Report

European Vehicle Market Statistics – Pocketbook 2023/24

The ICCT’s European Vehicle Market Statistics 2023/24 Pocketbook offers an annual statistical snapshot of the evolving landscape of the EU’s car, van, truck, and bus markets in their journey toward decarbonization. The report encompasses data spanning from 2001 to 2022, focusing on vehicle sales, fuel efficiency, greenhouse gas emissions, and air pollutants. For user-friendly navigation through the facts and figures, please visit our website at eupocketbook.org.

The latest findings from the 2023/24 report indicate a sustained decline in vehicle sales across the EU market. This trend has persisted since the peak in 2019, with the COVID-19 pandemic causing a setback in sales growth. In 2021, sales continued to contract, falling by 3% compared to the previous year and plummeting by 26% in comparison to the 2019 peak.

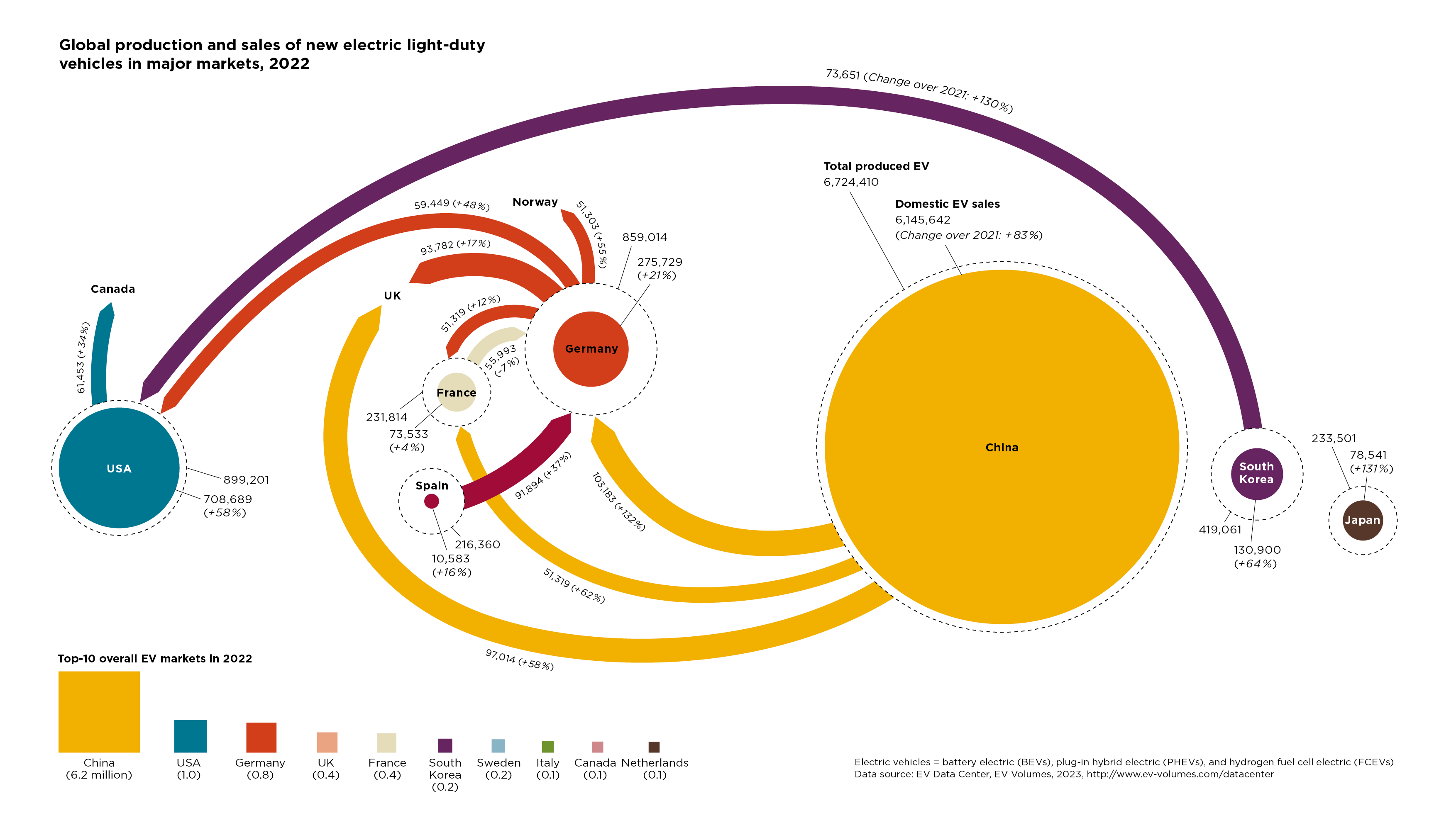

In terms of the electric car market, the report highlights a stabilization in early 2023, following a remarkable period of growth. In 2022, the EU’s electric passenger car market share reached 22%, establishing a significant presence. While this exceeded the United States, which registered a 7% market share, the EU still trailed behind China, where electric vehicles accounted for a substantial 32% of the market.

Moreover, the report underscores noteworthy progress in reducing carbon emissions. Average CO2 emissions from new passenger cars, as assessed using the Worldwide Harmonized Light Vehicles Test Procedure (WLTP), declined to 110 g/km in 2022 within the European Economic Area. This marked a notable decrease of approximately 6 g/km when compared to the emissions recorded in 2021.

Other select highlights from the 2023/24 edition include:

- The electric car market made a significant leap from 3% market share in 2019 to 22% in 2022. However, growth temporarily slowed in early 2023, influenced by factors such as the expiration of government incentives and supply constraints.

- Leading the battery electric car segment in the European Economic Area are Norway (65%), the Netherlands (20%), and Sweden (19%). Larger EU vehicle markets, including Germany (14%), France (9%), Italy (5%), and Spain (3%), are adopting electric vehicles at varying rates.

- Norway and the Netherlands owe part of their electric car market success to extensive charging infrastructure. Norway boasted 14.5 publicly accessible charging points per thousand passenger vehicles in 2021, over seven times the EU average, followed closely by the Netherlands with eight charging points.