Materials and battery supply chains ready to meet future global EV demand

Report

Electrifying road transport with less mining : A global and regional battery material outlook

The acceleration of the transition to battery electric vehicles (BEVs) entails a rapid increase in demand for batteries and material supply. This study projects the demand for electric vehicle batteries and battery materials globally and in five focus markets—China, the European Union, India, Indonesia, and the United States—resulting from policies and targets that have already been adopted or are under discussion. This is compared with announced battery cell production and mineral supply capacities. The study covers all segments of road transport, including sales in the light-duty, heavy-duty, and two- and three-wheeler vehicle segments as well as non-vehicular demand. Given the uncertainty surrounding the future development of battery technologies, this study also evaluates sensitivity scenarios for a higher-than-baseline market share of lithium iron phosphate (LFP) batteries and a large-scale application of sodium-ion batteries. Finally, this analysis explores how efficient battery recycling, a reduction in the average battery size of passenger BEVs, and a change in vehicle sales through transport demand avoidance and modal shift policies could reduce the demand for raw materials while maintaining a rate of vehicle electrification aligned with announced policies and targets.

Key findings

Our analysis supports the following conclusions:

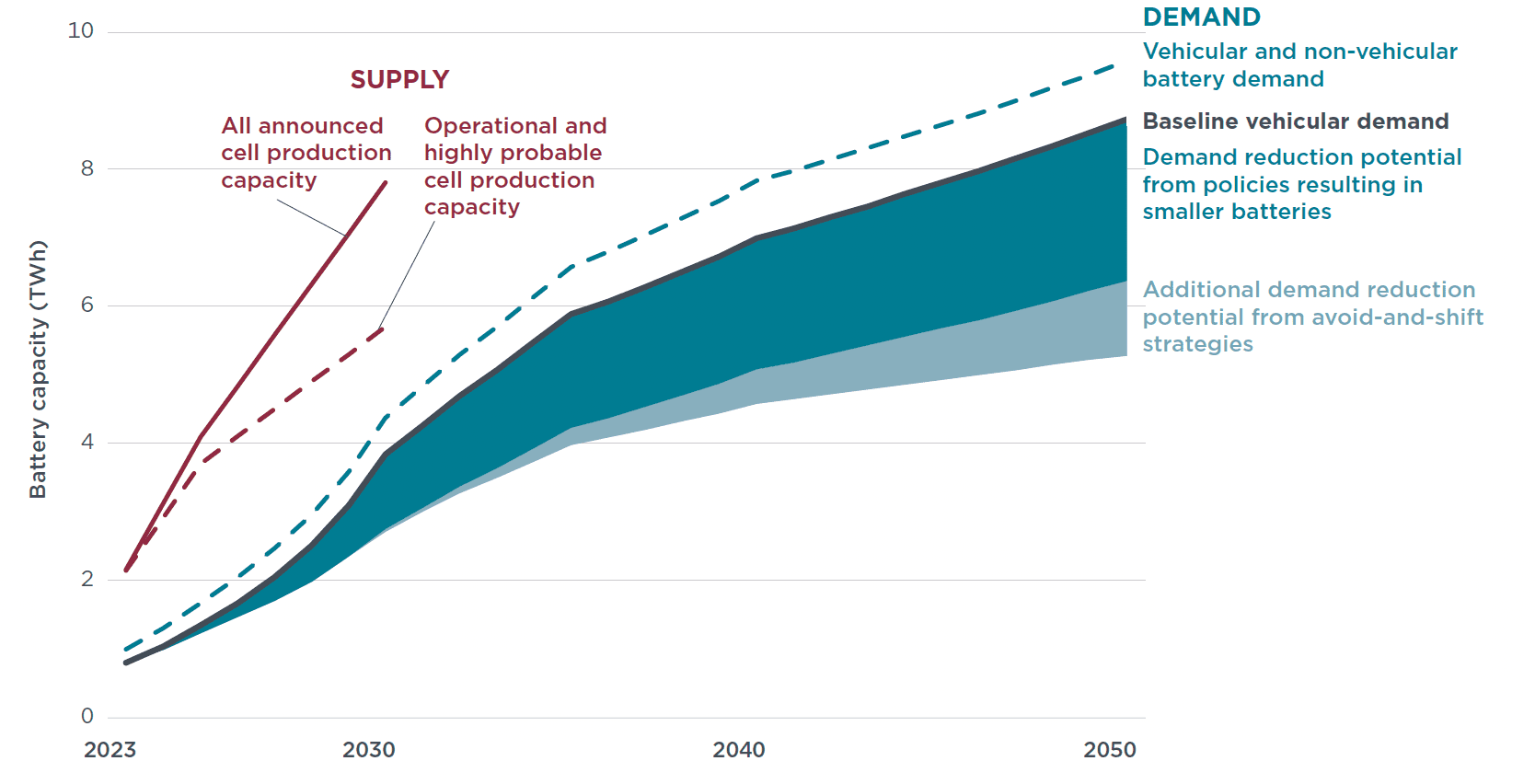

Announced battery production plant capacities significantly exceed the projected global road transport and non-vehicular battery capacity demand.

