CO2 emission standards for new passenger cars and vans in the European Union

Report

Within reach: The 2025 CO2 targets for new passenger cars in the European Union

European Union legislation mandates carbon dioxide (CO2) reduction targets for new car and van sales. This regulation, referred to as the EU CO2 emission performance standards, is designed to steer the automotive industry towards achieving 100% zero-emission vehicle sales by 2035. This briefing projects the CO2 targets for each manufacturer in 2025, based on the latest official data, and estimates the maximum share of new battery electric vehicles (BEVs) needed to comply. This maximum share assumes that manufacturers will not further reduce CO2 emissions from internal combustion engine vehicles.

The study analyzes the 10 largest manufacturers and concludes that all these manufacturers except Volvo must lower their CO2 emissions to meet the 2025 targets. This requires a maximum increase in battery electric vehicle sales, with manufacturers needing to raise their BEV share at most by an average of 12 percentage points, from 16% in 2023 to about 28% by 2025.

Besides increasing their BEV sales share, compliance flexibilities within the legislation, technological progress, and adjusted marketing strategies offer manufacturers additional options to meet the targets. The study concludes that the 2025 targets seem to be within reach.

Manufacturer CO2 targets for 2025

The report estimates manufacturer-specific CO2 targets for 2025, considering official 2023 data, adjusted CO2 emissions of plug-in hybrid vehicles (PHEVs), and the impact of zero- and low-emission vehicle incentives on CO2 target calculations. The analysis shows that:

- Volkswagen and Ford face the largest reduction effort, with required cuts of approximately 21%.

- Hyundai, Mercedes-Benz, and Toyota must also reduce CO2 emissions by more than the average of 12%.

- BMW, Kia, and Stellantis are closest to meeting their targets, with CO2 reductions needed between 9% and 11%.

2025 Manufacturer CO2 targets versus 2023 fleet performance

Note: The 2025 targets are adjusted for expected changes in plug-in hybrid CO2 emissions. Data (sorted alphabetically) is shown for the 10 largest, leaving aside Tesla, a manufacturer that solely sells BEVs.

Options to meet 2025 targets

Manufacturers may consider various approaches to achieve their CO2 reduction goals:

