the developments in both countries soon. Stay tuned for updates in 2020.