CO2 emissions from new passenger cars in Europe: Car manufacturers’ performance in 2022

Research Brief

CO2 emissions from new passenger cars in Europe: Car manufacturers’ performance in 2023

This briefing analyzes the carbon dioxide (CO2) emission levels of new passenger cars in the European Union (EU) for 2023, based on preliminary data from the European Environment Agency.

The study finds that all manufacturers met the EU CO2 emission targets. The average emissions fell 1 g/km compared to 2022, marking a decrease of 1.5%. In total, 10.7 million new cars sold in 2023 had average CO2 emissions of 107 g/km, as measured by the Worldwide Harmonized Light Vehicles Test Procedure (WLTP).

The briefing details manufacturer performance in terms of CO2 emissions reduction, fuel type and technology trends, and market share. It also examines country-specific differences and compliance strategies.

Historical CO2 emission values for new passenger cars relative to EU targets

Figure 1 plots the historical average CO2 emission values relative to the targets. The graph shows the reported CO2 values measured using the New European Driving Cycle (NEDC) up to and including 2020. Since 2020, the values are based on the new testing procedure WLTP.

Figure 1. Historical average NEDC and WLTP CO2 emission values and targets for new passenger cars without flexible compliance mechanisms

Note:The 2021–2024 line corresponds to the WLTP specific emissions reference target for 2021, calculated as the average of the WLTP specific emissions reference targets of all manufacturers.

Note:The 2021–2024 line corresponds to the WLTP specific emissions reference target for 2021, calculated as the average of the WLTP specific emissions reference targets of all manufacturers.

The pace of CO2 emission reductions has varied over the years, with reduction rates generally accelerating as deadlines approach.

Between 2000 and 2007, before the first standards were agreed in 2008, fleet CO2 emissions, on average, declined by 1.9 g/km per year.

From 2008 to 2015, manufacturers exceeded the annual reduction rates required to meet the 2015 target of 130 g/km. Rather than the required 3.6 g/km annual reduction, average CO2 emissions dropped by 4.9 g/km per year. All manufacturers met their target in 2015.

From 2015 to 2019, with no stricter targets in place before 2020, average CO2 emissions increased by 0.7 g/km per year.

As the next target approached, a significant turnaround occurred from 2019 to 2020, when emissions dropped by an average of 14 g/km. All manufacturers met the 2020 target of 95 g/km using flexible compliance mechanisms.

In 2021, the transition from NEDC to WLTP took place. Removing the 2020 phase-in provisions required another significant drop in fleet-average CO2 emissions to meet the equivalent WLTP target. Since 2021, manufacturers face little pressure to further reduce CO2 emissions until the next round of targets in 2025–2029. As a result, 2022 and 2023 reductions occurred at a slower pace.