- Increasing BEV share

- Pooling

- More efficient combustion engine vehicles

- Increasing share of plug-in hybrid vehicles

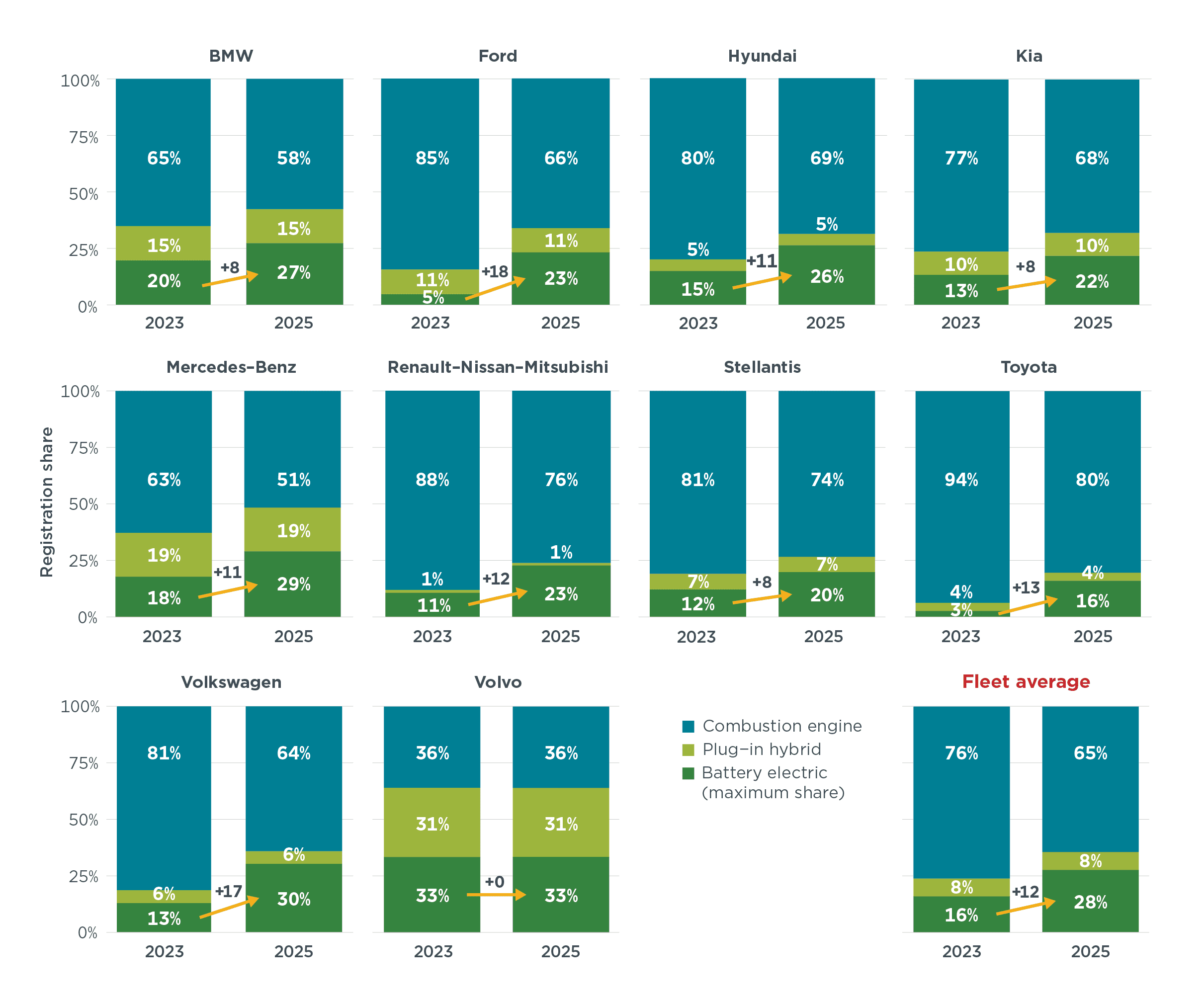

Manufacturers would need to increase their BEV shares at most by 12 percentage points on average, from about 16% in 2023 to approximately 28% in 2025. This estimation considers the maximum increase needed and assumes that there are no further reductions of internal combustion engine vehicles CO2 emissions. These increases would range from 8 to 18 percentage points depending on the individual manufacturer, but as mentioned below, strategic pooling can reduce the required BEV share increase to 4–12 percentage points.

Maximum BEV share required by manufacturers in 2025 to meet their CO2 targets  Powertrain type shares in 2023 and estimated maximum required battery electric vehicle shares to meet the 2025 CO2 targets for the 10 largest manufacturers in terms of 2023 registrations

Powertrain type shares in 2023 and estimated maximum required battery electric vehicle shares to meet the 2025 CO2 targets for the 10 largest manufacturers in terms of 2023 registrations

Note: Tesla is not included. Manufacturers are assumed to adjust their BEV shares to meet the targets.

