STACKS

The steep descent to net-zero aviation

- Aviation’s contribution to climate change

- Cumulative global aviation CO2 emissions

- Improve efficiency

- Sustainable aviation fuels

- Fuel projections through 2050

- Zero-emission planes

- Economic incentives

- Carbon pricing per effort scenario from 2020 to 2050

- Changing travel habits

- Choose your emissions

- Glossary

- Credits and sources

Aviation poses a difficult challenge to the global effort to decarbonize transportation. Air travel is popular, and emissions from the sector are growing rapidly. But the low-carbon technologies required to decarbonize aviation are immature and expensive. For this reason, aviation (along with shipping and energy-intensive industrial sectors such as steelmaking) is often described as “hard to abate.” Decarbonizing aviation will not be easy.

Still, strategies to bring about a low-carbon aviation sector are emerging. This card stack aims to summarize how cleaner fuels, new aircraft designs, smarter operational practices, improved aircraft technology, effective policy incentives, and more selective use of air travel could, in principle, combine to greatly reduce the greenhouse gas footprint of aviation. None of these is a silver bullet. The full range of these diverse measures will be needed to achieve meaningful decarbonization of the sector.

-

Aviation’s contribution to climate change

-

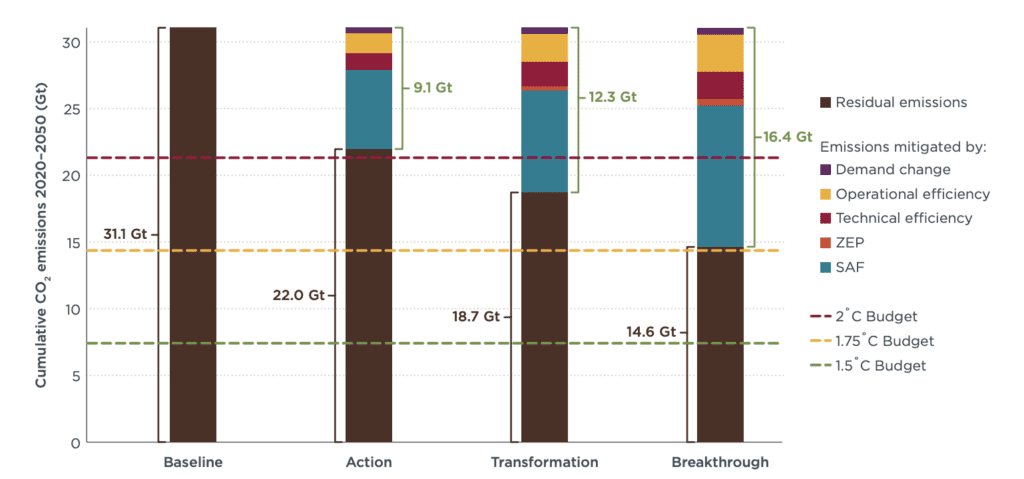

Cumulative global aviation CO2 emissions

Cumulative global aviation CO2 emissions, 2020–2050, baseline and three scenarios of progressively greater decarbonization effort. Source: Graver et al., Vision 2050: Aligning aviation with the Paris agreement.