CO2 emissions by vehicle manufacturer

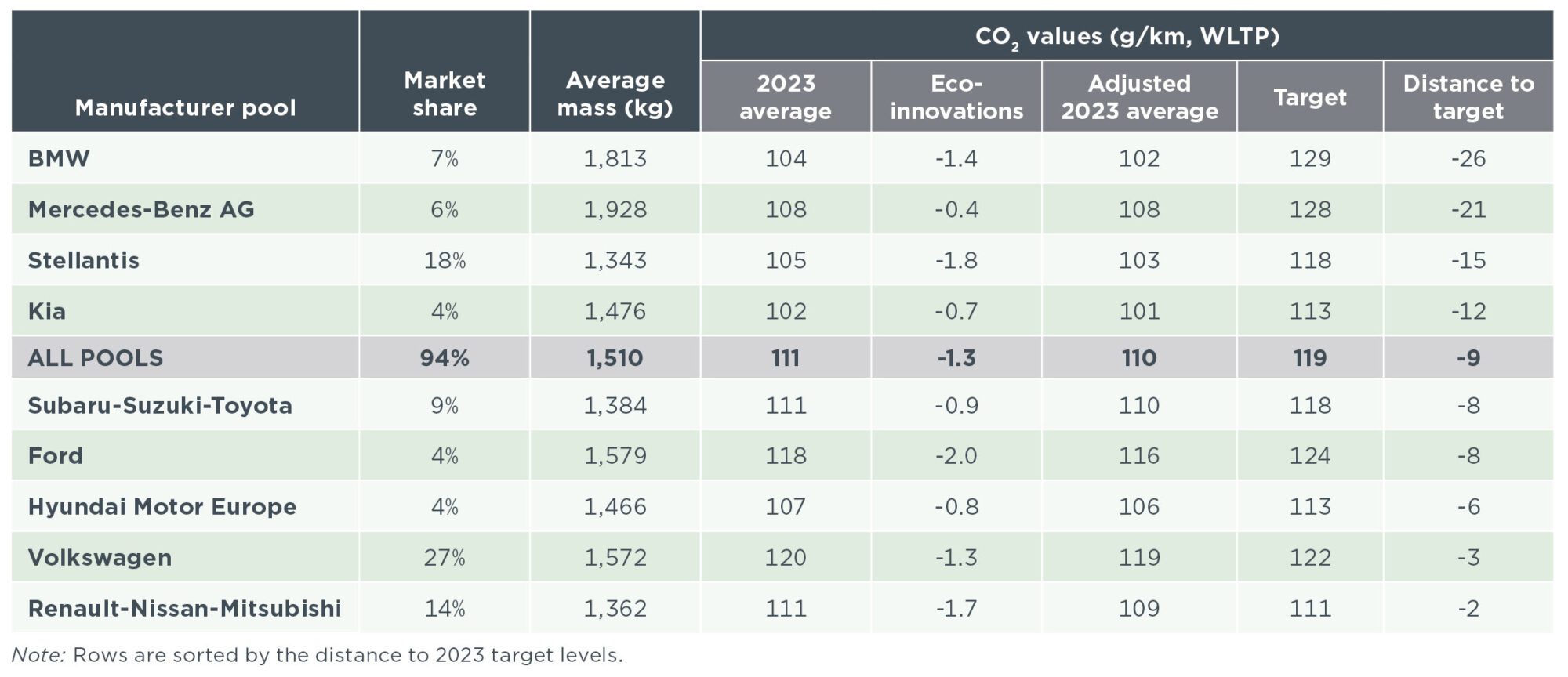

Car manufacturers can pool together several brands, not necessarily from the same manufacturer, to meet CO2 targets. Table 1 presents data for nine manufacturer pools, representing approximately 94% of all new passenger car registrations in the European Economic Area in 2023.

All manufacturer pools are expected to have met their 2023 CO2 targets, even without using the flexible compliance mechanisms. Eco-innovation technologies lowered CO2 emission levels by 0.4 to 2 g/km.

Table 1 Market share, CO2 emissions, impact of flexible compliance mechanisms, and CO2 emission targets in 2023 for the largest manufacturer pools in terms of registrations

