Blog

The impact of COVID-19 on new car markets in China, Europe, and the United States: V, U, W, or L?

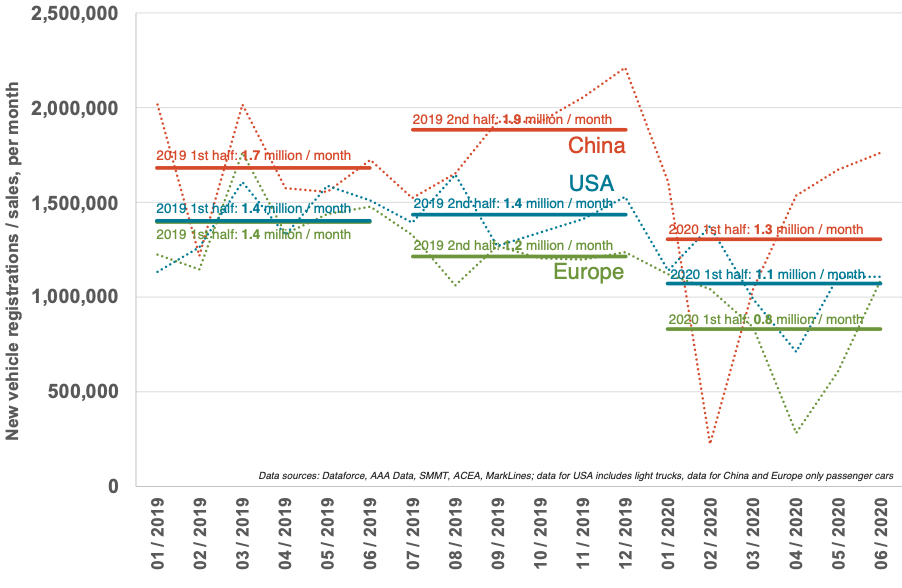

With new vehicle registrations data for the first half of 2020 now available, it is possible to take a closer look at the big three markets overall, and their respective electric vehicle market shares in particular.

As expected, year-to-date sales volumes are lower than they were in 2019. In China, during the first six months of 2020, an average of 1.3 million new passenger cars were sold every month. That is about 23% lower than in the first half of 2019. In Europe (more precisely the European Economic Area), roughly 0.8 million new passenger cars were registered each month, on average—about 43% lower than in the first half of 2019. And in the United States, monthly average sales of passenger cars and light trucks hovered around 1.1 million, which is about 21% lower than in the first half of 2019.

It is evident that COVID-19 had a drastic impact on vehicle markets during the first half of 2020, and also that it had a different impact on each of the markets. In China, the peak of the pandemic was reached in February. In the same month, new car sales dropped close to zero. Since then, however, the Chinese vehicle market saw a strong recovery, and has now reached pre-COVID-19 levels, resembling what economists call a “V”-shaped curve. In Europe, strict lockdown measures were implemented in most countries from the end of March onwards and were particularly prevalent throughout the month of April. Again, showing a “V”-shape curve, new car registrations dropped close to zero in April and have now returned to pre-pandemic levels. In the U.S., the pattern is not as clear-cut as in China and Europe. New passenger car and light truck sales decreased notably in April but not nearly as strongly as in the other markets. At the same time, there is currently no sustained upward trend in sales. The shape of the U.S. curve could possibly develop into something more like a “U,” with a slower downward trend, followed by a slower upward trend. What we are not witnessing in any of the markets, at least so far, is a second economic bump (“W”-shape) or a continued strong contraction in the automotive market (“L”-shape).