-

Improve efficiency

-

Sustainable aviation fuels

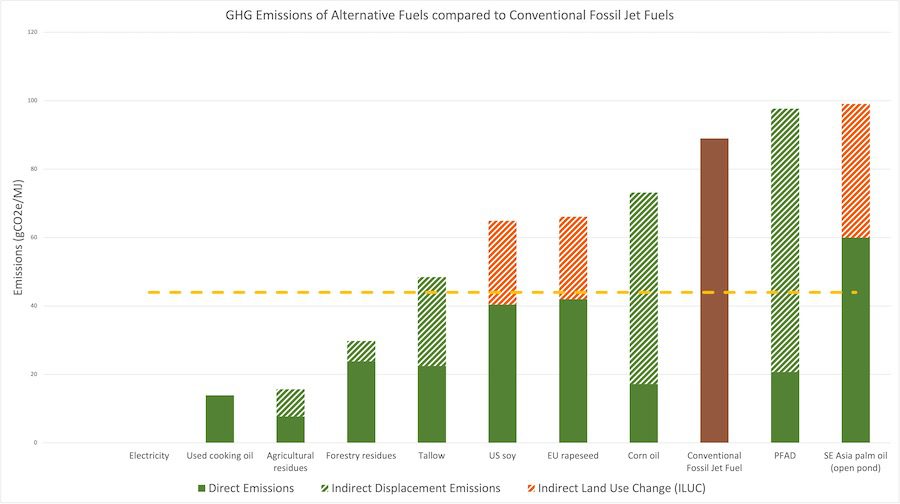

Cleaner fuels, more than efficiency gains, are expected to drive aviation decarbonization in the decades ahead. Sustainable aviation fuel, or SAF, is an umbrella term used to denote “drop-in” alternatives to conventional jet fuel that can be used in today’s aircraft and engines. In the Vision 2050 analysis, SAFs could account for 62% percent of emission reductions under the most ambitious Breakthrough scenario. Similarly, a 2022 ICAO analysis estimated that SAFs could deliver 55% of the CO2 reductions needed. Such findings, while encouraging, come with caveats.

SAFs can be produced from a variety of biological feedstocks and renewable energy (also termed “power to liquid” or e-kerosene), with varying degrees of environmental integrity. Public policies intended to support the development of SAFs include a performance requirement: for example, the U.S. Inflation Reduction Act stipulates that only SAFs that produce a 50% reduction in lifecycle emissions compared to conventional jet fuel qualify for funding support under the law. This chart breaks down the direct and indirect emissions of potential SAFs and shows those fuels that meet a 50% reduction threshold.

GHG emissions from feedstocks that claim SAF status, and fossil jet fuel.

Indirect emissions comprise two categories. Displaced emissions occur when a large industry’s securing of limited supplies of a low-carbon fuel is achieved at the expense of other industries, which then must resort to carbon-intensive substitutes. For example, if the palm fatty acid distillates (PFADs) – a fuel worse than conventional jet fuel (see above chart) – currently used in livestock feed are diverted to make aviation fuel, feed producers would likely turn to palm oil, whose total emissions are very high—higher than those of conventional jet fuel. Indirect land-use change (ILUC) refers to land use changes that occur when existing cropland is used to produce feedstock for biofuels. It results in the displacement of other agricultural activities, for example: in Brazil, as soy oil production increased, farmer’s pasture raising lands decreased. As a consequence, farmers moved their pastures to unclaimed forest land –creating a cycle of land displacement.

In sum, full life-cycle accounting of emissions from SAFs is necessary. Only SAFs that can substantially reduce GHGs after accounting for both direct and indirect emissions are likely to help decarbonize aviation.

SAFs will likely be rolled out over the near, medium, and long term as different types of SAFs mature.

Near term. Fuels produced from used cooking oil and beef tallow, known as hydro-processed esters and fatty acids (HEFA) fuels, are already available for use in aircraft. The HEFA process converts virgin vegetable oils, or waste fats, oils, and greases, into hydrocarbons through deoxygenation. It creates a hydro-treated vegetable oil that is chemically similar to kerosene and therefore requires little modification for use in an aircraft. As the chart shows, the GHG life cycle (direct and indirect) emissions of most HEFA fuels are half the levels of conventional jet fuel or less, and therefore qualify as SAFs.

The chief obstacle to the use of HEFA fuels is their limited supply. With competition from other transportation sectors that can also use HEFA fuels, ensuring a sufficient volume of HEFA fuels for aviation may be difficult.