Fuel type and technology trends by member state and manufacturer

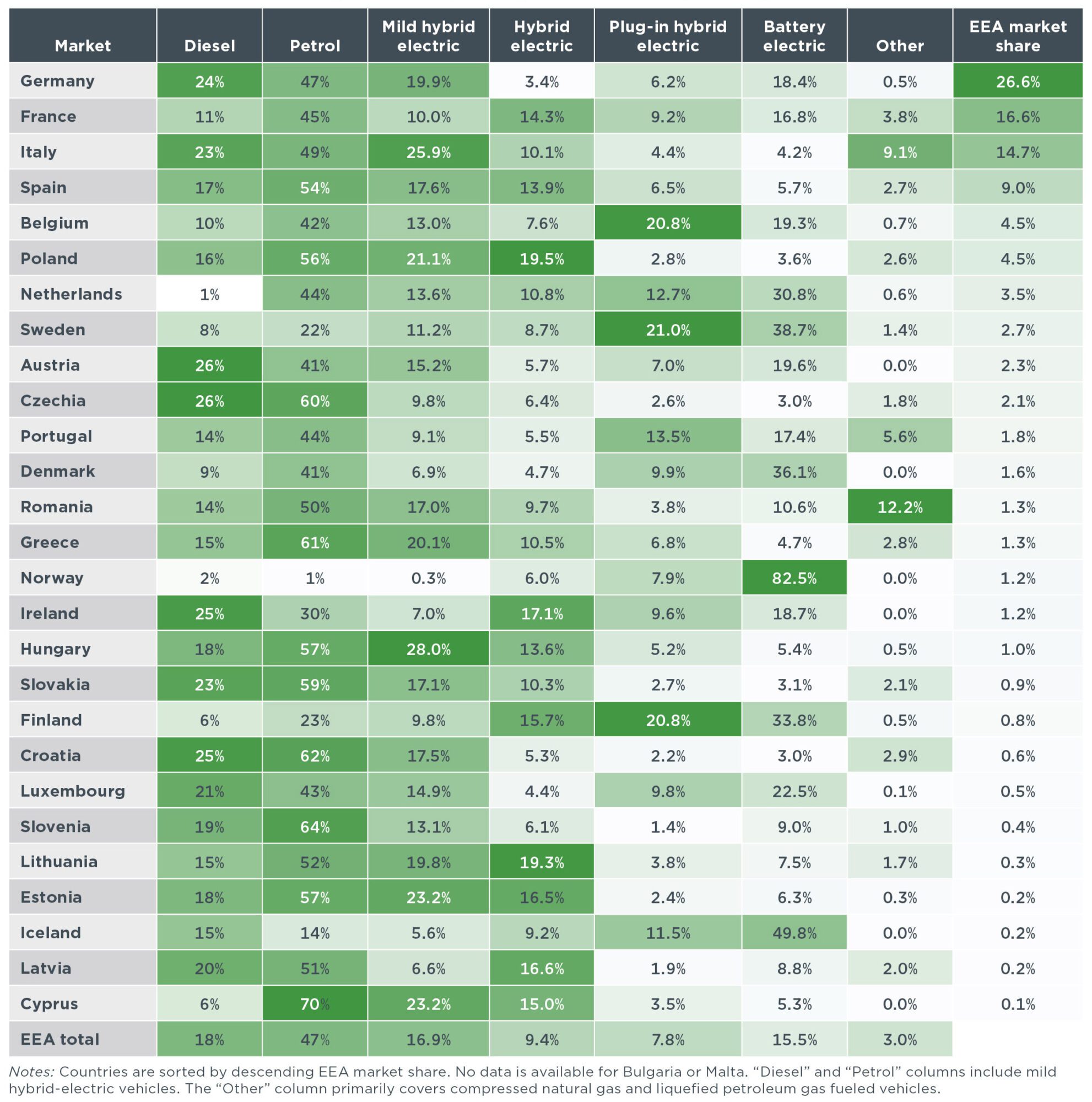

Uptake of electric vehicles increased from 2022 to 2023. The share of battery electric vehicles (BEVs) grew by 2.1 percentage points (from 13.4% to 15.5%), whereas the share of plug-in hybrid electric vehicles decreased by 1.8 percentage points (from 9.6% to 7.8%).

Table 2 presents the market share of the various fuel types and powertrain technologies by country in 2023. Norway continues to dominate the European BEV market in terms of market penetration, with more than 83% of new car registrations in 2023 being BEVs.

