EPA should work to quickly finalize multipollutant rule for light and medium-duty vehicles

Blog

Infrastructure and supply chains won’t hold up EPA’s proposed light and medium-duty vehicle standards

The U.S. Environmental Protection Agency’s (EPA) light and medium-duty vehicle proposal builds upon important climate legislation enacted in last year’s Inflation Reduction Act (IRA) and in the 2021 Infrastructure Investment and Jobs Act (IIJA). EPA expects the regulation, proposed on April 12, 2023, to lead to a 67% electric vehicle (EV) sales share in 2032 for light-duty vehicles such as cars, SUVs, and passenger pick-up trucks and 46% for medium-duty vehicles including vans and larger pick-ups.

This proposal is a critical complement to fiscal incentives. It establishes a clearly defined timeline for automakers to ramp up EV production and sales and allows other supporting businesses – from automotive suppliers and battery manufacturers to charging infrastructure companies and electric utilities – to invest with confidence. And with wait times for EV purchases hovering around 6 months, consumers are clearly demanding more and faster EV production.

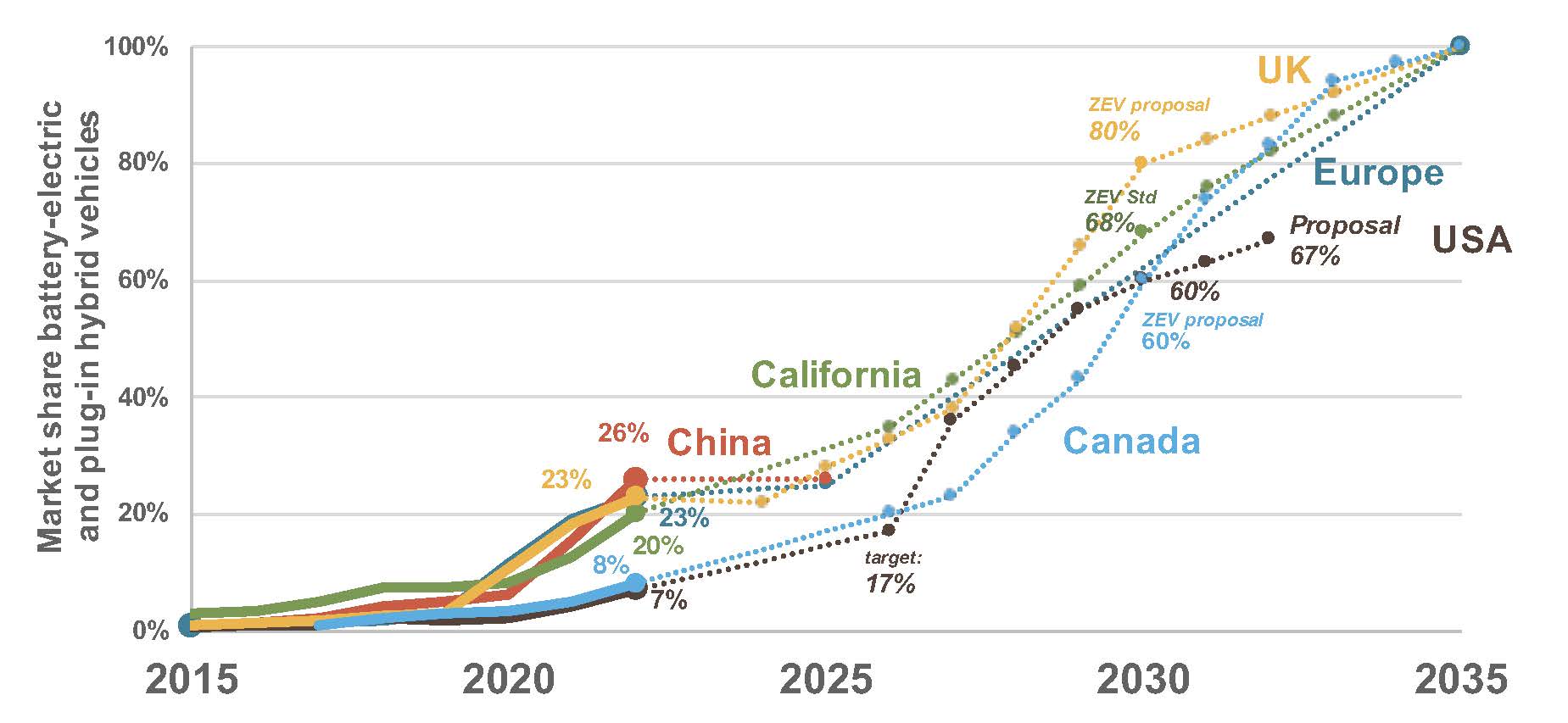

When it’s finalized and implemented, EPA’s regulation will put the United States on par with other leading countries and jurisdictions in terms of growing EV sales. In 2022, 7% of new U.S. light-duty vehicle sales were electric, trailing California (20%), the European Union (23%), the United Kingdom (23%) and China (28%). EPA’s proposal will help the U.S. catch up to global leaders in terms of EV targets as early as in 2027.