Medium term. Advanced biofuels derived from agriculture and forestry wastes are expected to become more common in the medium term. These are not the biofuels made from food crops like corn and soybean that are still being used today but provide little emissions reduction benefits. Instead, advanced biofuels are made from waste residues such as corn stalks and forest branches that offer substantial GHG savings if harvested sustainably, i.e., in ways that avoid erosion and soil carbon loss. Because advanced biofuels are made from inedible (by humans) plants and parts of plants consisting mainly of cellulose, they are also referred to as cellulosic biofuels. The greatest opportunity in cellulosic biofuels may be to use “energy crops” such as willows and elephant grass. Fuels derived from these sources have much lower emissions from land use than food-based biofuels have; note the low emissions values of agricultural residues and forestry residues shown in the chart above. Food-based biofuels, made from crops such as corn, soy, rapeseed, and palm, do not meet the emissions criteria to qualify as SAFs (see chart).

Long-term. SAFs in the long-run are likely to be e-fuels and liquid hydrogen, which can offer large reductions in GHGs if renewable energy is used to make them. Both e-fuels and liquid hydrogen (LH2) fuels are made by using electricity to split water into hydrogen and oxygen, then combining the hydrogen with carbon dioxide to produce liquid synthetic hydrocarbon fuels that are chemically indistinguishable from the fossil fuels (diesel, methane, jet fuel) they are intended to replace; hence the term “drop-in” fuels. Producing these fuels requires substantial amounts of power, because the process is inherently energy inefficient. Around half of the input energy of the electricity used (56-63% for LH2 and 51-58% for e-kerosene) is lost in the production process. And while e-kerosene (as aviation e-fuel is known) and liquid hydrogen can be very low-carbon replacements for conventional fuel, that is true only if they are produced using truly renewable electricity – i.e., generated with zero carbon emissions. But alternative fuels produced using power from the U.S. grid (with current state policies) could be as much as twice as carbon intensive as fossil jet fuel. Further, additional amounts of e-kerosene and LH2 produced for aviation would be low carbon only if they’re produced using additional renewable power. Poaching renewable electricity from another use, if it must be replaced by non-renewable energy, is merely an accounting trick.

-

Fuel projections through 2050

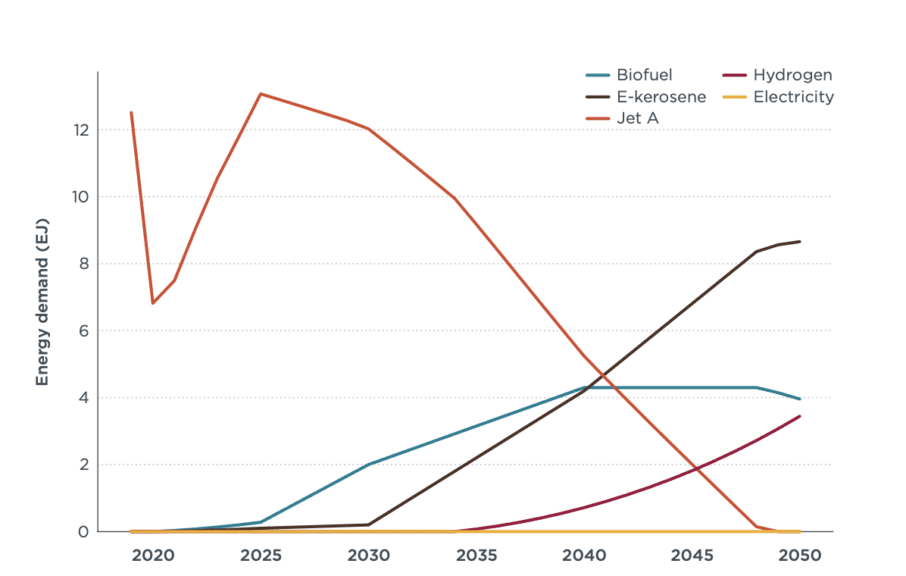

The chart below depicts the transition from conventional jet fuel to lower-carbon alternatives under a high-effort scenario that leads to 100% use of SAFs by 2050. The orange line shows a decline in use of conventional jet fuel from 2025 through 2050. Biofuels start their growth around 2023 (blue line), e-kerosene begins to take off around 2030 (brown line), and hydrogen fuels begin in 2035. Electricity (yellow line) is hardly visible, largely because the demand for electric aircraft will, we estimate, account for only 0.01% of total energy demand.