Table 2 Market share of fuels and technologies for new passenger cars in 2023 by country

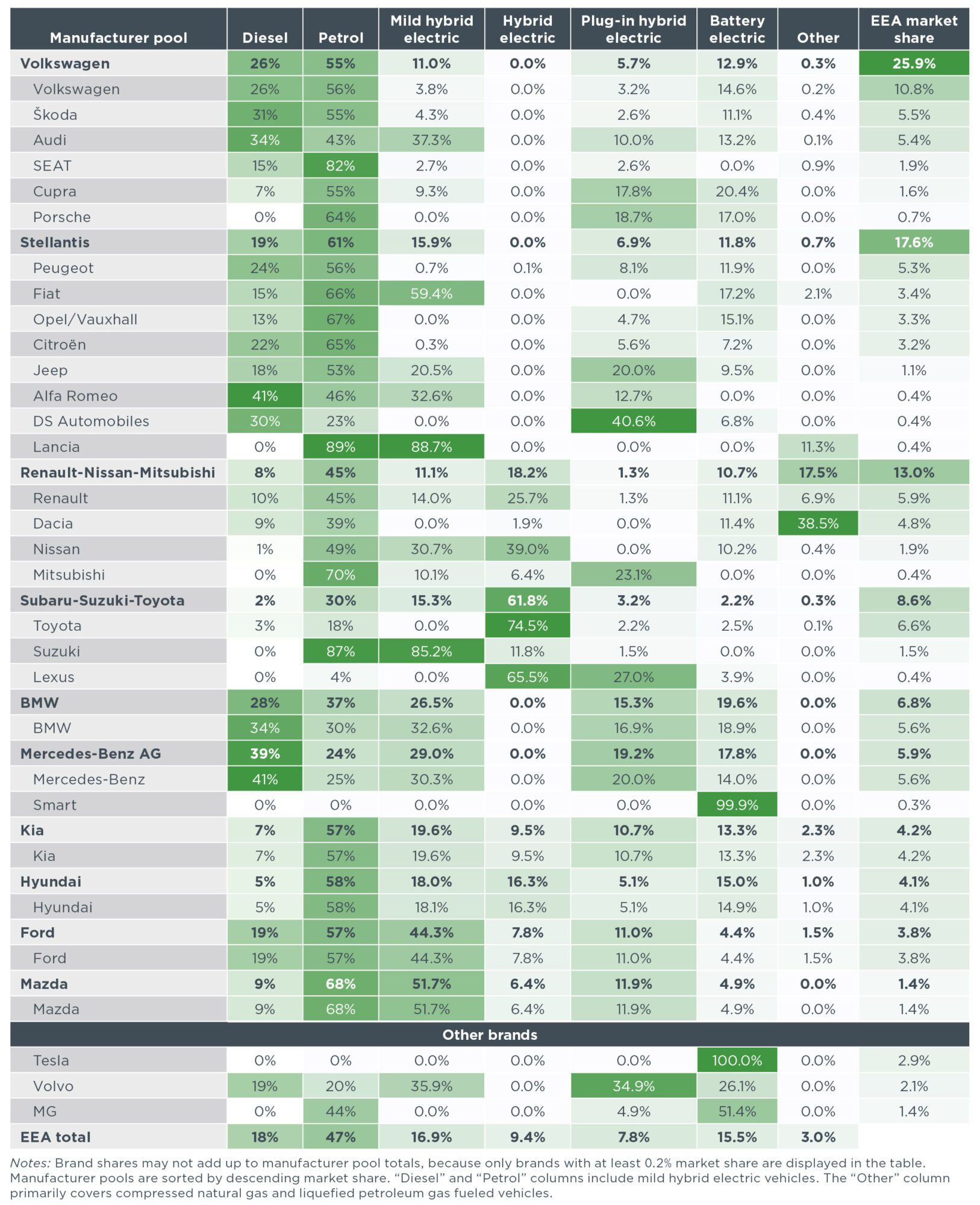

Table 3 presents the market share by fuel type and powertrain technology in 2023 for manufacturer pools and selected brands. Most pools had a BEV share above 10% in 2023, led by BMW with almost 20%. Ford, Mazda, and Subaru-Suzuki-Toyota were the only pools with BEV registration shares below 5%.

Table 3 Market share of fuels/technologies for new passenger cars in 2023 for manufacturer pools