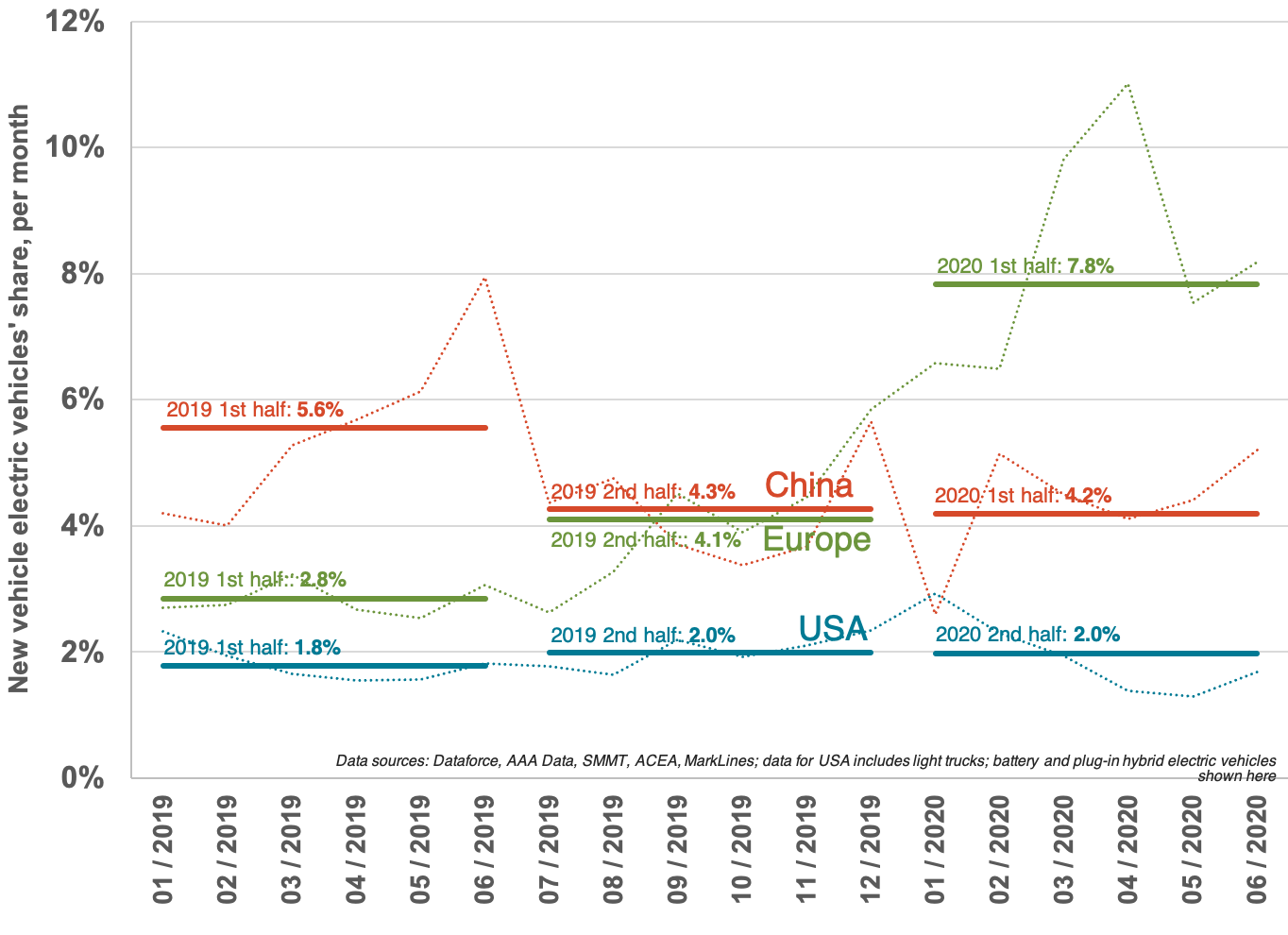

Turning from all new vehicle sales to electric vehicles specifically, it is remarkable how well the electric vehicle market in Europe is developing at the moment. Average electric vehicle shares increased from about 3.4% in 2019 to 7.8% in the first half of 2020. In April, electric vehicles in Europe accounted for 11% of all new vehicle registrations and, in May and June, still hovered around 8%. About half of the electric vehicles currently sold in Europe are battery electric, the other half is plug-in hybrid electric. A strong push for electric vehicles comes from the mandatory EU CO2 targets for manufacturers. From 2020 onwards, new passenger cars, on average, have to emit a maximum of 95 gCO2/km (about 58 mpg) – a level that most manufacturers haven chosen to comply with by deploying more electric vehicles. Another strong push for electric vehicles comes, unexpectedly, from efforts to reverse the COVID-19 related economic downturn. Several European countries have implemented comprehensive stimulus programs, and most of these recovery programs include generous purchase premiums for electric but not for combustion engine vehicles. In Germany, for example, vehicle owners currently receive a bonus of up to €9,000 when opting for an electric vehicle.

In China, where the electric vehicle share was higher than in Europe throughout 2019, sales have slightly decreased to around 4.2% during the first half of 2020. An underlying reason might be the reduction in purchase premiums for electric vehicles in China. At the same time, electric vehicle sales targets for manufacturers were tightened and strong non-fiscal incentives, such as license plate and registration privileges for electric vehicles, continue to be in place in China. In the United States, the share of electric vehicles has remained essentially unchanged throughout the past months, being stuck at around 2% and thereby much lower than in Europe and China.

For Europe, we expect a continued increase in the share of electric vehicles for the second half of the year. With the sales launch of the Volkswagen ID.3, it is likely that the world’s largest vehicle manufacturer will catch up with its competitors and bolster electric vehicle markets. Furthermore, the 2021 EU CO2 targets will be stricter than in 2020, thereby likely requiring manufacturers to deploy more electric vehicles in the year to come. In China, electric vehicle penetration is likely to remain stable or increase throughout the rest of the year, partially due to purchase premiums being extended to 2022 as part of the financial remedies to the vehicle industry in response to COVID-19. Moreover, the Chinese government is transitioning to a stronger focus on its new energy vehicle manufacturing mandate, with strengthened targets for vehicle manufacturers set for 2021 to 2023, plus a number of regional incentive programs. Meanwhile, the United States is at risk of falling behind Europe and China in terms of electric vehicles uptake. Even if scrappage schemes and electric vehicle tax credits are revived after the upcoming national elections in November, it likely will take several months for the policy decisions to show an effect on actual electric vehicle sales.