Working Paper

Decarbonizing China’s coastal shipping: The role of fuel efficiency and low-carbon fuels

This report takes a first look at China’s domestic coastal shipping sector and provides recommendations for actionable long-term decarbonization pathways designed to avoid exceeding its current share of transportation-sector CO2.

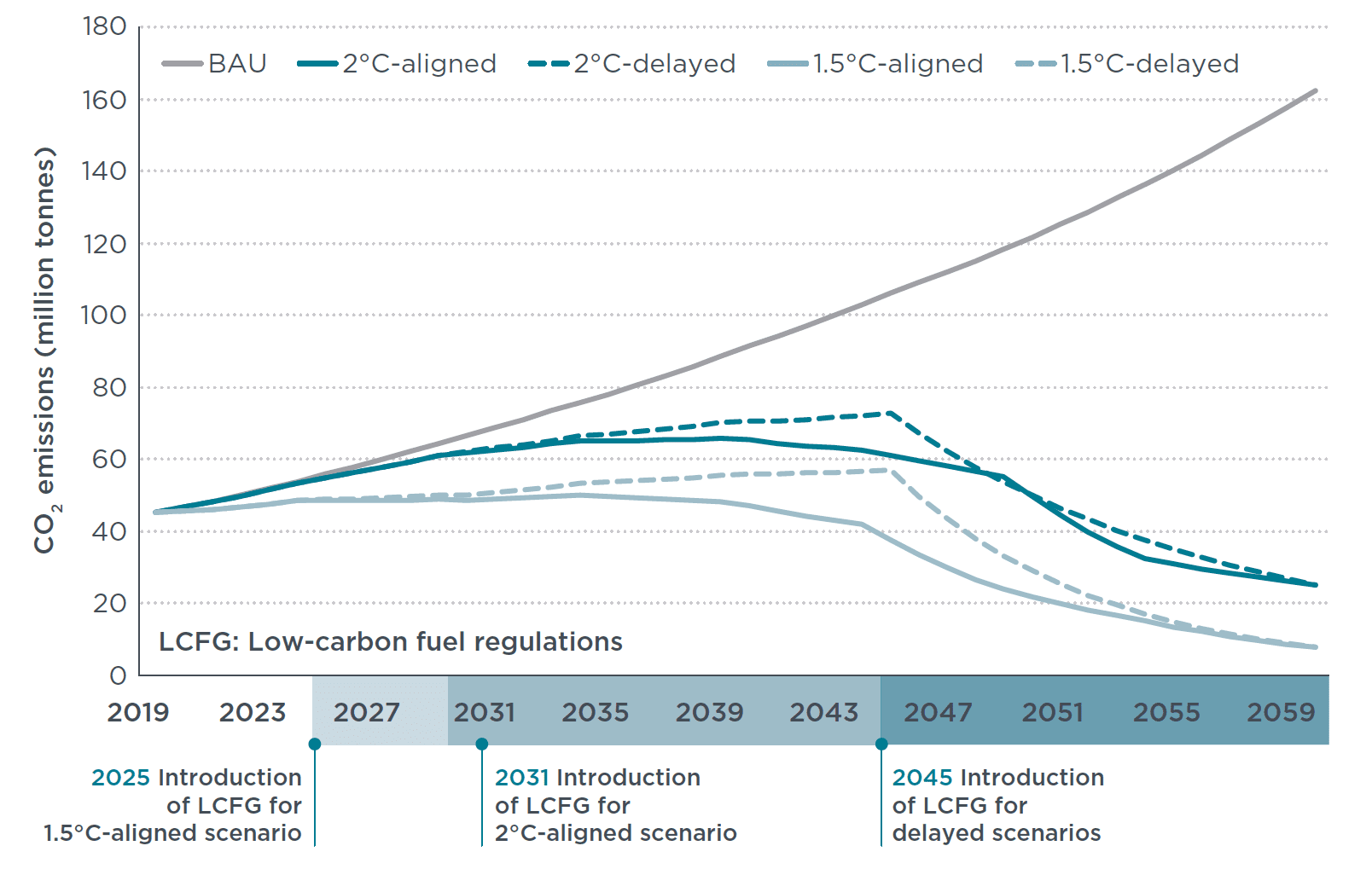

It uses the sector’s 2019 activities, energy consumption, and CO2 emissions as a baseline and projects those out to 2060 under three scenarios: a) Business-as-usual (BAU), which assumes that the sector’s energy consumption will be governed only by adopted policies, with no new policies proposed and implemented after 2019; b) a 2°C-aligned scenario, which assumes coastal shipping maintains its 2019 share of a 2°C transportation sector CO2 budget in future years; and c) a 1.5°C-aligned scenario, which assumes that the sector maintains its 2019 share of the 1.5°C CO2 budget for the transportation sector. The 2°C-aligned and 1.5°C-aligned scenarios require 44%, and 83% reductions, respectively, in CO2 emissions in 2060 compared with the 2019 baseline.

We considered two broad categories of policy actions in addition to adopted policies to reach the goals of 2°C-aligned and 1.5°C-aligned scenarios: improving energy efficiency and reducing the carbon intensity of shipping fuel. Finally, because fuel carbon intensity regulations (or low-carbon fuel regulations) are crucial to decarbonizing the shipping industry and are currently less mature and more costly than energy efficiency improvements, we considered two different implementation schedules for each of the 2°C-aligned and 1.5°C-aligned scenarios, while keeping their targets intact.

We found that:

- In 2019, China’s coastal shipping sector emitted about 45 million tonnes of CO2, or roughly 4.5% of total CO2 emissions from China’s transportation sector. With no additional policies, CO2 emissions from China’s domestic coastal shipping would more than triple to more than 162 million tonnes in 2060.

- With the help of mandatory energy efficiency standards as well as low-carbon fuel regulations, CO2 emissions from China’s domestic coastal shipping could peak by 2040 and fall significantly by 2060. We proposed two possible pathways for achieving this:

- With mandatory energy efficiency standards tightened every five years between 2025 and 2045 for newbuild ships, and with low-carbon fuel regulations slowly phasing in from 2030, CO2 emissions could peak by 2040 and decrease by 56% in 2060 relative to the 2019 baseline, which is aligned with the 2°C-target set for the transportation sector in the ICCSD report. The average carbon intensity of the fleet could fall by 79% relative to the 2019 baseline.

- With more stringent mandatory energy efficiency standards to be implemented between 2025 and 2045, and with low-carbon fuel regulations phasing in five years earlier (beginning in 2025), CO2 emissions could peak by 2035 and decrease by 83% in 2060 relative to the 2019 baseline, which is aligned with the 1.5°C-target set for the transportation sector in the ICCSD report. The average carbon intensity of the fleet could fall by 92% relative to the 2019 baseline.

- It is essential that low-carbon fuel regulations be implemented no later than 2030. If delayed until 2046 after expiration of mandatory energy efficiency standards, the required rate of fuel carbon intensity reduction would be dauntingly high for the industry.

Figure. Impact of delayed implementation of low-carbon fuel regulations for 2°C-aligned and 1.5°C-aligned scenarios