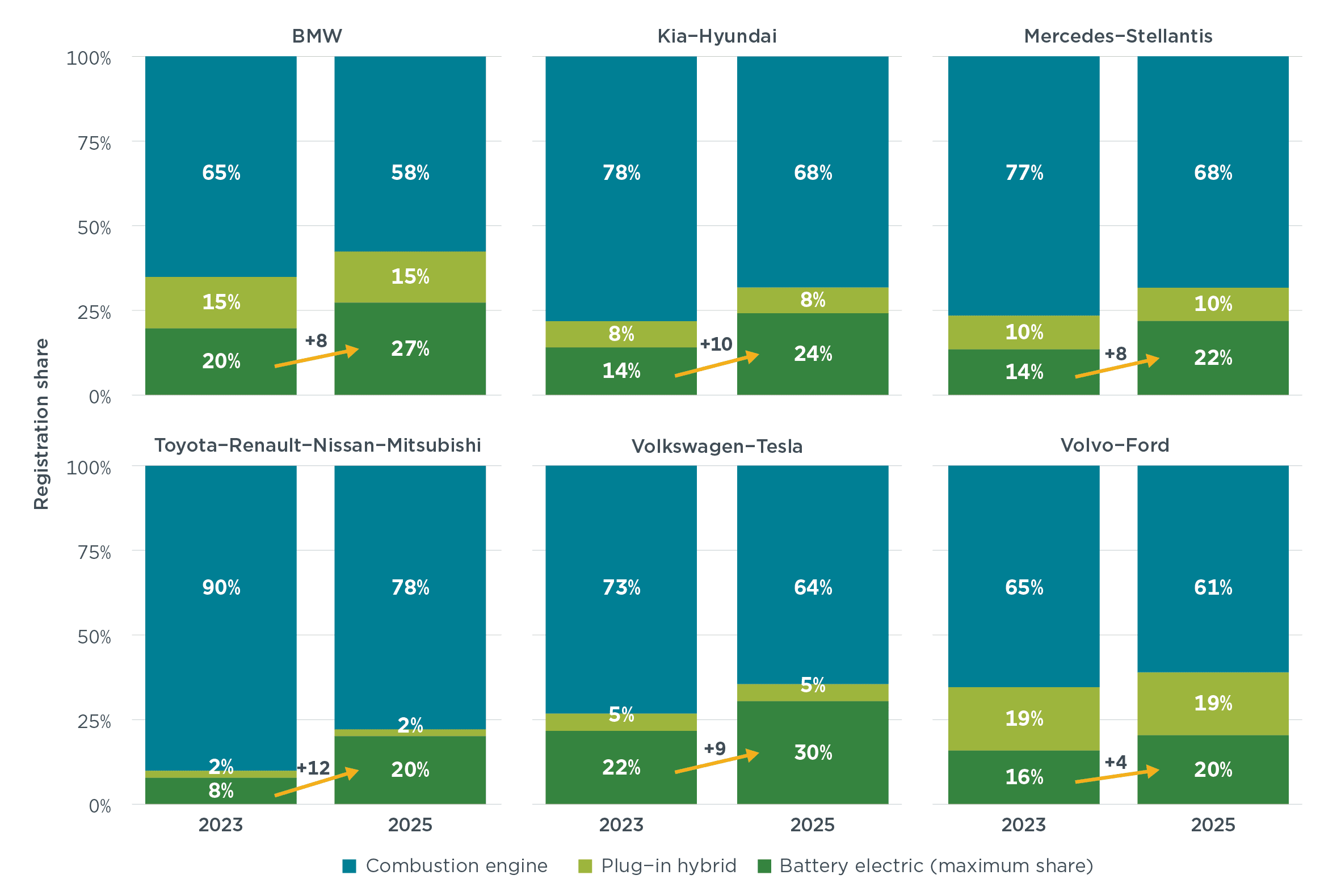

Manufacturers with higher emissions can pool with lower-emitting manufacturers. For example, Volkswagen would need to increase the BEV share by a maximum of 8 percentage points when pooling with Tesla instead of 17 percentage points.

Six hypothetical pools by powertrain type shares in 2023 versus maximum required battery electric shares to meet 2025 CO2 targets  Note: Data is shown for 6 hypothetical pools (sorted alphabetically) of the 10 largest manufacturers that produced combustion engine and battery electric vehicles in 2023 plus Tesla. It assumes that manufacturers only adjust their BEV shares to meet targets.

Note: Data is shown for 6 hypothetical pools (sorted alphabetically) of the 10 largest manufacturers that produced combustion engine and battery electric vehicles in 2023 plus Tesla. It assumes that manufacturers only adjust their BEV shares to meet targets.

Within their existing model portfolio, manufacturers can adjust their sales strategy away from heavy and high-CO2-emitting vehicles towards more efficient models. Furthermore, manufacturers can effectively reduce the CO2 emissions of individual models by deploying mild-hybrid technology.

While detrimental for the climate due to their much higher real-world CO2 emissions, increasing the market share of specific plug-in hybrid models would substantially reduce manufacturers fleet-average CO2 emissions.

Meeting the CO2 targets seems within reach

The study concludes that achieving the 2025 CO2 targets is within reach considering historical CO2 reductions, regulatory flexibilities, and powertrain types and technology availability:

- The CO2 reductions needed is about half of previous reductions achieved by manufacturers. The average CO2 reduction of 12% required from 2023–2025 is about half the 23% fleet-average CO2 reduction observed between 2019 and 2021.

- The increase in BEV market share required for the hypothetical manufacturer pools is about 1–1.5 times as high as the growth observed from 2019 to 2021. This ramp up of BEV sales from 2019 to 2021 occurred despite limited BEV model variety and fewer charging stations at the time.

- Reductions of CO2 remissions could accelerate rapidly. The historical trajectory of manufacturers CO2 emissions performance shows sudden and rapid changes. While emissions rose by 1% annually from 2015 to 2019, they fell by 1% monthly from 2019 to 2021, when a stricter target was introduced.

Fleet-average CO2 performance compared to CO2 targets, 2012–2025