This graph shows historical EV sales shares (solid lines) and regulatory targets (dotted lines) for light-duty vehicles. Not shown, the 46% EV sales share EPA projects for medium-duty vehicles in 2032 is more ambitious than the 40% required for this category in California’s Advanced Clean Trucks (ACT) rule, a reflection of how much the market and technology has advanced since the ACT was passed in 2020.

Figure: Historical (solid lines) and regulatory targets (dotted lines) for EVs in different jurisdictions. (Note: Data for China and the United States is from Marklines. Data for Europe is from the European Environmental Agency (EEA) and Dataforce. Data for China and Europe only includes passenger cars, while data for the United States also includes light trucks.)

These targets line up with announcements from auto manufacturers. Ford, GM, Mercedes-Benz, Audi, and others have committed to selling 100% EVs globally or in leading markets by 2035. Stellantis (which includes Chrysler) and Volkswagen have set more ambitious goals of 100% and 70%, respectively, for their European sales in 2030 compared to the 50% EV sales target they set for the U.S. That shows automakers can deliver more to the U.S. market – if we put the right policies in place.

Critically, major automakers are collectively investing over $1.2 trillion in EVs globally. EPA’s proposed rule will help bring a significant share of that investment to the United States.

EPA’s proposal and goals from automakers are realistic and possible because of technological advancements in EVs and batteries, their underlying economics, and impactful policy incentives. We already know that consumers will save money over the first ownership period of an electric passenger car, thanks to lower fueling and maintenance costs. In terms of vehicle cost – and by extension price at the dealership – we expect light-duty EV manufacturing costs to fall below those of their gasoline counterparts for cars, crossovers, SUVs, and pick-ups starting as soon as next year for electric cars with 150-mile range and for all electric passenger vehicles with ranges up to 400 miles by 2030 except for pickups (2033), even without incentives.

The IRA will boost consumer savings even more. Although the U.S. Treasury Department’s new guidance restricts the $3,750-7,500 tax credit to 14 models, compared to 91 EV models available on the market, those 14 account for most EV sales. Bloomberg New Energy Finance reported that 65% of all U.S. EV sales would qualify for at least part of the tax credit based on 2022 sales data.

Admittedly, there is significant uncertainty as to the number of EV that will be eligible for all or part of the $7,500 tax credits over the next decade. Accounting for this uncertainty, we forecast that new EV sales could reach 56-67% in the U.S. by 2032 based on consumer demand supported by EV tax credits and state adoption of supporting policies. This means that the IRA could get us most – or all – of the way to the EPA’s proposed EV sales target that matches the high end of our forecast as 67%.

Since there are more than enough minerals available for a global transition to EVs, the challenge is how to scale up investments into mining and battery production within this decade. With the IRA’s Advanced Manufacturing Production Tax Credit and the domestic content provisions in the Clean Vehicle Tax Credit, the U.S. directly incentivizes mining, recycling, and battery production on U.S. soil, and further supports establishing resilient material supply chains from friendly countries. The manufacturing subsidy of $45/kWh cuts about one third of total battery costs (global average of $151 in 2022), making battery production in the U.S. even cheaper than in China.

This support showed an immediate effect. In response to the IRA, we saw a significant uptick by more than one-third in announced plans for battery production facilities, catching up with Europe. Longer-term forecasts now indicate U.S. battery production capacity at 1 TWh by 2030, within striking distance of forecasted battery demand of 1.2 TWh taking the proposed EPA standards into account.

So why are EPA’s standards necessary if the IRA might already be enough to deliver significant EV growth?

Because the IRA is a supporting mechanism, not a roadmap. We’ve seen that unless they’re held to meaningful standards, automakers dial back on their commitments to EVs. For example, GM committed to deliver 23 EV models in 2023. That number is now down to eight.

More than that, clear targets and sustained commitments will help build out the charging infrastructure needed to support accelerated electrification. Other countries have met that challenge, and so can we. Norway hit nearly 80% EV sales in 2022 with one public charger for every 26 EVs. Significant resources are already being dedicated to charging, including the $7.5 billion allocation from the IIJA as well as several billions of dollars in power utility and private sector investment. For example, British Petroleum announced plans to invest $1 billion in EV charging in the U.S. by 2030. Automakers are investing too – GM, working with its dealers, aims to install up to 40,000 public charging stations across the U.S. and Canada. Globally, Bloomberg New Energy Finance expects $100 billion to be spent to grow charging infrastructure in the next 3 years alone.

Lastly, EPA’s proposal is what we need to get closer to meeting our climate goals. In an earlier analysis, we found that nearly 70% EV sales share would be needed by 2030 (along with improvements in gasoline vehicle efficiency) to reach the goals we set in the Paris Climate Agreement. EPA’s proposal moves us close to that.

Finalizing the regulation would address climate change, respond to EV market demand, and enhance U.S. global competitiveness while establishing the EV roadmap that automakers, suppliers, charging companies, and utilities need to make needed investments with confidence. That’s why the EPA should move ahead as quickly as it can to finalize and implement its proposal.