Heavy-duty zero-emission vehicles: Pace and opportunities for a rapid global transition

ZEVTC publication

Deploying charging infrastructure to support an accelerated transition to zero-emission vehicles

The quantitative analysis presented in this briefing shows that deployment of electric vehicle charging infrastructure needs to ramp up considerably if Zero Emission Vehicles Transition Council (ZEVTC) member jurisdictions are to align infrastructure with their ambitions for ZEV sales. Leading ZEVTC members have incentivized infrastructure deployment in many financial and non-financial ways, and based on a review of policy approaches, the paper also identifies priority areas for government focus and policies that can help overcome common barriers.

Key takeaways:

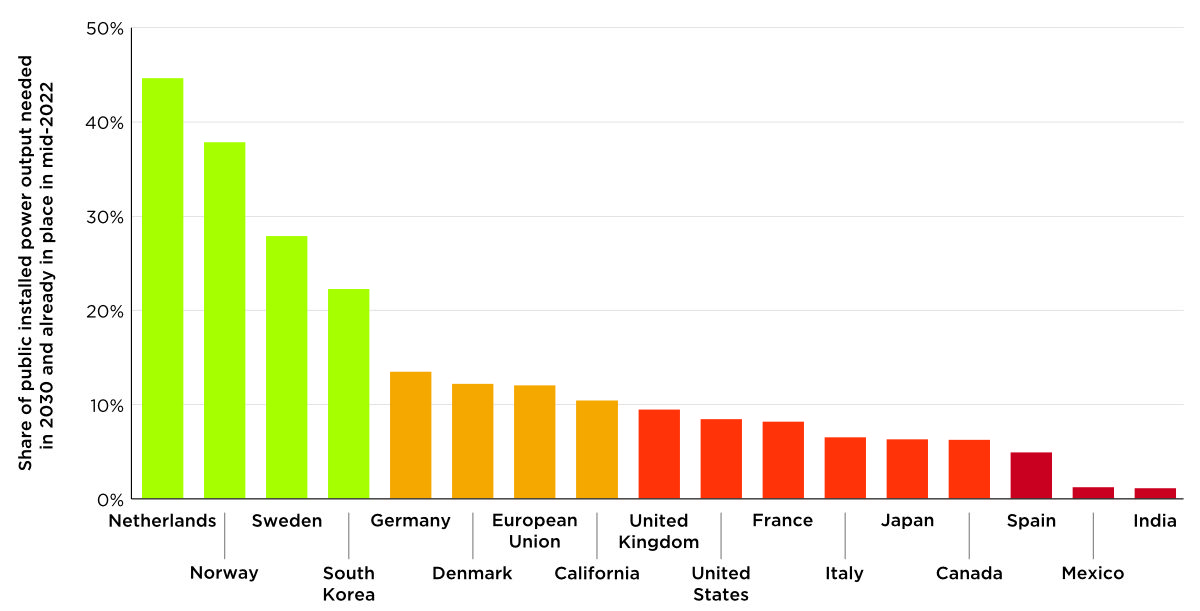

More than 100 million chargers, including 6.2 million public ones representing 240 GW of public installed power output, will be needed across ZEVTC jurisdictions by 2030. As of mid-2022, only 13% of public chargers and 10% of power output were in place. As shown in the figure, the Netherlands and Norway have the most infrastructure already installed.

Figure. Share of projected public installed power output needed in 2030 that was already in place as of mid-2022.

As charging infrastructure requires careful planning and takes time to be installed, ZEVTC governments need to act now to ensure sustained build-out. For light-duty vehicles, the yearly growth rate of installed public charging power output needed between mid-2022 and 2030 is estimated to range from 7%–8% in the Netherlands and Norway to over 50% in India and Mexico. For heavy-duty vehicles, the same countries are at both ends of the spectrum, but the growth rates needed are much higher in many countries and almost no public charging has been deployed so far.

This paper estimates the cost of hardware, installation, and planning required for public and private charging infrastructure in all ZEVTC jurisdictions is approximately €336 billion over the period to 2030. These costs will be shared between the public and private sectors. Emerging government programs showcase that infrastructure policies need to include planning and coordination among stakeholders that breaks silos between agencies of energy, transportation, and environment and includes electricity utilities. There are several effective policy approaches:

- Set binding installation targets for charging infrastructure to align with expected ZEV growth. These are most effective when they carry binding obligations for public and private stakeholders to ensure that infrastructure deployment matches the needs of different vehicle types and travel patterns.

- Use regulatory tools and incentives to address charging gaps and improve the business case for private investment. Policy mechanisms that encourage efficient and faster deployment of private capital will help governments limit the role of public funding in the long term. Equity-centered programs can promote charging access in rural and disadvantaged communities that have lower rates of electric vehicle ownership and building codes can promote charging installation in multi-unit dwellings where owners might not otherwise see a business case.

- Empower utilities to support ZEVs by designing electric vehicle-friendly rate structures and encouraging smart charging. Regulators can enable public and investor-owned utilities to pay for grid upgrades through phased introduction of new rate structures for electric vehicle charging. Additionally, as smart charging balances the grid load, it can potentially defer expensive grid upgrades.