On a global level, the total announced cell production capacity and the proportion of this capacity that is considered highly probable, exceed projected demand at least until 2030. The majority of the announced cell production capacities are in China, corresponding to 84% of the global total in 2023 and 67% in 2030. In the European Union, announced cell production capacities could meet an estimated 99% of the region’s road transport and non-vehicular battery capacity demand in 2030 if all projects are realized, while production capacities in the United States correspond to 130% of domestic demand in 2030. When considering only facilities that are either already operational and those under construction that are considered highly probable to reach the announced output, capacities in the United States correspond to 103% of domestic demand in 2030, while those in the European Union cover just 72% of road transport and non-vehicular battery capacity demand, highlighting the importance of EU Member States supporting the realization of announced investments. In India and Indonesia, the capacities of the announced cell production plants are comparatively more limited, corresponding to a projected 49% and 44%, respectively, of domestic vehicular battery demand in 2030.

Figure 1. Annual global battery demand by demand reduction scenario compared with announced cell production capacity

The scaling-up of battery material supply is projected to catch up with growing demand.

Assuming a continuous increase in the average battery size of light-duty vehicles and a baseline scenario for the development of the market shares of LFP batteries, we estimate that mining capacities in 2030 would meet 101% of the annual demand for lithium, 97% of the demand for nickel, and 85% of the demand for cobalt that year, including the demand for these minerals in other applications. When considering a scenario with higher market shares of LFP batteries, the capacities would meet a slightly higher 102% of lithium demand, along with 108% of nickel demand and 103% of cobalt demand. These scenarios highlight that the market can continue to react to low supply or high prices of individual materials by switching to higher market shares of battery technologies containing none or less of these materials.

In the long term, global mineral reserves are sufficient to meet battery demand.

In a scenario in which the battery demand through 2050 were met only with lithium-ion battery technologies already commercialized in 2024, and in which no material demand reduction measures were implemented, cumulative material demand would correspond to 49% of current land-based lithium reserves, 38% of nickel reserves, and 38% of cobalt reserves. As reserves include only those deposits that are currently explored and profitable to extract, they do not reflect the full availability of minerals. Given advances in mineral exploration and mining technology, deposits classified as reserves keep increasing, exemplified by a doubling of lithium reserves in the past five years alone, and it is likely that they will continue to increase in the future,

Despite a general reliance on global material supply chains, domestic reserves can partially meet domestic battery demand.

Individual countries and regions have ample reserves of certain minerals that exceed domestic demand. However, none of the focus markets of this study has sufficient domestic reserves of all key battery materials to meet their projected domestic battery demand. Building resilient international supply chains to secure ample battery-grade minerals is thus necessary to achieve a rate of vehicle electrification aligned with adopted and proposed policies and targets.

Smaller average battery sizes, especially for light-duty BEVs, can significantly reduce battery and related mineral demand in the near term.