Fuel projections through 2050 in the Vision 2050 Breakthrough scenario

-

Zero-emission planes

-

Economic incentives

-

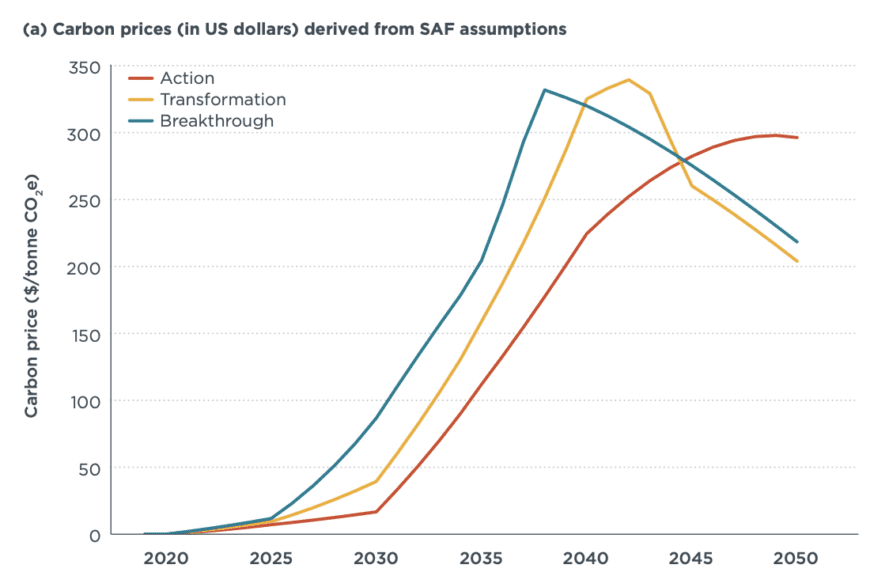

Carbon pricing per effort scenario from 2020 to 2050

In the high-effort scenario (blue line), carbon prices peak before 2040 because early, aggressive government policies lead to economies of scale for SAF production. The mid-effort scenario (yellow line) shows a delayed carbon price peak around 2045, after which time prices drop steeply as SAF volumes expand. In the low-effort scenario (red line), lower SAF production volumes in early years mean that SAF costs do not peak until sometime after 2050.

Another potential tool for generating funding for clean fuels would be to tax tickets and earmark the revenue for technology demonstration and deployment. Taxes, like a ticket tax, could be designed to shift some of the cost of technology from those who fly infrequently to relatively prosperous frequent fliers. Indeed, almost two-thirds of aviation CO2 is emitted by upper-income country residents, while countries representing the poorer half of the world emit only 10%. Any discussion of the prospects for decarbonizing air travel should recognize that air travel’s benefits skew toward prosperous people, while its climate impact affects everyone.

-

Changing travel habits

Technological and efficiency gains alone cannot achieve the carbon reductions required in aviation. Changes in travel habits, from allowing consumers to choose lower-emission flights to encouraging modal shift for short journeys, will make the path to decarbonizing aviation easier.