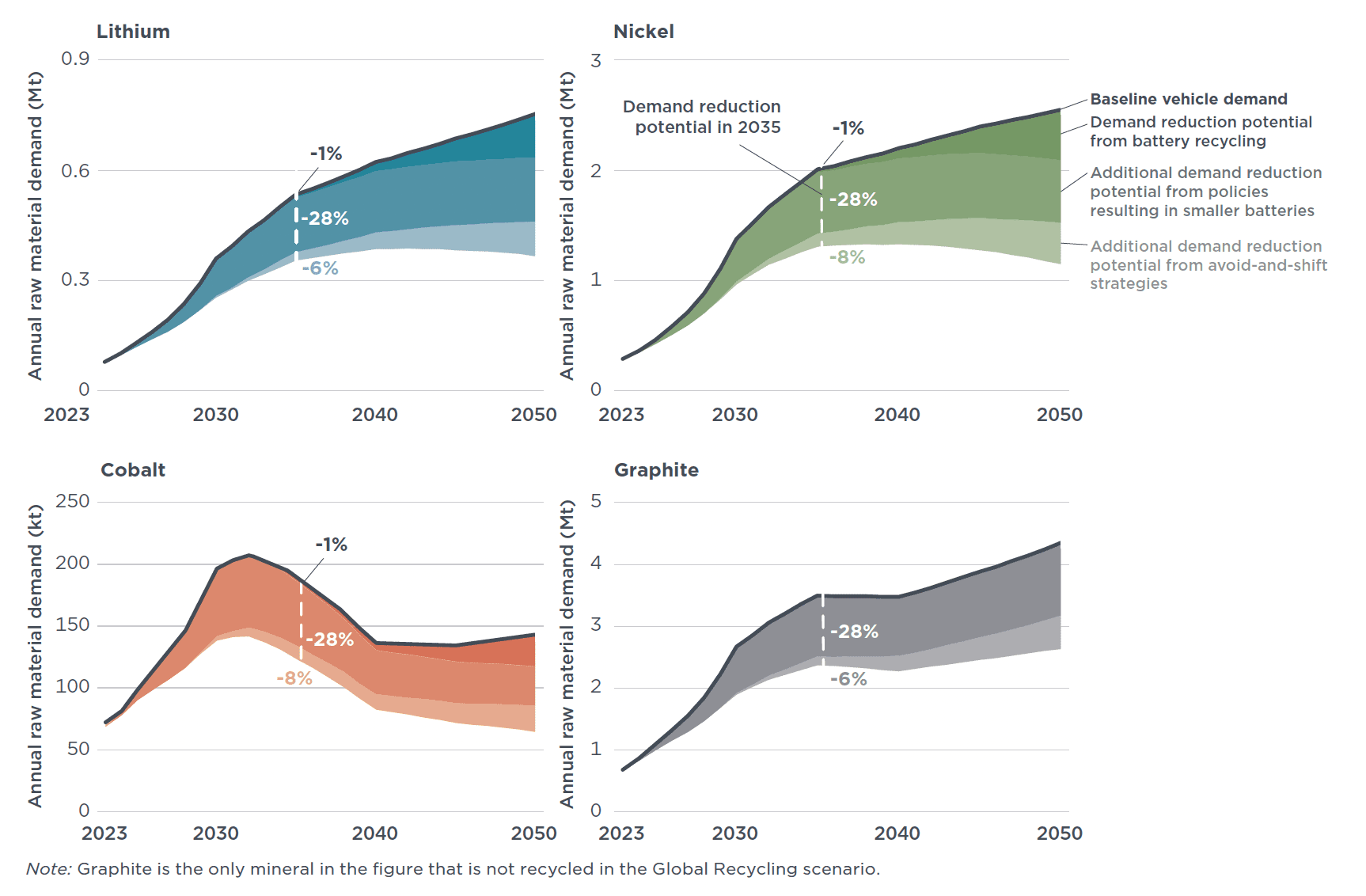

Improvements in vehicle energy efficiency can contribute to reductions in average battery sizes for a given vehicle range, while the deployment of more charging facilities can lower the demand for longer-range BEV models. Reducing the average battery size of light-duty BEVs by 20% by 2030 compared to today’s level means more affordable BEVs with lower operational costs and would reduce the annual global battery demand by 28% in 2035 and 27% in 2050 relative to a baseline scenario in which the average battery size increases by 20% (or 10% in the United States) by 2030. This translates into an equivalent decrease in demand for lithium, nickel, cobalt, manganese, and graphite in both years. Out of the evaluated measures, this was found to be the most immediate way of reducing battery (and thus raw material) demand.

Figure 2. Annual global raw material demand for lithium, nickel, cobalt, and graphite under the Baseline and demand reduction scenarios, all with the Baseline battery technology shares

Policy recommendations

Policymakers could consider various measures to reduce the environmental impacts of new raw material mining and refining while maintaining the rate of vehicle electrification. On a regional level, several measures can support a reliable supply of battery cells and raw materials.

- Policies reducing the average battery sizes of light-duty BEVs, establishing efficient battery recycling, and implementing avoid-and-shift strategies can help to reduce the demand for new mining.

- Predictable BEV adoption policies, incentives for domestic battery material mining, refining, and cell production, and trade agreements with mineral producing countries could help to build reliable supply chains.

- Setting battery durability standards and supporting research in emerging battery technologies can alter the pathway of vehicle battery-related mineral demand.

For media inquiries, please contact Susana Irles, Senior Communications Specialist, at communications@theicct.org.