Trains, trains, trains…

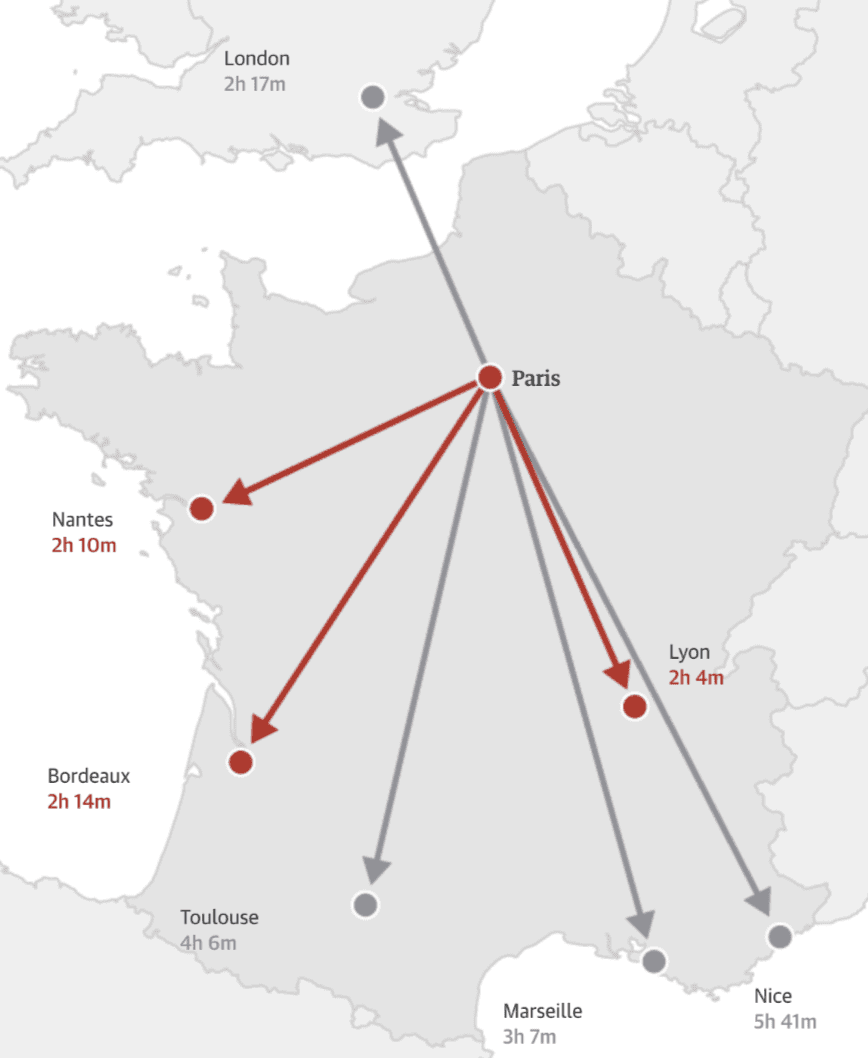

For short trips, trains can be cleaner and more convenient than air travel. Short flights are the most carbon intensive, because takeoff, with its high rate of fuel burn, accounts for a larger share of a short flight than of a long one. A flight of less than 500 kilometers emits roughly 199 g CO2/passenger-kilometer, while a diesel train in the U.S. emits roughly 64 g CO2/passenger-kilometer. By one estimate, train travel could reduce short-haul flight traffic by up to 28% and significantly reduce carbon emissions. Moreover, trains are often more spacious and comfortable than planes, while train stations can be more accessible and convenient than airports. And for short distances, trains are competitive with planes in terms of door-to-door trip duration. In sum, for short trips, train travel can be a better option, environmentally and practically.

Still, the modal shift from planes to trains relies on government initiative to invest in rail. For example, as part of their decarbonization path, France imposed a ban on short-haul flights where train journeys of two and a half hours or less are available, which is projected to eliminate 12% of French domestic flights. Other EU member states are reportedly considering similar bans. The map below highlights the routes impacted (in red) by the French ban compared to those unaffected by the ban. Policies such as this will help to shift travel away from short-haul flights, and limit aviation’s emissions into 2050.

Flights impacted by the French ban on short flights. Gray lines indicate flight paths that will remain unaffected, red lines indicate banned flight paths.

-

Choose your emissions

-

Glossary

-

Credits and sources